This article was originally published on Forbes on Forbes Forbes on Mar 14, 2024,07:01pm EDT

Ad spending growth is widely forecast to accelerate in 2024, after a challenging macro environment significantly dented budgets and growth in 2023. The US advertising market is already showing positive signs of growth, starting off 2024 with a 4.3% YoY increase in January, the strongest January on record and a tenth straight monthly increase.

We’re tracking ad-tech at the moment for three key reasons: a robust ad market backdrop with multiple major event tailwinds, strong cash flow generation, and improvements in operating leverage. We’ve previously covered the 2024 outlook for four major digital advertising verticals in our analysis “Ad Spending Growth to Accelerate In 2024” at the end of December; now, we take a look at three of the advertising industry’s top stocks: Meta, The Trade Desk, and Alphabet.

Meta: The Juggernaut Has Returned

The Juggernaut is back — Meta has been the second-best performing stock of the Magnificent 7, with its 44% return since the end of 2021 and a 301% return since the end of 2022 beaten only by Nvidia. This rally has been supported by significant improvements in operating leverage as revenue growth has reaccelerated to the mid-20% range.

Meta has stood out amongst social media peers for its strong growth in ad impressions, a recovery in ad pricing, and its ability to generate strong cash flows while still spending tens of billions on R&D. We’ve tracked Meta’s strong ARPU acceleration, but the more impressive (and arguably more important) story for Meta is how this translates into a substantial degree of operating leverage.

Meta’s operating margin expanded over twenty percentage points YoY to 40.8% in Q4, returning to a margin not seen since Q1 and Q2 2021. FY23 operating margin improved 990 bp YoY to 34.7%, with room for improvement in FY24. This is helping drive a strong improvement in the bottom line, with Meta reporting a net margin of 34.9%, a second straight quarter above 33% and a strong 2040 bp YoY expansion. Improvement from the 2022 bottom in fundamentals is easily visible in the chart below.

The rebound in leverage comes despite Meta pouring tens of billions into Reality Labs – operating loss for Reality Labs totaled ($16.1) billion for FY23, or a massive ~1195 bp headwind to operating margin.

Sign up for I/O Fund's free newsletter with gains of up to 221% – Click hereClick hereClick here

Meta’s Momentum to Continue in 2024

Meta’s momentum with strong revenue growth is expected to continue in 2024, supported by ARPU trends. In addition, the implementation of AI features, a favorable ad market backdrop, and improving operating leverage supports substantial EPS growth this year.

Meta guided for a very strong Q1, calling for 24.8% YoY growth, a third straight quarter with growth >20%, though it comes against a weak 2.6% YoY comp. Accelerating ARPU in Facebook’s two core geographies, the US/Canada and Europe, supports this revenue growth story.

Source: Meta

Also supporting the growth story is a favorable social media ad spend backdrop, as well as major political and sporting events, namely the US presidential election in November and the Summer Olympics. Globally, social media ad spend has one of the fastest projected growth rates in the ad industry at +13.8%.

In the US, growth is expected at a similar rate, with Insider Intelligence projecting 13.5% YoY growth to $82.9 billion. This represents a $7.8 billion increase from their Q1 2023 forecast, with the market benefiting from “higher ad loads, a focus on lower-funnel ads, and an improved advertising economy,” driven by both Meta and TikTok.

For 2024, key metrics are supporting a return to >40% operating margin for the full year and a possible >33% net margin, driven by increasing ad pricing, strong engagement trends and impressions growth, aided by the release of numerous AI features. Reaching those margins for the full year would imply EPS growth of nearly 38% to $20.50 on $160B in revenue. Meta would be trading at a 24x forward PE ratio under that EPS growth assumption, 15% cheaper than its 5-year average PE of 27x; however, this is the peak multiple we’ve seen so far in Meta’s rally.

The Trade Desk: CTV Tailwinds Offer Growth Outlet

The Trade Desk, which offers a cloud-based digital advertising purchasing and optimization platform for advertisers across many mediums, from CTV to display, audio, digital out-of-home, and more, continues to be one of the fastest growing ad-tech stocks in the industry. Revenue grew 23% in FY23 to $1.95 billion, outpacing a tepid ad market but representing a 9 percentage point deceleration from 32% revenue growth in FY22.

Though revenue has decelerated, profitability has remained solid, and GAAP net income more than tripled YoY to a nearly 10% margin this year, though that is much lower than historical levels. Operating income is showing signs of stability and improvement on a TTM basis, after periods of volatility in 2021 and 2022.

The Trade Desk's operating income has quadrupled from $50 million in early 2017 to $200 million in2023 despite a deterioration in operating margin. Source: YCharts

Despite a steady deterioration in TTM operating margin over the past six years, from the 30% range to the 10% range in FY23 (after briefly dipping negative), operating income has grown, in fact it has quadrupled from $50 million in early 2017 to $200 million in 2023.

The challenge now for The Trade Desk is maintaining this more rapid trajectory in operating income growth through 2024 and into 2025 given that revenue growth is expected to decelerate. This will be critical in driving expansion in GAAP net margin, which hovers just below 10% currently, compared to above 15% as it had maintained for more than three years.

The Trade Desk's net profit margin hovers just below 10% currently, compared to above 15% as it had maintained for more than three years. Source: YCharts

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.Learn more hereLearn more here.

CTV, Kokai Provide Growth Opportunities in 2024

CTV ad spend and the ramp of The Trade Desk’s new AI-powered buying platform Kokai offer two potential growth outlets for 2024.

CTV ad spend is forecast to be digital advertising’s fastest growing channel this year, with Dentsu placing growth at 30.8%, while BIA is expecting growth as high as 39.5%. CTV ad spend in total has surged 400% since 2019, as use of streaming services soared through 2020 and 2021; now, rising adoption for major streamers’ ad-supported tiers beckons to bring more spend through CTV. This trend bodes well for The Trade Desk, as CTV “continues to be the fastest-growing channel at scale” for the company, as it sees that “ad supported streaming is going to be an essential strategy for any successful TV provider moving forward.”

Kokai, which launched in June 2023 as The Trade Desk’s AI-powered buying platform, has been labeled by CEO Jeff Green as the “largest platform overhaul” in its entire history. Kokai will be scaling throughout the year, and promises a new degree of optimization for ad buyers while providing KPIs throughout the entire funnel, instead of simply at the last click. In essence, The Trade Desk sees Kokai as an “upgrade in almost every way” to its existing platform.

Though determining the growth trajectory of Kokai over the next few quarters may be challenging, tracking gross spend and The Trade Desk’s take rate provides insights into revenue acceleration trends, and if Kokai and a strong CTV ad market are driving an acceleration in spend and improvements in take rate.

Source: The Trade Desk

The Trade Desk’s take rate has fluctuated between 19% and 21%, hovering around 20.3% in FY23. While it may seem obsolete to track a metric that fluctuates within a tight 200 bp range, the impact of a 100 bp change in take rate is actually quite large. Take FY21 as an example, when The Trade Desk recorded its lowest take rate at 19.4% — had this been 100 bp higher at 20.4%, revenue growth in the year would have been 700 bp higher, at 50% versus the 43% reported growth.

If gross spend can accelerate via a robust CTV market and Kokai’s improvements and efficiency gains for buyers, maintaining a take rate above 20% or driving growth to above 20.5% can help revenue growth accelerate to the high-20% range. However, the upcoming phase-out of cookies provides a significant risk to take rate, in that if The Trade Desk fails to get significant adoption of UID 2.0, which is the second most-used cookie replacement, it may struggle to command such a high take rate due to a loss of targeting ability in a cookie less digital environment.

Alphabet: Beneficiary of Search, CTV Ad Spend

Alphabet is a beneficiary of both search and CTV ad spend, and has seen growth accelerate this year as it works to integrate generative AI features and AI-based tools to drive improved ROI for advertisers – Alphabet recently reorganized its digital ad business to place more emphasis on generative AI and AI automated ads.

Alphabet reported $65.5 billion in advertising revenue, up 11% YoY, its first double-digit growth rate in six quarters, driven by strength in Search and YouTube. Alphabet has nearly doubled its quarterly run rate in just four years.

