Given there will be very few perfect earnings reports in the coming weeks, the new macro will force investors to subjectively determine what is a good report and what is not a good report. Before we go into the pros and cons of the report, I want to say that Tesla’s low valuation is a primary reason we entered the stock coupled with a strong earnings report. We covered this yesterday in our notification blog:

“Tesla is trading quite low and has not traded this low since “the new macro.” The forward P/S is at 4.7 and the forward P/E is at 36.15. If you take the tumultuous market of 2022 as a comp, Tesla may have 20% and up to 100% room. For the best case scenario to happen, we need broad market participation.”

It was not a perfect earnings report – but the point is the stock is not priced for perfection. I think there’s a disconnect basically between the company’s fundamentals and the current stock price (barring any unforeseen black swan macro event).

The pros are the roughly 30% forward growth rate, no debt, $20 billion in cash on the balance sheet and an expanding operating margin (YoY) and expanding net margin (YoY). The catalyst is the lower prices that allow Tesla’s Model 3 to be included in the $7,500 EV credit. What was a $50K vehicle has now become a $40K vehicle with Tesla only eating $3K of the price as they’ve priced the vehicle at $47K to clear the $50K limitation on the EV credit. We covered this a few months back here.

Here is what the CFO said: “So based upon these metrics here, we believe that we'll be above both of the metrics that are stated in the question, so 20% automotive gross margin, excluding leases and rent credits and then $47,000 ASP across all models.”

The price cuts are between 7% to 20%. For example, a Model Y was originally $65,990 and will now be $52,990. Then, you add the $7500 EV credit and you get about $20K off the price of the smaller SUV.

An additional catalyst for Tesla stock is the manufacturing credits for battery cell packs, that were stated to be $3,700 per Model 3 and Model Y. Tesla’s manufacturing is partly overseas and the credit is only for domestic manufacturing. The CFO stated to expect this: “But we think on the order of $150 million to $250 million per quarter this year and growing over the course of the year as our volumes grow.”

Note: We discussed the credits Enphase was expecting on their microinverters here.microinverters here.

The cons are the free cash flow was down 50% this quarter to $1.4B and the gross margin is a bit softer. Notably, free cash flow increased 50% for FY2022 but it’s certainly something to watch as it’s partly due to higher inventories. However, given the zero debt and $20B in cash (Tesla makes substantial interest on this cash), the company has time on their side to recover the FCF margin. In other words, to beat Tesla up over this while it’s far and above the better auto OEM on the bottom line, is perhaps lacking perspective. With that said, it’s earmarked as the number one thing to watch moving forward.

Financials:

Given the recent headlines, expectations going into Tesla’s 4th quarter earnings were fairly low. On an adjusted basis, Tesla reported an EPS of $1.19 eps vs consensus of $1.11. With that important hurdle cleared, Tesla’s 2023 outlook was in focus. In a market where companies have been providing dour outlooks based on the macro, there were enough positives to cause us to look closely at valuation.

- 2023 Production of around 1.8m vehicles, in line with Tesla’s 50% long-term CAGR goal

- $20b in cash will allow it to execute its expansion plans during uncertain macro environment

- Although operating margins were down q/q and may stay at these levels in the short term, management stated that the longer-term trajectory was higher as the benefits of greater operating leverage take effect. Even at current levels, Tesla’s current operating margins are 2-3x more than traditional OEMs.

Revenue came in at 37% growth for $24.03 billion total. Automotive growth was 33% for $21.3 billion in revenue. There were regulatory credits of $467 million.

The FY2022 revenue came in at 51% for revenue of $81.5 billion. Automotive also came in at 51% for revenue of $71.462 billion. There were $177 million in regulatory credits.

The company reported EPS of $1.19 in Q4 compared to EPS of $1.05 in the third quarter. The FY2022 adjusted EPS was $4.07. The EPS for next quarter is expected to be $0.87 which is lower than the EPS of $1.07 in the year ago quarter.

It’s true that Tesla’s gross margin was soft at 23.80% with an automotive gross margin of 25.9%. This is 150 bps lower and 200 bps lower, respectively, than the September quarter.

It’s also true operating margin of 16% was weaker by 119 bps from the September quarter of 17.19%. However, it was higher than the June quarter at 15% and higher than the year ago quarter at 14.75%. I would consider this strong with anything below 14% to 15% would be contracting. But, this is where an earnings report becomes subjective – and why a lower valuation is helpful especially if a company is not priced for perfection, and rather, is priced for low expectations.

The adjusted EBITDA margin of 22.2% is on the low side for Tesla in FY2022 as the previous quarter was 23.2% and the year ago quarter was 23.1%. My opinion is that it’s not an egregious contraction (especially having a large cash position) and is noted as something to watch.

The net margin was higher than the September quarter at 16.8% compared to 15.30%. This was also higher than the year ago quarter at 13.10%.

The operating cash flow and free cash flow is where the concern is with this particular earnings report. Operating cash flow of $3.27B was down from $4.58B in the year ago quarter. The Free Cash flow of $1.4B was down 49% YoY compared to $2.775B in the year ago quarter. Both were down sequentially as well with the September quarter reporting Op Cash Flow of $5.1B and FCF of $3.29B.

