I want to start by saying that Q2 will be lagging when the reports come out (Q2 likely to be low) and the market will be focused on Q3 guidance. It’s not possible for every single company to come in with strong reports, and instead, it’s our job to look for the companies most probable to find their legs again.

The hawkish FED stole the show but there were many headwinds that the tech industry faced – we’ve covered them in great depth including Apple’s privacy changes and supply chains including auto and lower consumer hardware sales (which has a trickle-down effect to ad-tech), plus the Ukraine war.

Even more important for our industry, tech has had to clear eight straight quarters of anomalous conditions with Q2 2022 guidance – notably, the tail spin on the high revenue water mark clears for nearly all companies by Q3 2022.

When we look at which companies are expected to have strong, accelerating revenue from the nadir of Q2, Unity stands out from the data below. We believe there could be early evidence of fundamentals lining up with technicals.

Here’s a brief description from Knox on what he wants to see before we enter Unity as a momentum play – he will post more on the forum tomorrow.

Unity is basing from the May 12th low. Interestingly, as the broad market made a lower low on May 20th as well as June 17th, Unity instead made a series of higher lows.

This is important, because it signals that the ratio of buyers to sellers from Unity’s all time low is shifting. What we need to see is a high volume breakout above $47 to signal that momentum has shifted to the upside, at least temporarily.

What’s worth pointing out is that Unity is currently holding a key support in red on the chart below. This is the 45 degree line (1×1) from the last high before Unity’s blowoff top. Note how price has used this line for key support and resistance since the downtrend began. It’s currently back above this line, which is important for halting the downtrend.

We need to reclaim the 2×1 line in blue, and breakout above the $47 resistance for us to buy. The weakness we are experiencing must hold 1×1 line as well as the May 12th low at $29. If another of these supports fail, we will step aside as the stock could reach new lows.

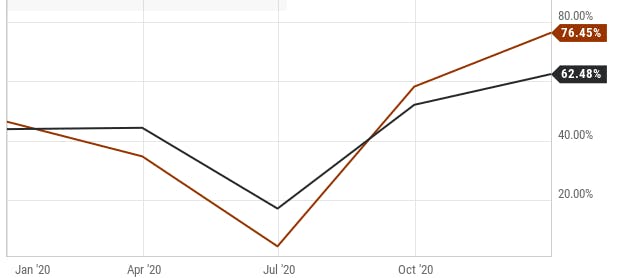

Analyst Consensus Showing Potential Q3 Rebound for Unity

Unity sits at the cross-section of cloud and ad-tech, and thus, it requires two looking at both categories to see the full picture for this company.

When comparing Unity to other cloud stocks, it ranks high for sequential growth from Q2 to Q3 at 17% from $305 million to $355 million, indicating the rebound is one of the best in the cloud category. If we look two quarters out to ensure the rebound is consistent, we see Unity is expected to increase revenue by 36% across two quarters from $305 million to $415 million.

Pictured Above: Unity leads but likely due to headwinds that ad-tech faced.

When we level the playing field and look at ad-tech stocks, which is probably a better indicator considering the transient headwinds facing the ad sector, Unity continues to rank high for the upcoming guide of Q3 yet is not as strong as ad-tech peers for Q4 indicating that two quarters out is when most ad-tech stocks will have rebounded.

Above: Unity leads Q2-Q3 sequential growth in ad-tech

Despite Unity showing a nice rebound for Q3 in analysts’ consensus, the far majority of ad-tech is showing a Q4 rebound:

It’s true that Q4 is affected by the holiday season yet we note many instances below where the growth is much higher between Q2-Q4 this year while these names are selling at much, much lower valuations. Please read the Q4 section below.

Unity has the following analyst consensus at this time:

Q2: +11% growth

Q3: +25% growth

Q4: +30% growth

On the bottom line, Unity expects to be consistently profitable by September of next year (2023). The biggest issue with earnings is also in the Q2 quarter while there’s a noticeable rebound for Q3 and beyond:

Q2: ($0.22) EPS

Q3: ($0.06) EPS

Q4: $0.02 EPS

Ad-Tech Showing a Rebound in Q4:

Unity:

Q3 consensus: +25% YoY growth

Q4 consensus: +30% YoY growth

Sequential growth for two quarters = +36% from $305M to $415M

Roku:

Q3 consensus: +36% YoY growth

Q4 consensus: +43% YoY growth

Sequential growth for two quarters = +55% from $805M to $1.24B

We already own Roku at a high allocation so this helps us keep the position in its current allocation going into earnings. There’s a caveat to Roku which is the hardware weighs on the bottom line but we have repeated (to the point where it’s probably becoming a bit repetitive) that we like it’s position on first-party data and we agree with its investments to strengthen what we’ve called the “Royal Flush” positioning. The company is expected to be profitable again by Dec 2023.