Source: Alphabet

Search and YouTube ad revenue growth accelerated in each quarter this year, from the low single-digits to 12.7% and 15.5% in Q4 respectively. What Alphabet is demonstrating is that AI-powered ad solutions are helping drive resilient Search ad revenue growth, at the same time that strong engagement metrics for YouTube Shorts (>2B MAUs, 70B daily views) and increasing watch times for YouTube TV are boosting YouTube’s ad revenue growth.

Source: Alphabet

AI Integrations Provide Opportunity for Growth

Alphabet is steadily making progress in integrating AI features in Search via Search Generative Experience (SGE) and in advertising campaigns via Performance Max (PMax). Executives have previously mentioned how these “AI-powered solutions like Search and PMax are helping retailers drive reliable, strong ROI and meet customers wherever they are across the funnel.” This is the value-add of SGE and PMax – driving CPM higher from via higher ROIs from improved targeting and optimization, while letting Alphabet toy with new ad placements and formats in Search pages. Alphabet sees “significant opportunities” to “actually deliver incredible ROI at scale” from these AI-powered features.

Alphabet’s Demand Gen is instrumental in driving long-term growth momentum across its more than 3 billion monthly active YouTube and Gmail users. Alphabet explains it as its “big bet to help social advertisers find and convert consumers via immersive, relevant, visual creatives” across these channels. Alphabet shared some color on Demand Gen in Q4, saying that “tens of thousands of advertisers are testing and, on average, seeing 6% more conversions per dollar versus image-only ads in Discovery campaigns.”

Gemini is also playing a more forward facing role in advertising products, powering Alphabet’s new conversational features in Google Ads. While it is still in beta in the US and UK, early tests have shown “advertisers are building higher-quality Search campaigns with less effort,” streamlining the campaign building process.

Cash is King

As the saying goes, cash is king, and Meta, Alphabet, and The Trade Desk stand out for strong cash flow generation metrics. Meta leads the Magnificent 7 with a nearly 53% operating cash flow margin, while The Trade Desk and Alphabet command OCF margins in the low-30% range.

To put how strong this cash flow generation is in perspective, Meta and Alphabet have grown operating cash flow 1,400% and 425% respectively. This is incredibly impressive given the scale of the duo’s cash flows, with Meta generating $71 billion and Alphabet $101 billion.

Conclusion

Ad-tech stocks are on 2024’s watchlist for a few reasons: strong cash flow generation and growth, a positive ad-market backdrop buoyed by major political and sporting events, and implementation and integration of AI features to help drive improved ROI for advertisers. Meta, Alphabet and The Trade Desk look best positioned to capture and capitalize on the ad industry’s acceleration this year.

My firm is not buying these stocks at the moment as we believe we can get them lower than where they’re currently trading. Though Meta is trading lower than its 5-year average PE ratio, it’s at the peak level sustained so far during 2023’s rally, leaving less room for upside. On the top line, it trades at a 9.6 with 11 being the highest its traded since 2019 (the stock was valued at 11 during Covid when ad-tech was surging from high social media use). The 3-year median is 6.4 and the 5-year median is 8.3.

Alphabet is the cheapest of the Mag 7, trading at a 20x forward PE although EPS growth is expected to be more tepid at just 17% this year, versus 38% for Meta. The company is trading right at its 3-year median and 5-year median on a PS ratio. Some of the softer price action could be due to the anti-trust lawsuit which has closing arguments set for May.

The Trade Desk is more expensive than the two on the bottom line, trading at 123x forward earnings, although it is expected to deliver 82% growth to $0.66 in GAAP EPS. Its trading at it’s 3-year median and 5-year median with a PS ratio of 20.6.

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

I/O Fund Equity Analyst Damien Robbins contributed to this report.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

This article was originally published on Forbes on Dec 27, 2023, 07:15 am ESTForbes Forbes on Dec 27, 2023, 07:15 am EST

Ad-tech stocks have generally enjoyed strong returns in 2023, buoyed by a rather fierce tech rally. Ad spending growth showing initial signs of stabilizing in the back half of the year, with ad spend growing YoY in each month from July to October.

Ad spending growth is widely forecast to accelerate in 2024, after a bumpy start to 2023 stemming from macro uncertainty as growth forecasts were pulled lower mid-year. The market looks to be cheering on a return to higher growth in 2024, along with new synergies from generative AI advertising offerings from Big Tech and pockets of stronger growth in digital and retail media ad spend.

Lower budgets in 2022 and early 2023 affected nearly every ad-tech stock, including companies that draw audiences in the billions – on a three-year basis, only three of ad-tech’s primary names have a positive return: The Trade Desk (TTD), Alphabet (GOOG), and Meta (META), and the latter two only recently broke back into positive territory. The rest of the sector is still struggling to cope with a significant slowdown in growth, from 19.6% in 2021 to the low single digits in 2023.

Sign up for I/O Fund's free newsletter with gains of up to 221% – Click hereClick hereClick here

Growth Forecast to Gain Steam

Growth forecasts from Magna, Dentsu and GroupM generally point to an acceleration next year, at around 5.7% on average between the three, compared to 4.7% in 2023.

Source: I/O Fund

Dentsu is projecting 4.6% YoY growth in 2024, almost 2 percentage points higher than its final 2.7% growth forecast for 2023. This outlook is positively impacted by stronger growth in CTV, digital and retail media ad spend. However, Dentsu sees media price inflation contributing 2.1 percentage points of growth in 2024; stripping out that effect, global ad spend is expected to increase just 2.5% YoY, a slight deceleration from 2023. media price inflation contributing 2.1 percentage points of growth in 2024; stripping out that effect, global ad spend is expected to increase just 2.5% YoY, a slight deceleration from 2023.

Magna tends to lean more bullish in its forecasts compared to Dentsu, projecting 5.5% growth in 2023 and a 1.7 percentage point acceleration to 7.2% in 2024. Magna’s outlook is boosted by “economic stabilization and lower inflation,” themes that have been broadly supported by a slew of macroeconomic data over the past two months. Magna and Dentsu both see positive effects from political spend, and major sporting events including the UEFA EURO 2024 and the Summer Olympics.

GroupM is forecasting a 0.5 percentage point deceleration to 5.3% growth in 2024, with this weaker outlook driven primarily by “uncertainty in some markets and interest rates.” Despite the weaker forecast, GroupM is more positive on retail media ad spend, similar to Dentsu, seeing the segment growing 8.3% in 2023.

Below, we will take a look at some of the dominant names across four major digital advertising categories: search, social media, streaming/CTV, and retail media for more color on the ad industry in 2024.

The I/O Fund provides entries and exits through real-time trade alerts for the stocks the portfolio owns. The team is ramping our analysis for our 2024 portfolio now. Learn more here.here.

Search Ad Spend to Decelerate, But AI Showing Promise

Search ad spending is projected to decelerate in 2024, dropping from an expected 12.5% in 2023 to a projected 9.5% next year as advertisers shift dollars to other mediums, primarily social media and CTV. Even with this deceleration, search ad spend is still projected to outpace global ad spend’s growth.

Google has seen Search revenue growth accelerate in each quarter this year, from just below 2% in Q1 to 11.3% in Q3 – the highest growth in five quarters driven by retail vertical growth. What Google is showing in Q3, and likely in a similarly strong Q4, is that AI-powered ad solutions are helping drive resilient Search ad revenue growth.

Google is rolling out AI-driven features and is now reorganizing its digital ad business to place more emphasis on generative AI and AI automated ads. SVP Phillip Schindler explains that these “proven AI-powered solutions like Search and PMax are helping retailers drive reliable, strong ROI and meet customers wherever they are across the funnel.” Increased ROI and improved targeting help keep advertisers engaged and could potentially draw some additional advertising spend to Search.

Source: I/O Fund

We discussed in the past how Google is on the precipice of a multi-decade disruption driven by generative AI: Google is showing early promise with Search Generative Experience (SGE), while Microsoft is actively deploying generative AI to search via Bing Chat.

Deploying generative AI search experiences opens the door for different ad formats and placements, as well as an increase in surfaced links and content. AI can also drive help revenues higher from bid optimization. Google’s AI campaigns, including Performance Max and Smart Bidding, are tapping AI and machine learning tools to analyze millions of data signals to better predict future ad conversions and improve bidding performance.