Looking closer, there were two line items weighing on cash flow:

· Change in operating assets and liabilities at ($2.191) billion

· Purchases of Investments ($4.368)

The change in operating assets and liabilities points toward an increase in inventories and account receivables. Where the bears may have a good point to consider is the inventory supply has been steadily increasing since Q32022. This is reflected in the $2.191B.

Where the bulls may win, is that the typical response to increased inventory is to lower prices. Not only is Tesla going to do this (with the idea it will increase selling volume) but is assisted in doing so with the $7500.

As long as current stockholders understand that this is where the speculations remains – will the lower prices help to lower global inventory and days of supply, and meanwhile, can the management keep operating margin steady while doing so?and meanwhile, can the management keep operating margin steady while doing so?

For the purchase of investments of $4.36B, we may need the 10-Q as there weren’t questions on the call from the sell-side analysts to know exactly what this refers to.

Earnings Call:

Management has stated that operating margin is what to watch:

“The second comment I wanted to make here is that as a management team here, we're most focused on what our operating margin is. And so as other areas of the business become more important, particularly the energy business, which is growing faster than the vehicle business and as we're heavily focused on operating leverage here, improving efficiency of our overheads, we think the right metric for us to be focused on is operating margin.”

Short sellers will certainly ignore this comment, and it’s up to each investor if a consistent operating margin is enough to overlook the FCF this past quarter and the softer gross margin.

The comment that has ruffled some feathers is this from Elon Musk:

“The most common question we've been getting from investors is about demand. Thus far — so I want to put that concern to rest. Thus far in January, we've seen the strongest orders year-to-date than ever in our history. We currently are seeing orders at almost twice the rate of production. So it’s hard to say that will continue twice the rate of production, but the orders are high. And we've actually raised the Model Y price a little bit in response to that.”

The first question on the call questioned if this statement was true or not:

Martin Viecha (moderator)

Thank you very much, Zach. Let's now go to investor questions. The first question is, some analysts are claiming that Tesla orders, net of cancellations, came in at a rate less than half of production in the fourth quarter. This has raised demand concerns. Can you elaborate on order trends so far this year and how they compare to current production rates? I think…

Elon Musk

We already answered that question.

Martin Viecha

Yes, exactly.

Elon Musk

Demand far exceeds production, and we actually are making some small price increases as a result.”

My take: I think they’re talking about two different things here. The question is asking about Q4 and Elon Musk is talking about January. With Q4 behind us, the January comment is more important but there's no evidence to back it yet.

Notably, orders won’t move stock price, rather it will be if Tesla can meet the guide of 1.8M on production, for the 28.8% growth. It was mentioned on the call that Tesla can produce 2M this year barring any unforeseen “force majeure” such as an earthquake or a tsunami.

Secondly, and perhaps most importantly, deliveries are what will also move the price. However, if we assume the January comment is accurate, then production will be equally important this year to meet the demand.

Regarding the operating margin, the company is taking cost reduction efforts. However, the company did state there would be an impact to operating margin in the near term that will level out over the year.

“Second, on cost reduction, we're holding steady on our plans to rapidly increase volume, while improving overhead efficiency, which is the most effective method to retain strength in our operating margins.

In particular, we're accelerating improvements in our new factories in Austin, Berlin and in-house cells, where efficiencies are the highest. But we are attacking every other area of cost and unwinding cost increases created for multiple years of COVID-related instability. This includes logistics, expedites, accumulation of material buffers, part premiums, productivity and overheads as an example […] In that, we've priced our products with a view towards a longer-term cost structure. Thus, there will be an impact on operating margin in the near term. However, we believe our margins will remain healthy and industry-leading over the course of the year.”

It's also important to note that deflationary pressures on Tesla’s supply chain will help the operating margin. The issue that is riling up the bearish thesis is that by cutting prices to $47,000 while the cost of goods (COGS) is at $42,000 will very little margin. Tesla’s answer to this is that COGS should go down as $42K is the peak, and $36K is the bottom, so somewhere in the middle is where it will land this year.

The company is working to optimize the supply chain and to also optimize the vehicle design, such as the powertrain.

Here is what was said on the call:

“And we're gathering a lot of data out of that fleet to understand how we can sort of bring some margin that we didn't know we had out of the product. So, over the course of 2023 on the powertrain side, we're actually going to go after sort of some materials where we're paying for more performance than we need, or we have more content than we need, without impacting reliability at all.”

Valuation:

If I were to choose one thing to talk about with Tesla stock (in a 1-minute elevator ride), it would be the valuation. I do think there’s some weight to the $7500 tax credit and the fact a Tesla will be priced competitively with mid-range sedans, like Toyota or Acura. There are some people who could not afford a Tesla before that now can.

In the face of what I would call a “no bad news is good news” earnings report, it was really the valuation that caused us to enter the stock. If the stock was trading at a more median valuation using 2022 comps, it would have been a harder decision (perhaps we would wait for the Q1 report).

But, with Elon Musk buying Twitter and selling a lot of Tesla stock, the valuation is very low. Even with the current run-up we’ve seen, it remains very low.