The Trade Desk has a rebound over a six-month period of 43% yet the valuation is quite a bit higher than its peers. There’s a great forum post here on The Trade Desk by a Member who invested in the stock. We love these long-form posts where Members discuss stocks they own outside of our portfolio – keep them coming! ☺

The Trade Desk:

Q3 consensus: +28% growth

Q4 consensus: +31% growth

Sequential growth 2 qtrs: $365M to $522M for 43% sequential growth

Snap’s rebound is slower on YoY basis yet from a Q2 low to a Q4 high in terms of sequential growth, the rebound is similar to its peers. Snap also has the highest revenue with roughly $6 billion in annual revenue compared to ad-tech peers with roughly $2 billion or less in annual revenue.

Q3 consensus: +19% YoY growth

Q4 consensus: +22% YoY growth

Sequential Growth 2 qtrs: +38% sequential growth

Among small caps, PubMatic actually is quite strong off the nadir of Q2:

Q3 consensus: +23% YoY growth

Q4 consensus: +22% YoY growth

Sequential Growth 2 qtrs: $61M to $96.5M for growth of 59%

Magnite is the small cap in ad-tech that we currently own and here is how the company compares. The growth listed is with SpotX.

Q3 consensus: +25% YoY growth

Q4 consensus: +16% YoY growth

Sequential Growth 2 qtrs: $125M to $165M for growth of +32%

This assumes each company will meet or exceed analyst guidance – there is no guarantee this will happen. This assumes each company will meet or exceed analyst guidance – there is no guarantee this will happen. What’s more important than making an exact prediction, however, is that we should be tracking when the rebound is scheduled to occur. We see real evidence of expectations this will occur in Q3. It’s important to remember too that ad-tech is below historic valuations and any improvement in growth will likely see these valuations return to average levels.

Consensus Shows Rebound Even with Q4 Holiday Comps

As stated above, you could argue that sequential growth across two quarters is less relevant considering that Q4 is the strongest quarter for ad-tech.

Here is last year’s Q2 to Q4 growth rates:

Unity: +15% from Q2-Q4 2021 = higher this year at 36%

Roku: +34% from Q2-Q4 2021 = higher this year at 51%

The Trade Desk: +41% from Q2-Q4 2021 = a tick higher this year at 43%

Snap: +32% from Q2-Q4 2021 = a few percentage points higher this year at 38%

PubMatic: +51% from Q2-Q4 2021 = higher this year at 58%

Magnite: +41% from Q2-Q4 2021 with two months of SpotX (lower this year at 32%)

In many cases, companies will bounce back with growth from Q2 to Q4 — yet, these companies were trading nearly 3-4X higher last year.

It should be noted that Unity typically is grouped with cloud for its valuation which is why it’s exceeded 45 forward sales in the past. When we look at the bottom line, it’s the small cap stocks that are most reasonable with Magnite and PubMatic trading in the 12 and 20 Forward P/E range, respectively.

Unity Earnings and Product Overview (Editorial):

Please note: We covered Unity following earnings on May 20, 2022 and have copied and pasted this information below as its current and timely.

Unity has demonstrated strong price action following the IPO last year due to its unique blend of cash efficient ad-tech monetization and near-monopolistic game development platform. The company is well suited for the Metaverse and industrial 3D worlds due to its history of supporting 3D game development.

In previous earnings calls, the management was confident they would not be affected by Apple’s IDFA changes or the other road blocks that caused ad-tech companies to lower guidance across the board. Unity’s confidence primarily came from their contextual ad positioning as compared to direct response. Therefore, there was high confidence going into earnings yet management delivered a sizable revenue miss due to a product mishap.

Unity previously guided for revenue growth of 36% for full year 2022, which would put the company as the leader in ad-tech growth and mid-range for cloud. In the recent call, the company lowered this guidance to 26% at the mid-point for a negative impact of $110 million. Guidance for Q2 2022 was at 7% at the midpoint, which would put Unity in the lowest quartile for ad-tech on growth and certainly for cloud. The stock dropped 35% following the announcement.

The surprise miss in revenue guidance was due to the company’s product Audience Pinpointer, which is a machine-learning powered user acquisition tool that allows game developers to acquire players based on a targeted return on their spend. Unity’s training data was also affected by ingesting bad data from a large customer. This led to Unity noticing less revenue coming from their monetization platform, and as advertisers saw less performance, they began to spend less.

Below, we weigh the pros and cons of an otherwise solid game engine and Metaverse stock.