Today, Google dominates the search advertising market, with estimates placing the giant holding over 60% of the market, however, anti-trust risk is still present for Google as regulators seek to determine if the company has been engaging in anti-competitive behavior across its search engine and demand-side platform (DSP).

For a deeper dive into Alphabet and how the Search giant is entering its Year of Execution, read more here.here.

Social Media Ad Spend Remains Robust

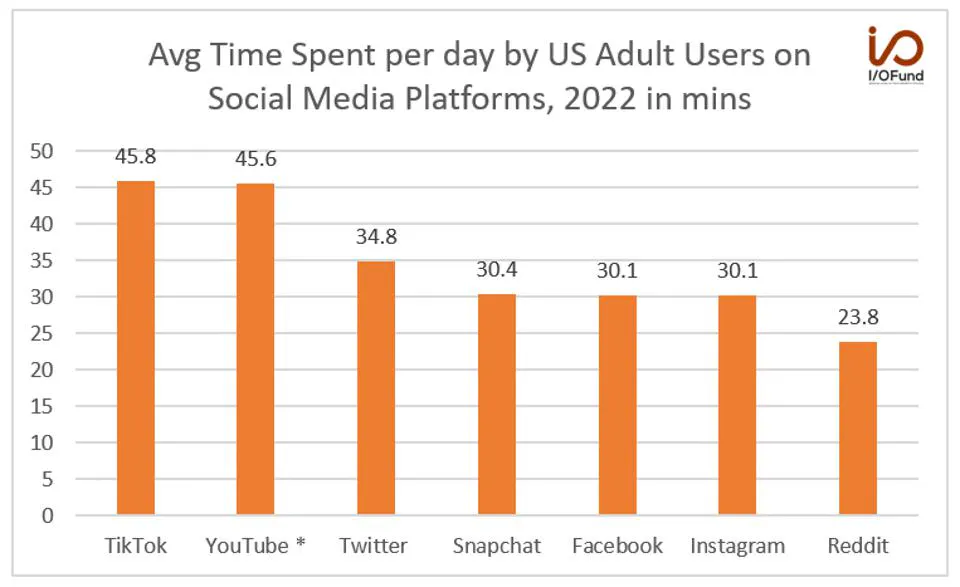

Social media ad spend is expected to remain robust in 2024, and may potentially overtake search ad spending this year, according to estimates from WARC. This medium will enter 2024 with one of the fastest projected growth rates at +13.8%, with spend estimated to climb to $227.2 billion, or less than 1% below search advertising’s $229.2 billion.

Social media’s share of total daily time spent on the internet remains above 35%, at more than 2 hours and 20 minutes per day on average. Combine that with billions of MAUs across the most popular platforms, and it’s easy to see why social media continues to be a popular place to park ad dollars.

Meta dominates the market with more than 60% share and has shown positive trends heading into the end of 2023 that are likely to carry over into 2024. Advertising revenues rose 23.5% YoY to $33.6 billion in Q3. This was driven by 34.2% growth in Europe to $7.77 billion as ARPU rose 33.8%, and 16.8% growth in US and Canada to $15.19 billion.

Pinterest (PINS) and Snapchat (SNAP) also mirror the trend of strong European growth, with Pinterest reporting European revenues rising 33% to $618 million as ARPU increased 26% in Q3. Pinterest said that its shift to Direct Links generated “88% higher outbound click-through rates and a 39% decrease in cost per outbound click for CPC objectives” for early adopters.

Snapchat’s European revenues rose 19.6% as ARPU rose 15.3%, the slowest of the three but much quicker than its overall revenue growth of 5.3%.

Source: I/O Fund

There are two factors currently driving this strong increase in revenues, especially for Meta – a surge in ad impressions to >30% YoY growth, and a recovery in ad pricing, which is nearing an inflection back to growth after declining throughout 2022 and 2023 to-date.

Engagement trends also remain positive, from both a user and advertiser standpoint. Meta noted that “AI-driven feed recommendations continue to grow their impact on incremental engagement,” driving a “7% increase in time spent on Facebook and a 6% increase on Instagram” this year.

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.Learn more hereLearn more here.

Streaming/CTV to See Double-Digit Growth

With 91.8% of internet users between ages 16 to 64 watching content via streaming services, it’s easy to see why advertisers are favoring CTV and YouTube over linear TV. CTV ad spend has risen 400% since 2019, as use of streaming services surged through 2020 and 2021, while linear TV spend has been declining. CTV ad spend is forecast to be the fastest growing channel next year – Dentsu places growth at 30.8%, while BIA expects growth as high as 39.5%.places growth at 30.8%, while BIA expects growth as high as 39.5%.

Major streaming providers had expanded into ad-supported tiers, which are demonstrating both strong growth and strong ad revenue generation. Netflix’s ad-supported tier accounted for 30% of all sign-ups in September and now accounts for ~6% of all US subscribers, per Antenna.

Netflix is projected to reach $1.03 billion in ad revenue in 2024, an estimated 50.3% increase from ~$684.6 million in 2023, according to Insider Intelligence.

Disney+ is expected to see a slower ramp in ad revenue, with a projected 16.1% increase to $911.9 million in 2024 followed by a 20.2% increase in 2025.

Amazon is rolling out its ad-supported Prime Video tier next year, and is projected to generate $3.13 billion in CTV ad revenue, topping Roku to become the third-largest CTV ad platform.

YouTube is also sharing in these gains, with ad revenues rising 12.5% to $7.95 billion in Q3, the fastest growth rate in six quarters.

Source: I/O Fund

Although Roku saw strong contributions from video advertising, it added a bit a caution on the market, saying that the “macro environment continued to pressure the overall U.S. advertising market” in Q3. Roku sees video ads continuing this trajectory in Q4 as it witnesses positive ad momentum driven “in part by diversifying demand sources of advertisers on our platform and expanding partnerships.”

The Trade Desk CEO Jeff Green summed up the CTV opportunity perfectly: “‘Executives at every major streaming giant with both an ad-supported and an ad-free tier, (including Disney, Netflix, Paramount, Warner Bros Discovery and NBC Universal) say that total revenue per user is higher on the ad-supported plan than it is on the ad- free plan.’ Not only do media companies generate more revenue per user within an ad supported option, but the potential for growth is much greater. Ultimately, there’s a limit to how much viewers will spend on subscriptions. Economic pressures on the consumer, right now, are increasing the appeal of a free or low-cost option, that is supported by ads. However, this model is only sustainable if the ad load is significantly lower than traditional linear TV. And the only way we get there is if the ads are relevant to the viewer, so that advertisers are willing to pay more for each of them.”

Retail Media Emerging as One of the Fastest Growing Categories

Retail media ad spend is quickly emerging as one of the fastest growing digital ad categories — US retail media ad spend is forecast to grow nearly 23% next year to more than $55 billion before almost doubling by 2027. Globally, retail media ad spend is expected to increase 10.4% to $141.7 billion, driven by this US growth. Amazon and Alibaba are a dominant duo in this market, with nearly 70% estimated share in 2023, but Walmart, Etsy, eBay and other retailers and e-commerce platforms share in the gains.

Retailers and advertisers are prepping for a longer and stronger holiday season, with holiday spending on the rise despite weaker consumer sentiment. Amazon is “still seeing a lot of strength in the lower-funnel ad products like sponsored products,” even as companies remain a bit more cautious on upper-funnel ads such as display and video.

Amazon’s ad revenues grew 26% YoY in Q3 to more than $12 billion, setting up for a potential $14 billion quarter in Q4 with supporting seasonal strength. For 2024, Amazon is expected to drive a majority of the market’s growth, as it is forecast to see ad revenues rise 16.7% from $45.4 billion to $52.7 billion. Amazon’s Q4 and Q1 ad revenue growth will give a clue into how retail ad spend growth may unfold.

Source: I/O Fund

Other benchmark companies are showing similarly strong trends: Meta noted that its “online commerce vertical was the largest contributor” to growth in Q3, while its AI tools for Advantage+ shopping campaigns “reaching a $10 billion run rate” with more than half of its advertisers using those tools.

2024 Outlook

2024 is widely expected to see an acceleration in ad spending, with major sporting events and political spend aiding the growth forecast. Retail media is expected to see 23% growth in the United States as it begins to shift to other mediums. CTV’s rapid growth outlook of 30% to 40% is boosted by major streaming media companies introducing ad-supported tiers. CTV ads are currently expected to be the strongest growing segment of the four covered here.