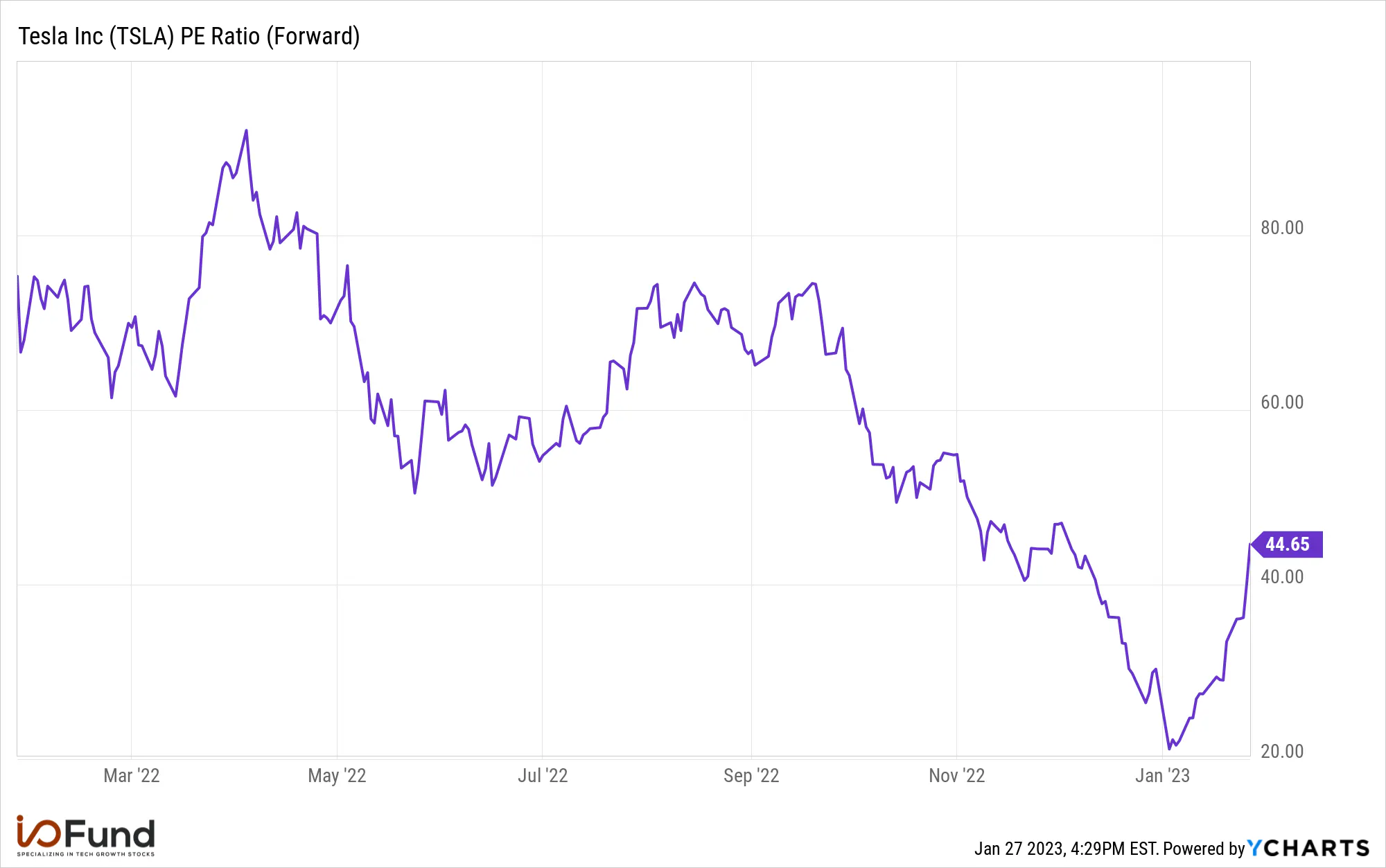

In the tough macro of 2022, Tesla’s forward P/S was between 8 and 11.5. It’s currently at 5.5.

The forward PE Ratio is trading at a 45 forward and traded between 55 forward and 75 forward last year in the tough macro:

Finally, if we look at FCF, it’s trading at a steeper discount as it was at 125 prior to October and is now at a 55 EV/Revenue:

Conclusion:

Over the past few years, Tesla has demonstrated excellent operating leverage. The company has halved its average sales price (ASP) between 2017 and 2022, yet improved the GAAP operating margin from (14%) to 17%. This helps illustrate why a lower ASP may not necessarily weigh on the operating margin. The bull case for Tesla is that the higher volume of sales, optimized supply chains/vehicle design, and deflationary pressure on COGS will improve (and/or sustain) the margins over time.

The bear case is that Elon Musk is misrepresenting January orders, that they’re lowering prices due to competition, and the softer gross margin and low FCF this quarter is forewarning of more margin contraction up ahead.

Investors should be aware it was mentioned in the call that “there will be an impact on operating margin in the near term” from the lower prices. What could offset this is a beat on production and deliveries, which as you know, comes out monthly.