Unity Has 2.8 Billion MAUs

Despite the temporary mishap with Audience Pinpointer, Unity has significant proprietary data and insights to feed contextual models. Unity is a game engine where more than 2.8 billion monthly active users (MAUs) play games or apps built on Unity compared to Facebook’s 2.9 billion monthly active users. The total addressable market for gaming exceeds 4 billion MAUs and Unity serves 61% of game developers.

It’s not exactly apples-to-apples with Facebook as Unity powers the games and is not a publisher like Facebook, yet it illustrates the scale the company is capable of. In the game development ecosystem, 72% of the top 1000 mobile games are made on Unity’s platform. There are 5 billion monthly app downloads.

Part of Unity’s substantial presence is the free tools it offers game developers who earn less than $100,000 annually, and for the most part they capture any developer between the indie (small) stage and up to AAA studios although many of these studios prefer to use their own in-house game engine. The company has especially found its stride on mobile.

Unity offers its products under two platforms, Create Solutions and Operate Solutions. The Create platform is used to create, edit and run 3D content. The Operate platform is used to grow and engage the user base and to also monetize content. The company derives 93% of 2021 revenue from these two platforms with a split of 64% Operate and 29% Create.

Create Solutions is where games are built and Operate Solutions is how games are monetized through ads and in-app purchases. There are also analytics offered through DeltaDNA, which collects information on end-user engagement and behavior.

Operate is successful through contextual ads rather than behavioral targeting, which has made the company resilient during Apple’s privacy changes.

Prior to Apple’s iOS changes, we had stated the following in September of 2020 in a note to our research customers:

On a contrarian note, because Unity has a very specific content type (gaming), there’s a chance the company is very resilient through the iOS 14 changes as targeting can occur through content type (i.e. Gaming, Financial News, Beauty & Health, etcetera). Previously, Unity Ads have been known to be more effective because the audience type and interests are narrow. There’s also a possibility that Unity is stronger with the IDFA changes as they own the game engine whereas their competitors are using third-party data only for targeting. These competitors include Vungle, AdColony, Facebook’s Audience Network, MoPub, Leadbolt, TapJoy, etcetera.Unity has a very specific content type (gaming), there’s a chance the company is very resilient through the iOS 14 changes as targeting can occur through content type (i.e. Gaming, Financial News, Beauty & Health, etcetera). Previously, Unity Ads have been known to be more effective because the audience type and interests are narrow. There’s also a possibility that Unity is stronger with the IDFA changes as they own the game engine whereas their competitors are using third-party data only for targeting. These competitors include Vungle, AdColony, Facebook’s Audience Network, MoPub, Leadbolt, TapJoy, etcetera.

Notably, Unity’s revenue miss was unrelated to Apple’s IDFA changes and was instead related to the company’s internal product Audience Pinpointer.

The Metaverse Opportunity

Developing games on Unity is low code and sometimes no code, which is ideal for 3D creators who are not necessarily developers. This lends itself well to the creator community that is most likely to drive forward the Metaverse, or Web3, and also the various industries that can benefit from 3D or AR/VR right now. The Create Solutions and tools are also great for prototyping, which speeds up the time to deployment. Unity is frequently acquiring tools and plugins to lower the barrier of entry for developers and creators. For example, Bolt2 helps developers implement logic without knowing how to code.

Last year, Unity developed a new architecture that provides native APIs to third-party providers and offers a high-level managed API to Unity developers. The new architecture fundamentally improves how Unity delivers and manages SDKs for XR platform integrations.

With Unity Pro, real-time 3D, AR and VR content can also be deployed on HoloLens and Oculus. The Unity Pixyz Plugin works with manufacturing software like AutoDesk to further industrial uses, such as automotive. Additionally, Unity does not compete with creators and is royalty-free.

The main thing to know about Unity’s products is they offer 3D creation for everyone, i.e., democratizes the process. This was initially intended for the gaming industry yet there is a natural affinity for gaming tools, IDEs, chips, etcetera, to be used for virtual worlds and the Metaverse.

The management had mentioned in the earnings call that the company was able to expand its market share in gaming and AR/VR. The company’s non-gaming business outpaced gaming business revenue as it grew 70% year-over-year. Digital twins and the metaverse are a substantial opportunity with 34 deals closed in the current quarter over $100,000, up 126% YoY.

Unity bought Weta Digital for $1.62 billion in exchange for the design tools, assets and data platform that drove film creations such as Lord of the Rings, Avengers, Avatar, and Game of Thrones. The goal is to bring the magic of film assets to the individual creator on Unity’s platform. It will also help the company to remain competitive against Epic’s Unreal Engine.