Although search ad spending is forecast to soften, Google’s reorganization of its digital ad business to further integrate and utilize generative AI shows promise in reinvigorating growth. Social media ad spend remains robust, and improving pricing trends combined with strong impression growth and AI opportunities could send growth higher next year.

Macro uncertainties are not completely out of the picture. 2022 and early 2023 saw ad-tech stocks get pummeled as growth slowed dramatically from macroeconomic headwinds, so a resurgence of economic growth concerns and any potential budget optimization trends among major advertisers could dent the strong returns enjoyed by a plethora of ad-tech stocks this year. What’s most important to remember is that ad spending can be paused very quickly or resumed quickly, and so this sector is known for sharp moves. We continue to monitor this sector as we build our 2024 portfolio.

I/O Fund Equity Analyst Damien Robbins contributed to this report.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

Adtech has seen extreme volatility over the past few years with Covid causing some stocks to see 1,000% gains in a brief period of time between 2019-2021, and then plummet by up to 80% in 2022. For the current year-to-date, many have rebounded despite reporting depressed growth levels.

Below, we review the stocks in the ad-tech sector to find out which companies have performed well in the recent quarter results and which companies stand out in revenue growth estimates, profits, cash flows, earnings surprise, and we also look into management insights.

Pictured Above: Ad-tech returns from Jan 1, 2022 to Dec 31, 2022. Source: YCharts

Pictured Above: Ad-tech returns since Jan 1, 2023 Source: YCharts

Top Ad-Tech Stocks with the highest revenue growth rates in Q1

Source: YCharts

Unity sits at the cross-section of cloud and ad-tech. The company’s revenue grew by 56% YoY to $500 million in the recent quarter, however, the revenue was down (2%) YoY on a pro-forma basis to reflect the ironSource merger that was completed in November 2022. The company beat its own guidance of $470 million to $480 million and the analyst’s revenue estimates by 4.3%.

Unity’s guidance for the next quarter is $510 million to $520 million, representing a YoY growth of 72% to 75% and 6% to 8% YoY on a pro-forma basis. Management is expecting the overall advertisement sector to be flat QoQ. Per the macro-outlook, they are still cautious, as the company’s CFO Luis Visoso said in the earnings call that “the economic environment is still volatile and uncertain.”

Perion Network is a small cap ad-tech stock with a market cap of $1.4 billion that has sustained a stronger bottom line than its peers. We covered this stock here. Revenue grew 16% YoY to $145.2 million. Management stated the company is likely to raise its revenue growth in 2023, when CEO Gerstel stated: “Given our current visibility, and the sustainability and predictability of our business model, we feel confident in raising annual guidance for the full year 2023.”

The company’s new 2023 revenue guidance is $725 million to $745 million, representing YoY growth of 15% at the mid-point, up from the previous guidance of $720 million to $740 million.

Quarterly Revenue Surprise.

Source: YCharts

Fubo beat analyst revenue estimates by 6.9% in the Q1 results, which led the ad-tech sector. The company’s revenue grew by 34% YoY to $324.4 million, and its North American business grew by 34% YoY to $316.5 million.

The company’s North American revenue guidance for the next quarter is $292.5 million to $297.5 million, representing a YoY growth of 36% at the mid-point. It also raised FY2023 North American revenue guidance to $1.235 billion to $1.265 billion, representing YoY growth of 27% at the mid-point, up from the previous guidance of $1.195 billion to $1.225 billion. It also reiterated its goal of being cash flow and adjusted EBITDA positive by 2025.

The company sees some improvement in its advertising business as the company’s CFO, John Janedis, answered to an analyst question on CTV advertisement demand trends. “And so when we looked at our Q1 results, to your point, we came in about flat on ad revenue. From a monthly perspective, let me just talk you through that and then I'll also go through 2Q in some of the categories. March was better than February, which is better than January. And I'd say if I sort of give you some of the numbers around that, January was down slightly, February, call it, flattish and then March was up a bit, maybe call it mid-singles. And then we're seeing further acceleration now into April and 2Q and so far April, I think finished up in the double-digits. So, we're encouraged by what we're seeing in terms of some of the trends.”

Revenue Growth Estimates for Q2

Source: YCharts

Unity leads with the highest growth estimate for the next quarter. Per what was already discussed, this is due to the ironSource acquisition. Unity is followed by Fubo and DoubleVerify. DoubleVerify’s revenue grew by 27% YoY to $122.6 million.

Revenue guidance for the next quarter is $131 million to $135 million, representing YoY growth of 21% at the mid-point. Analysts expect revenue to grow 22% YoY to $133.5 million.

Needham analyst Laura Martin raised the firm's price target on DoubleVerify (DV) to $45 from $35 and kept a Buy rating on the shares after attending an investor call with its CEO Mark Zagorski.

According to her note, Meta Platforms (META) accounts for half of the company's total social revenue, and the firm now believes that measurement revenue from Meta could double over the next 12-24 months after DoubleVerify adds brand safety suitability to its product suite, the analyst told investors in a research note. Retail media networks will drive total addressable market and revenue upside for DoubleVerify as more brands insist on closing the loop between ad spending and sales, the firm added.

Revenue Growth Estimate for Current Fiscal Year

Source: YCharts

For the current fiscal year, analysts expect Unity to have the highest revenue growth estimate among ad-tech stocks. It is followed by Fubo, which analysts expect to grow by 28% and DoubleVerify is expected to grow by 25%.

P/S Ratio (Forward)

Source: YCharts

Most ad-tech stocks are trading at a low valuation. The Trade Desk has the highest forward P/S ratio of 19.5. The Trade Desk has been trading at a premium valuation as its revenue growth has been stronger and its bottom line is better than its peers. The company’s 2022 revenue grew by 32% YoY to $1.58 billion. This revenue growth was exceptional while other ad companies struggled with growth last year, such as Meta, which reported a decline of (1%) in revenue.

The company’s CEO and Founder, Jeff Green, highlighted in the Q4 earnings call, “Specifically in the last 6 months of 2022, The Trade Desk started to separate from much of the digital advertising market in terms of relative outperformance. In the third quarter, we have reported 31% growth while our competitors were either in retreat or posting single-digit growth. That same trend continued into the fourth quarter as we grew 24% and most of our large competitors were posting between negative 9% and negative 2% growth. I don’t think we have ever had the level of industry outperformance in our 6 years or so as a public company as we did in 2022.”

Analysts expect revenue to grow 22% in FY2023 and continue to grow over 20% till 2030, with a revenue growth forecast of 30% for FY2028.

The company’s recent quarter revenue grew by 21% YoY to $383 million.While macro conditions remain uncertain and advertising budgets are carefully scrutinized, the management sees some improved visibility. Laura Schenkein, the new CFO of the company, said in the earnings call, “Turning now to our outlook for the second quarter. While macro conditions remain uncertain, visibility has improved slightly since the beginning of the year. We are cautiously optimistic and estimate Q2 revenue to be at least $452 million which would represent growth of 20% on a year-over-year basis.”

The company reported an operating loss of ($23.3) million compared to ($17.1) million for the same period last year. The increase in operating loss was due to increased operating expenses related to in-person events and travel this year that was stopped briefly post Covid. We have noted later in our article that ad-tech stocks have a weak bottom line. The company has a better bottom line than most adtech stocks, and in the recent quarter, it ranks 7 in the operating margin among the 17 stocks we track in the sector. The company reported an adjusted EBITDA margin of 28% compared to 38% in the same period last year.

Morgan Stanley analysts recently upgraded the stock to overweight from equal weight. “We see growth in ad-supported streaming and retail media as two of the strongest growth areas in online advertising and see the US CTV market growing at a ~18% '22-'25 CAGR while we forecast retail media (global ex-China) to grow at a ~17% CAGR. As the leading independent demand-side platform (DSP), TTD is well positioned to benefit from both trends,” the analysts said in a client note. “We believe TTD will be able [to] leverage its position as an independent player to sign more retail media partners…and ultimately be a leader in offsite retail media advertising,” they added.

Free Cash Flow Margin

Source: YCharts

Ad-tech is a very cash-efficient industry, evidenced by the robust free cash flow (FCF) margins, as seen in the above chart. The Trade Desk has the highest free cash flow margin of 46%, followed by Pinterest with 30%, and Netflix with 26%.

We had highlighted the Netflix’s cash flow turnaround in our editorial in July 2022 when we said, “The most important line item for Netflix is the company’s cash flow. Looking back, this has been troublesome for Netflix as the company lost $3.3 billion in cash in 2019 as it built up its original content pipeline. However, the company is on an entirely new trajectory with $1 billion in free cash flow expected this year and “substantial” free cash flow in 2023, per Netflix management.”

Operating Margin

Source: YCharts

Only five of the ad-tech stocks have positive GAAP operating margins in the recent quarter. Meta leads the sector, followed by Google and Netflix. We believe focusing on profitable companies or those with strong profitability paths is prudent during a time of current macro uncertainty.

This article was originally published on Forbes on May 10, 2023,07:45am EDTForbes Forbes on May 10, 2023,07:45am EDT

The mega-cap stocks that are known as FAAMG reported earnings recently. These names are driving the market higher, especially Microsoft and Apple. In fact, the percentage of Microsoft and Apple’s combined weighting in the S&P 500 has never been higher.

The S&P 500 weighting is according to market cap, which is price times float. The longer buying happens in these two names, accompanied with selling in other areas of the index, the percentage weighting becomes stretched to unhealthy extremes. This is not characteristic of a burgeoning bull market; instead, it is the type of behavior we usually see at market tops.

Also worth noting, since the February top, we are seeing a strong rotation into Big Tech while aggressive selling is taking place in other areas of the market. Take a look at the market cap weighted NASDAQ-100, which has over40% weighting into the FAAMG stocks, compared to the equal weighted NASDAQ-100.

Source: I/O FUND

While the NASDAQ-100 has made a series of higher highs, led mostly by the FAAMG names, the equal weighted index has made a series of lower highs. We are seeing similar price action in small caps as well as most economically sensitive sectors. This is typically not the sign of a healthy market.

FAAMG Stocks Trading at Precarious Valuations

As you’ll see below, there’s little room in FAAMG valuations compared to their 5-year historic averages. Apple and Microsoft both trade above their 5-year median on the top line and bottom line whereas the others are getting quite close given the low growth rates and macro uncertainty. The only exception is Amazon.

Microsoft is leading on valuation at 10 compared to the FAAMGs that are at 7 or below. Most are within range of their five-year average valuation except Amazon at 2.0 today compared to an average valuation of 3.6.

Source: YCHARTS

Amazon has a P/E ratio of 247.79, compared to 32.96 for Microsoft, 29.22 for Meta, 28.13 for Apple, and 23.32 for Alphabet. The FAAMGs are trading within range of their historical valuation except for Amazon with a five-year average P/E ratio of 93.48.

Source: YCHARTS

Sign up for I/O Fund's free newsletter with gains of up to 221% – Click hereClick here

FAAMG Earnings Overview:

There were some puts and takes in the most recent earnings reports. Despite price telling us we could be nearing a top, there are some fundamental signs that FAAMG stocks may be overstretched in the near term.

Below, you’ll find that consensus points toward a bottom for FAAMG stocks yet it will require consensus materializing in the coming quarters in order for the stock price action to hold. In other words, the market has front run the rebound in growth and now we must wait and see if this rebound unfolds.

Alphabet: Search is Resilient

Alphabet’s revenue grew by 2.6% YoY or 6% in constant currency, for a total of $69.8 billion, primarily helped by the resilience in Search and the momentum in Cloud business. Although this is marginal growth, below you can see that Alphabet is expected to accelerate in revenue growth over the next few quarters from 2.6% to an expected 9.4% in Q1 of next year.

Source: SEEKING ALPHA

Operating margins were soft at 25% of revenue compared to 30% last year. Net income declined (8.4%) YoY to $15.1 billion. This resulted in EPS of $1.17 compared to $1.23 for the same period last year.

Source: YCHARTS

The drop in profits was mainly due to $2.6 billion in charges related to the reduction in the company’s workforce and office space, and was offset by $988 million in depreciation from servers and network equipment.

Google Cloud revenue grew by 28% YoY to $7.45 billion and reported its first profitable quarter bringing in $191 million operating income.

Microsoft: Top Line and Bottom Line Beat

Microsoft’s revenue grew 7.1% YoY and 10% in constant currency to $52.9 billion. Management’s revenue guidance for next quarter is $54.85 billion to $55.85 billion, representing YoY growth of 6.7% at the mid-point. Similar to Google, a noticeable acceleration is expected in the second half of the year.

Source: SEEKING ALPHA

Azure grew by 27% and 31% YoY in constant currency and came in at the higher end of management guidance of 30% to 31%.This is down from 38% growth in constant currency last quarter. Next quarter will also mark a deceleration with management guiding to 26.5% in constant currency. This includes 1% from AI services.

Source: I/O FUND

Operating income grew by 9.8% YoY to $22.35 billion. The net profit margin was 34.6% compared to 33.9% in the same period last year which resulted in EPS of $2.45 compared to $2.22 in the same period last year.

Source: YCHARTS

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.Learn more here.

Meta: Back to Positive Growth

The company’s revenue grew by 2.6% YoY and 6% on constant currency to $28.6 billion. This is a positive as Meta’s revenue has declined YoY in the last three quarters.

Management’s revenue guidance for the next quarter is between $29.5 billion to $32 billion, representing a YoY growth of 6.7% at the mid-point. Analysts expect revenue to grow 7% YoY to $30.84 billion.

Source: SEEKING ALPHA

The operating income declined by (15%) YoY to $7.2 billion as total expenses rose 10% YoY. The operating margin was 25% compared to 31% in the same period last year. The net income declined by (24%) YoY to $5.7 billion, resulting in EPS of $2.20 compared to $2.72 in the same period last year.

Source: YCHARTS

The company recorded $1.14 billion in restructuring charges related to layoffs, facilities consolidation, and data center. Excluding these charges, the operating margin would be 4% higher and EPS would be $0.44 higher.

Amazon: AWS is Slowing

The company’s revenue grew by 9.4% and 11% YoY in constant currency to $127.4 billion. Analyst consensus is for growth of 8.2% next quarter.

Source: SEEKING ALPHA

The operating margin was 3.8% compared to 3.2% in the same period last year. Net Income was $3.2 billion or $0.31 per share compared to a net loss of ($3.8) billion or ($0.38) per share in the same period last year.

The net income included a pre-tax valuation loss of ($0.5) billion from the investment in Rivian Automobile compared to a pre-tax valuation loss of ($7.6) billion in the same period last year.

Source: YCHARTS

AWS revenue grew by 16% YoY to $21.4 billion. This is lower than the 20% growth in the December quarter and a remarkable slowdown from the 37% in the same period last year.

Management discussed in the earnings call that April AWS revenue growth further decelerated to 11%. This is due to the ongoing tough macro environment, causing customers to optimize their cloud spending in the recent quarter.

The company’s CEO, Andy Jassy, also highlighted cautiousness in the enterprise customers. “In AWS, what we’re seeing is enterprises continue to be cautious in their spending in this uncertain time. Customers are looking for ways to save money however they can right now. They tell us that most of it is cost optimizing versus cost cutting, which is an interesting distinction because they say they’re cost optimizing to reallocate those resources on new customer experiences.”cost optimizing versus cost cutting, which is an interesting distinction because they say they’re cost optimizing to reallocate those resources on new customer experiences.”

Notably, despite the market rewarding Microsoft’s report, cost optimization is not isolated to one hyperscaler and investors can expect to see more evidence of optimizations in future reports.

Apple: More Buybacks to Appease the Street

Apple’s revenue declined by (2.5%) YoY to $94.84 billion. Management commented that they expect YoY performance to be similar to the March quarter. Analysts expect revenue to decline (1.7%) YoY to $81.53 billion in the next quarter following these comments.

Source: SEEKING ALPHA

iPhone sales grew by 1.5% YoY to $51.3 billion. Mac revenue declined by (31%) YoY to $7.2 billion. iPad revenue declined by (13%) YoY to $6.7 billion. Wearables, home and accessories revenue was flat, and the services segment revenue grew by 5.5% YoY to $20.9 billion.