We had stated the following in a private note to our research customers when Unity acquired Weta:

“The Weta Digital acquisition helps Unity remain defensive against Epic’s Unreal Engine, which was used on virtual sets, such as Star Wars The Mandalorian. It also helps Unity build a Metaverse asset library, such as stadium scenes, character movements, large crowds, fantastical characters and backgrounds, etcetera, which can help the workflow for content creation for the metaverse. With that said, the more near-term opportunity for these acquisitions is for Unity to turn Hollywood into a customer.”is for Unity to turn Hollywood into a customer.”

Earlier this year, the company acquired Ziva Dynamics, the film software used for creating digital humans in Marvel movies, Hellblade, Jumanji, and Godzilla vs King Kong. In the recent quarter, the company received more than 8,000 sign-ups for the cloud uploads of beta version of Ziva Faces. Accroding to CEO John Riccitiello, “This service enables artists to use advanced machine learning models and massive data to train meshes for full expressiveness, instead of requiring teams of artists to spend weeks doing manual rigging.”

The company’s addressable market is growing and the management had mentioned in the last earnings call that the total addressable market for Create Solutions and Operate Solutions is $45 billion, up significantly from $29 billion during its IPO in 2020. The growth in the addressable market was due to the additions of new products and acquisitions.

Financials and Audience Pinpointer Issues:

The company finished the year 2021 strong with revenue growing 44% YoY to $1.1 billion and adjusted operating margins improved 200 bps to -4.6%. As a percentage of revenue, R&D is at 69%, which is slightly higher than it’s been in previous quarters. Expenses are frontloaded at the beginning of the year with the company expected to break even by 2023.

Q1 2022 revenue grew by 36% year-over-year to $320.1 million, which missed analyst consensus estimates by -0.32%. The company’s dollar-based net expansion rate came in at 135% compared to 140% in the same period last year and Q4 2021.

Unity’s management guided for revenue growth of 7% at the mid-point for Q2 2022. This was a stark surprise and lower than the 48% growth reported in Q2 2021. For the full-year, it has guided revenue growth of 26% at the mid-point which was lower than the earlier forecast of 36% provided during the year-end results.

The management mentioned in the earnings call that it was mainly due to two issues. According to John Riccitiello, CEO, “The first was a fault in our platform that resulted in reduced accuracy for our Audience Pinpointer tool, a revenue expensive issue given that our Pinpointer tool experienced significant growth post the IDFA changes. The second is that we lost the value of a portion of our data, training data due in part to us ingesting bad data from a large customer.”

Audience Pinpointer is a user acquisition product that is based on machine learning which helps game developers to acquire users based on a certain return on spending. The management expects these issues to be partially recovered in the third quarter and fully recovered by the end of the year. They reassured analysts on the call that there will no negative impact on the revenue for the year 2023.

As we had expected, the company was able to overcome the challenges of Apple’s iOS changes and the deprecation of the IDFA since a majority of games are built with Unity engine and analytics per the company saying: “Pinpointer tool experienced significant growth post the IDFA changes.” The CEO also stated, “We have proprietary data and insights coming from our reach to over three billion monthly active users feeding our contextual models. We have deep context, about game play, what players like to play, when and how they play games. And in gaming, this data has proven to be the most relevant for advertising.”

The management remains confident in the long-term opportunity. They estimate that there are more than four billion monthly active users and that less than 3% of users pay for games.

The company’s Create solutions is doing well and accelerated by 65% YoY to $116 million. This was driven by the strong adoption of real-time 3D. In the Content Solutions segment, some of the notable business use cases of big publishers include, “Angry Birds brought back Angry Birds Classic to mobile app stores using Unity to relaunch this treasured game and easily make it work across multiple modern devices. And Ubisoft used Unity to deliver incredible visuals and fast gameplay in Rainbow Six Mobile.”

The adjusted operating margin improved 280 bps to -7.2% which is lower than FY2021. The company had free cash flow of $86.4 million. However, the cash flow included the license fees for four years of $200 million relating to Weta FX.

Looking forward the management reiterated that it expects revenue to grow above 30% in the long-term. It also expects to be profitable in the fourth quarter of this year.

Conclusion:

Unity Software is the market leader in the fast-growing gaming industry. The company’s future growth opportunities extend beyond gaming to include industrial real-time 3D and the Metaverse. Due to its proprietary data from 2.8 billion MAUs and contextual targeting, Unity will likely come out stronger than other ad-tech companies following Apple’s privacy changes (and Google’s upcoming privacy changes circa 2023).

The market has been extraordinarily temperamental towards tech stocks and this is likely to be one of many instances where the current (low) stock price does not fully reflect the opportunity.