The operating margin was 29.9% compared to 30.8% in the same period last year. The operating expenses of $13.66 billion were lower than management guidance of $13.7 billion to $13.9 billion, which the market saw as a positive.

Net income declined by (3.4%) YoY to $24.2 billion with a net profit margin of 25.5% compared to 25.7% in the same period last year. EPS came in at $1.52 and remained unchanged from the same period last year.

Source: YCHARTS

Apple returned $23 billion to the shareholders through dividends and equivalents of $3.7 billion and $19.1 billion in share repurchases. The board also authorized an additional $90 billion share repurchase and increased the quarterly dividend by 4% to $0.24 per share.

Analyst Comments:

Deutsche Bank analyst Benjamin Black raised the firm's price target on Alphabet to $125 from $120 and kept a Buy rating on the shares. He noted, “The company reported solid Q1 results with the biggest takeaway being the stabilizing growth trends at Search and YouTube, which beat Street expectations.”stabilizing growth trends at Search and YouTube, which beat Street expectations.”

Wedbush Securities analyst Dan Ives said in a research note. "It's clear that in Redmond's enterprise backyard the company is gaining more market share on the cloud front with many enterprises making this transformational shift on the shoulders of Microsoft,"gaining more market share on the cloud front with many enterprises making this transformational shift on the shoulders of Microsoft," He further said, "Cloud growth and the overall outlook for the June quarter was solid and much better than feared given recent noise in the market and will be music to the ears of investors this morning digesting results."Cloud growth and the overall outlook for the June quarter was solid and much better than feared given recent noise in the market and will be music to the ears of investors this morning digesting results."

BMO analyst Keith Bachman upgraded Microsoft (MSFT) shares to outperform. He stated that he now has "higher conviction" that any headwinds to Azure are likely to moderate by the end of the year, while opportunities in artificial intelligence can help the longer-term. "While the stock is not inexpensive, we think the durable growth opportunities warrant a premium valuation."

RBC Capital analyst Brad Erickson raised the firm's price target on Meta Platforms to $285 from $225 and kept an Outperform rating on the shares. Brad said, “The company's Q1 results were better-than-feared and the simple three-fold bull case – dominating engagement vs. competition, restoring lost signal post-IDFA, and cutting costs – is increasingly coming into view.” RBC believes that further upside is still achievable for Meta on engagement share gains and the ongoing conversion improvement eventually leading to incremental spend.

Citi analyst Ronald Josey raised the firm's price target on Meta Platforms to $315 from $260 and kept a Buy rating on the shares. “With engagement rising, newer advertising products attracting incremental spend, and a more streamlined organization, Meta's momentum in Q1 can continue.”“With engagement rising, newer advertising products attracting incremental spend, and a more streamlined organization, Meta's momentum in Q1 can continue.” the analyst tells investors in a research note.

Conclusion:

We have Buy levels we are targeting for FAAMG stocks, which we share with our premium research members each week as the stocks progress. We believe our target buy levels will set us up for gains in FAAMG stocks when the next bull cycle begins. We provide in depth macro and individual stock analysis so that readers can better understand why we buy/sell. In this market, we frequently take gains.

Right now, we do not believe FAAMG stocks are in a buy zone. Instead, some are trading higher than their 5-year median on valuations despite a weaker macro backdrop and fundamental weakness. The market is front-running the anticipated revenue rebound. Most of this rebound is based off low comps, and there could be soft growth in the future for some of these names.

You can learn more here including information on our next webinar, this Thursday at 4:30 pm Eastern, where we review our positions live.

Equity Analyst Royston Roche contributed to this article.

Please note, that Perion is a Hold right now and we will inform our Premium Newsletter Members if we initiate a position. The I/O Fund is unique in that we do not issue blanket buy recommendations, rather we offer an actively managed portfolio. We do not own the stock right now but we hope to enter the stock when the technicals line up. Our process is tied to a real portfolio with audited results. Our service aims to show individual investors the reality of stock investing, which is to do extensive due diligence, and then to be patient on price. In addition, tech investors must be especially keen on macro events as the tech sector is particularly sensitive to high interest rates. This is very different from other services that push out content with no adherence to actual performance and/or entries, exits.

Summary:

Last March, we covered Google’s anti-trust lawsuit here for premium newsletter members. This is an important analysis to revisit for Perion Network.Google’s anti-trust lawsuit here for premium newsletter members. This is an important analysis to revisit for Perion Network.

Perion Network is a digital advertising company headquartered in Holon, Israel. The company offers digital solutions in three primary channels of digital advertising: ad search, social media, and display/video/CTV advertising.

Perion helps brands and publishers to identify and reach customers through the company’s proprietary Intelligent HUB (iHub), which processes billions of signals, and powers the cookieless solution SORT. By mixing contextual data with user insights, Perion is able to forego cookies by using this data with AI-based clustering techniques. SORT stands for Smart Optimization of Responsive Traits, which translates to categorizing customers into 1 of 30 Smart Groups through shared traits.

The primary sources of data are contextual – so what a customer is reading at the moment, why they’re reading it, how long they’re reading it and/or what search words brought them to the content. This is combined with signals such as time of day, weather, browser, device, etc.

Ultimately, what Perion’s technology does is calculates the similarities between groups, and then to target the group that performs the highest in terms of converting. The model is deemed effective when one group has a significantly higher click-through-rate (CTR).

Second, SORT then optimizes the bids so that it’s a cost-effective solution. SORT analyzes the bid of each publisher and selects the price that is likely to win. If the price is too high, SORT finds another publisher with a similar audience as the SmartGroup. The entire process happens in real-time.

Doron Gerstel, CEO of the company, said in the Q2 2022 earnings call, “iHub sits in the center of the supply and the demand side of the market. This is an innovative model that no one else in the industry has, aggregate data signals from all channels and from both sides of the open web to create the model that eliminates waste and rewards clients. The data goes into Perion’s privacy first cookieless solution known as SORT.”

This is important because cookies are expected to be phased out from Chrome in 2024. Cookies have already been phased out by Mozilla Firefox and Apple Safari.

In addition to this, Perion has partnered with Microsoft Bing. CodeFuel is the Perion product that powers intent-based monetization. When you go to search for something on a search engine, Perion’s CodeFuel can power the search results in an optimal way for conversion. This has led to a strategic partnership between Microsoft and Perion that was renewed in 2020 for four years.

Per a previous earnings call, “If the new Bing search with ChatGPT sparks even modest share gains, Microsoft can do very well in the business. As their CFO, Amy Hood said yesterday, every percentage point of share it gains in search equals roughly $2 billion in additional advertising revenue, and as a strategic partner of Microsoft Bing, I’m sure we will be benefiting from this increase.”I’m sure we will be benefiting from this increase.”

Notably, there is a risk that Microsoft does not renew its partnership next year. However, this risk is muted a bit since Perion was named “Global Supply Partner of the Year” by Microsoft in 2022.

What’s interesting about Perion is that the company is fundamentally one of the strongest ad-tech companies on the public markets due to a strong bottom line and a top line that was more resilient than its peers. Any windfall here could very interesting for a company that already proven operational efficiency with a 16% to 20% operating margin while maintaining 30%+ growth in the tough year of 2022. Notably, the top line is decelerating to the 10% to 15% range but a catalyst here that could lead to a reversal could be quite interesting

Perion Networks: Google Anti-Trust Beneficiary Plus AI Tailwinds

We published a piece in March on the potential outcomes from Google’s anti-trust trial slated to begin in the fall of this year. If Google is found to have engaged in anti-competitive behavior, we identified Perion Networks (PERI, $1.5b mkt cap) as a potential beneficiary.

Currently, Perion holds a unique position in the advertising technology sector that has enabled it to outperform its peers. Perion recently reported Q123 earnings. At a time when its peers are dealing with advertising budgets that are in flux, Perion revised upward its 2023 sales target. The earnings report provided a good opportunity to get an update on the business and the main business drivers.

Perion is positioned to benefit from several key investment themes.

Maximizing search monetization and integration with AI

Helping companies compete against Amazon and Walmart

Increased browser privacy awareness

Outsourcing of video advertising functions

Maximize advertising budgets

What does Perion do?

Perion is a digital advertising company that provides technology to brands, agencies and publishers to identify, reach and monetize their most valuable customers – across numerous digital channels, including retail media. Clients include world-class brands such as Mercedes-Benz, IBM, Disney, Walmart, Albertson’s and Verizon.

Perion has two main businesses, Display and Search advertising. They make up 55% and 45% of total revenue, respectively. Within these divisions, there are 3 main activities

Search ad monetization, a direct-response platform that works with a range of different publishers

Cross-channel high impact advertising through the open web, including video and CTV

Social advertising through Perion’s performance monitoring platform and content monetization system

There are 5 key business drivers

1. Search Advertising and AI

Capturing consumers at their moment of highest intent has been well-established as the highest ROI (Return on Investment) advertising channel. Advertisers are increasingly allocating funds to search advertising. According to eMarketer reports, U.S. search advertising market reached $101 billion in 2022, and is estimated to reach over $108 billion in 2023, which represents 39% of U.S. digital ad spending.

Search is a fundamental digital behavior that will continue to grow. Perion continuously innovates to provide more value to its publishers. Perion deploys advanced AI, neural networks, and machine learning to optimize yield for its publishers and transform search into revenue. As this shift continues, Perion is well positioned thanks to its longstanding relationship with Microsoft Bing. In 2022, Perion was named Microsoft Advertising’s Global Supply Partner of the Year.

Search monetization is one of Perion’s core and most profitable areas. The business is driven by 1) increasing the number of publishers 2) the aggregate number of monetized searches transferred, mainly through its partnership with Microsoft Bing and 3) integration of ChatGPT with Microsoft Bing

In Q123, these 3 factors contributed to a 29% increase in the number of publishers. As a result, average daily traffic increased by nearly 50% year-over-year and are now close to 30 million monetized searches per day on an average basis. The ability of Perion to monetize search traffic through their Microsoft Bing Partnership and its effectiveness is best reflected in the growth of Perion’s publisher network. This is particularly important given the growing shift to Direct Response, as search represents the highest intent customers.

This is how Perion described the ChatGPT impact and opportunity. Notably, Microsoft Bing has 3% market share and for every additional 1%, Microsoft will make an additional $2 billion. This may not be enough to move Microsoft stock, but can have an impact on Perion.

“We believe that the massive media attention to ChatGPT has driven a material portion of this (Q1 growth) and that will continue to see growth that exceeds our normative project. Microsoft Bing has a real competitive advantage now and that cascade[s] immediately to our business.”

“Now to other part of your question, I think that this is – it’s beyond what we able to imagine, what the ChatGPT is going to make. It’s quite a transformation. Quite a transformation and I would say that the search interaction as we’ve seen an experience in let’s say the last 20 years is not going to be the same. And we will have a chance to look at it two years from now, it would be completely different interaction, user experience, engagement between consumer and search engine. No doubt about it.”

2. Perion’s retail media solutions

Perion provides digital advertising for major retailers who have launched their own digital presence to compete with Amazon and Walmart. Perion works with companies such as Albertson’s, CVS and Target. Perion has built an AI-driven platform that enables these retailers to maximize the value of their inventory with ad units that identify consumer signals and responds with timely and personalized promotion and content. Perion can personalize at scale and can do it in an omni-channel fashion across all screens.

This allows retailers to shift away from transaction campaigns (i.e. circulars) to “always on” which generates higher returns. For Albertson’s, Perion delivered 14 times return on ad spend.

As the chart below shows. Perion develops targeted advertising at various touchpoints for different companies to target the consumer throughout the day. As the diverse client list below shows, this ranges from RiteAid to P&G to GSK.

3. SORT and Privacy

Perion’s proprietary SORT (Smart Optimization of Responsive Traits) technology will benefit from ever increasing privacy demands. SORT is a cookie less and totally anonymous solution that protects consumer privacy. Further, SORT does not collect or store any user data, the way other cookie-less solutions do. This is attracting brands who wants to be associated with the privacy-first capability while generating strong ROI.

Cookies are an essential part of the targeting infrastructure of the digital advertising market, they are under increasing pressure for the manner in which they are perceived to violate user privacy. In fact, the U.S. Congress is looking into cookies and considering further restrictions. SORT provides a competitive solution that should enable Perion to capture additional revenue as brands and advertisers move away from traditional methods such as cookies and other platforms. Google has postponed its elimination of cookies until the end of 2024 presumably because they need to do further testing to develop a satisfactory replacement solution.

In addition, consumers are made aware that a brand campaign is running through SORT, and hence the ads are safe to click, thanks to a proprietary “Privacy Shield” graphic logo that is incorporated into every ad unit running through SORT. SORT is a solution that provides consumers with visible confidence they won’t be followed around the web as their behavior is being tracked.

Currently, Perion’s clients range from Mercedes Benz to the United Nation. SORT will grow as it attracts more brands who want to be known for espousing privacy first principles.

4. Video Platform

Via their Vidazoo division, Perion’s end-to-end platform is meeting a large and growing need for publishers who are looking for fast results and lack the internal resources to build the complex time maintenance internal system. Perion is able to offer different aspects of the Vidazoo suite depending on their client’s needs.

Through Vidazoo’s proprietary video platform, Perion offers a wide range of products, through which publishers can deliver an enhanced user experience, increase video content consumption, and identify new monetization opportunities.

A simple example is how Dr. Pepper, using Perion’s Vidazoo, was able to run an ad while a sport event was playing. There was no interruption to the viewer.

5. iHUB

Perion’s proprietary Intelligent Hub (iHUB) connects the supply and demand sides of the ad marketplace. It processes billions of signals from across its network and properties. This provides five levels of value: operational savings in the form of – shared resources; reduced traffic acquisition costs and media buying optimization; increased customer value; market agility.

For Perion, iHUB helps increase its media margin (Revenue less traffic acquisition costs or TAC) by lowering TAC costs. While for Advertisers, iHUB helps them reach their ROAS (Return on Ad Spend) goals.

iHUB allows Perion’s business units to quickly balance demand and supply, providing optimum utilization of their owned & operated supply, as well as what is available on the open web. This optimization is enhanced by their ability to offer publishers and advertisers multiple ad products to support their marketing efforts which enables Perion to increase its market share with current and new clients. This helps reduce Perion’s TAC.

At the end of the day, companies seek to maximize their advertising budgets. Perion is able to help companies satisfy their ROAS though iHUB. This technology is Perion’s key competitive advantage. This is how Perion described it.

“We’re able to capture and analyze data signal from all channels and from both sides of the open web into our central hub. We’re using advanced AI to develop a bidding system that maximize our unit revenue, while reducing our video costs. By doing this, we uniquely combine efficient bind with the ability to meet our customer ROAS, Return on Ad Spend expectations. At the same time, when advertiser under extreme growth pressure, this is a true competitive advantage for us.”

“Without having all the pieces of the business connected, we would be managing a very costly, inefficient, fragmented business. On a given day, we capture into iHUB data lake billions of data requests from various media channels. One example of effectively leveraging this amount of data is creating an AI driven bidding strategy that optimizes the match between supply and demand to maximize our profit.

At the same time, it assures the highest performance to our customers. Our iHUB open architecture is a foundation that enable us to make acquisitions, which are instantly optimized because they plug in into the center of our ecosystem. As FX grows more complex and multi-dimensional, the value of our iHUB will only become way more meaningful.”

Q123 Earnings

Perion recently exceeded Q1 earnings expectations and revised their FY23 sales target of between $725-745 million which is 15% year-over-year growth at the midpoint.

One risk for Perion is that the revenue growth rate decelerated from the 30% range in prior quarters to 15.8% in the most recent quarter. Right now, analysts are showing further deceleration. We will want to see Perion resist this deceleration through one of the catalysts noted above – whether it’s product-market fit with niche advertisers, Microsoft-Bing partnership with Bing increasing in market share due to Chat-GPT and/or Google’s anti-trust lawsuit having a favorable outcome.

With increasing EBITDA and Profitability (EBITDA Margins). The GAAP operating margin was up year-over-year at 16.8% this quarter compared to 13.17% in the year ago quarter. However, this was down from the September quarter and December quarter, both in the 19% to 20% range. This is something to watch, to make sure it continues to trend up – if not on a sequential basis than at least on a year-over-year basis.

Q1 media margin increased year over year (Sales less TAC)

The balance sheet is very strong for a small cap stock with $384 in cash and no debt.

Conclusion:

Through different market environments from 2020 to 2022, Perion has continued to execute from a business and financial perspective. It demonstrates that through changing consumer and advertiser needs, Perion has been able to adapt and meet those needs.

During a time when advertising budgets are under pressure, Perion’s key competitive advantage is its technology provides a meaningful ROI on ad dollars spent by its customers.

Perion’s partnership with Microsoft Bing, while still in its early stages provides an exciting growth opportunity in its Search business. Meanwhile, Retail Media and SORT are businesses that will continue to grow. Later in the year, depending on the Google court case, Perion may also benefit.

Deep dives, trade alerts, a forum and weekly webinars on the I/O Fund portfolio are offered on our premium service, you can find out more information here.Deep dives, trade alerts, a forum and weekly webinars on the I/O Fund portfolio are offered on our premium service, you can find out more information here.more information here.

It may feel like the words “Google” and “lawsuit” are commonplace, but the trial in September carries enormous weight and is unlike the lawsuits of the past. Not only do we want to keep an eye on ad-tech names that could benefit should Google’s monopoly be broken up and the juggernaut come out weaker, but we also want to be prepared if the tech giant is able to hold off regulators.

Considering that Google is sitting on the world’s very best consumer data, which is not an exaggeration in the least bit, its ability to lead on artificial intelligence and large language models should not be underestimated. For our purposes, the company is far from sitting on its laurels and there’s a predictable path where the company competes in a duopoly with Microsoft.

Therein lies the issue. Google undisputedly has the world’s best consumer data, but did this grow to become part and parcel with operating a monopoly? The Department of Justice has asserted anti-trust violations against Google with the trial beginning in September 2023. The trial is expected to last ten to 12 weeks, although a lawyer for the DOJ told CNBC it could be as brief as five weeks.

Why it matters:

With Google and other ad-tech companies trading this low, one of two outcomes will happen. The antitrust outcome will be mild, and Google will be empowered to continue to dominate. Or, the outcome will require the ad properties to be broken up, leading to a weaker stance for Google. This could benefit smaller ad-tech players.

The Goal — Looking back:

A few years back, I analyzed the potential outcome of a government decision when the Pentagon was evaluating cloud providers. Clearly, this decision is far outside of anyone’s control and requires some speculation. At the time, I speculated Azure would be a winner. For a year or so, Microsoft did secure the Pentagon contract over the more-favored Amazon. This decision was ultimately reversed, and the contract was split between four tech companies.

The exact outcome of the Pentagon contract was not particularly important because the analysis led to my conclusion that Microsoft’s hybrid computing was a material advantage and this would be the path Nadella would most likely use to take market share from AWS’s heavily-slanted public cloud strategy.

I’m hoping for something similar, which is to acknowledge something very important is going on with ad-tech, which is Google’s antitrust case. This is not a headline to simply dismiss. It’s the first time the DOJ has brought a case of this kind against a technology company since Microsoft. If there are even minor cracks in Google’s monopoly, there could stand to be a stock or two that starts a new trajectory.

On similar note, Cambridge Analytica is what sparked my coverage on Facebook. Similar to Google’s antitrust case, it became apparent to me that Facebook was peaking in terms of its ability to monetize through third party data. I covered this extensively, for example here and here.

Brief Overview of Antitrust Case:

According to Lanier Law Firm, which is the litigation team for the State of Texas in the state coalition case, a primary argument against Google is that the company went above and beyond to become the default search engine on iOS devices by paying Apple $12 billion per year.

The lawsuit includes other deals that Google struck with Apple’s Safari browser, the Mozilla browser and Android device manufacturers where Google either paid up or imposed restrictions on Android device makers to strongarm having their suite of apps pre-installed on the home screen.

The company has already lost an antitrust case in Europe in 2018 with a $4.4 billion Euro fine for forcing Android manufacturers to pre-install Google’s bundle of apps on the device, including Chrome, Maps and the Play Store.

Google’s market share of Search is at 91% and the argument is being made this was accomplished through anti-competitive practices, especially since Google owns Android and had leverage over the many device makers that used this operating system.

In addition to being pre-installed and the default browser/search engine, Google also attempts to keep people on its search engine by using a website’s data on its page. For example, if you look up “Best Dog Breed” Google scrapes Wikipedia and puts the results onto the search page instead of sending you to Wikipedia. This is seen as anti-competitive as it takes a website’s data to profit from it, rather than directing the traffic to the rightful copyright owner, which is the function of a search engine.

Part of Microsoft’s antitrust case was based on Microsoft using its dominance on Windows to force a Microsoft Explorer to be the default browser. At the time, the decision was that default settings are anticompetitive.

The secondary argument filed by a 10-state group led by Texas, is that Google leverages its properties to be the buyer and the seller via its ad exchange. Per Lanier Law Firm, the Texas case states Google and Facebook “unreasonably restrained trade and harmed competition through an unlawful agreement to allocate auction wins and to fix prices in violation of Section 1 of the Sherman Act, 15 U.S.C. § 1”

This is where it gets very messy, and so I’ve dedicated a specific section below to break down these details. The purpose of understanding the minutiae is not to only determine if we should buy Google and when, but also what companies could stand to benefit if Google’s products are shutdown or broken up.

My long-ago analysis on Facebook pointed toward a conflict of interest in the company owning a third-party ad network called Audience Network while also being publisher. At the very least, the conflict of interest created a risk since Facebook was essentially siphoning oil from real estate the company didn’t own (iOS users). This was a serious, material risk for investors that played out over time (note: it certainly wasn’t immediate, it took four years from the first time I covered the topic).

If you’re a Meta investor, you’ll want to watch the CPMs on the company and make sure the erosion below is not permanent. Despite Apple only impacting third-party data, it’s unclear how much of that third-party data was informing its first party data. The unusually high CPMs that Meta charged points towards enhanced targeting – that in my opinion – was likely due to mixing both first-party data with third-party data. This means there will be an eventual erosion, over time, of the CPMs Facebook can charge even on its own applications.

Pictured above: Although subtle, there is an erosion to Facebook’s otherwise high CPMs. You can see that Nov 2022 made a lower high over Black Friday compared to the two previous years. Many factors could be at play, such as lower ad budgets, but it’s something investors should keep a close eye on.

Google currently does the same thing that Facebook used to do, which is to run an ad exchange that is undeniably a conflict of interest. The difference is that rather than renting real estate, like Facebook did with iOS, Google is a real estate tycoon. There isn’t a tech company that can kick Google off their turf because Google owns all of the turf – primarily Chrome, Android, Google Search, and YouTube.cBy conflict of interest, I’m referring to AdX, DoubleClick and DV360, collectively known as the Google Network.

Below, you can see Google Network is a $32 billion annual revenue stream. Not exactly peanuts.

To further the lawsuit, a 30-state coalition has issued a third claim that Google uses its monopoly to rip off smaller companies, such as Yelp, DoorDash, and Kayak. You can see evidence of this when Google Search returns flight searches powered by Google at the top, with a large embedded format, rather than producing a fair search result that includes competitors. Yelp has been in a battle with Google over this for over a decade. After Google Reviews were launched, Google pushed Yelp down the page in terms of search results.

The two search engine allegations are fairly straight forward. Most of us who use Google Search can reasonably understand those arguments.

The Messy, Blackbox that is AdExchange (AdX):

DoubleClick was acquired in 2007 for $3.1 billion. As author Tony Yiu points out on Toward Data Science, this was twice the amount paid for YouTube a year earlier. Google Network is a by-product of many acquisitions including AdMob for $750 million and AdMeld for $400 million, among others, yet DoubleClick truly set the supply side dominance in motion as the company owned 60% of the desktop publisher market at the time of acquisition.

DoubleClick allows Google to set a cookie on a website so that online publishers can better target visitors with ads. The DoubleClick cookie provides the time and date a user saw an advertisement, as well as a unique ID that identifies a user by their browser. Publishers are then able to auction inventory to advertisers.

DoubleClick was a major move by Google to expand beyond search advertising. This was the first time Google entered the market on display ads. As stated, DoubleClick owned 60% of the publisher market when it was acquired, which means Google would eventually profit from monetizing millions of websites.