We recently initiated a position in CrowdStrike and want to take the opportunity to update you on the company. Previously, I covered CrowdStrike in October 2020 here. In the report, I explained how cybersecurity would continue to be a key initiative for organizations in the remainder of 2020 and beyond. I also covered CrowdStrike’s product offerings and explained how the company was uniquely positioned as the top vendor in a critical subsector of cybersecurity. We discuss the previous coverage below and examine why the company has become even stronger, as well as numerous industry catalysts.

We continue to see strong C-level survey results for cybersecurity in 2021, in particular, with CrowdStrike and Zscaler the undisputed leaders. We discuss why we have chosen CRWD, yet it seems ZS is a strong second choice. We also cover Cloudflare and why we have passed for our own portfolio.

Security Software: Top Priority for 2021

Security software has consistently ranked as a top spending priority among C-level executives, but our research shows it has become the #1 priority in 2021. The Covid-19 pandemic and shift to a more remote workforce uncovered a number of major gaps in the cybersecurity of organizations.

The high-profile Sunburst hack further highlights the need for businesses to transform their legacy security architectures, as legacy tech is no match for today’s adversaries. As a result of the Sunburst hack, the current administration has talked about how cybersecurity spending is a top priority, calling on Congress to “launch the most ambitious effort ever to modernize and secure federal IT and networks.”

Credit Suisse’s recent CIO survey suggests that security spending is the top spending priority in 2021, even more so than in July.

We view CrowdStrike and Zscaler as the best positioned cybersecurity companies to benefit from the growing security spending cycle. We are still in the early innings of the shift in security architecture towards Zero Trust and SASE, of which we believe CrowdStrike and Zscaler will benefit the most.

Here’s a snapshot of government spending and the triple-digit increase in FY2020 growth in federal spending for Zscaler and CrowdStrike. The current administration’s commitment to cybersecurity should also benefit CrowdStrike and Zscaler as they continue to gain more share of federal spending.

1. CrowdStrike (CRWD)

In my past coverage of CrowdStrike here, I explained why the company would thrive as the fastest growing endpoint security vendor. Endpoints are frequently the first point of entry for attackers, so endpoint security is an integral part of a multilayered security strategy. CrowdStrike has thrived in this area, leading to the addition of a record 1,480 new subscription customers in Q4.

While CrowdStrike has demonstrated tremendous expertise in endpoint security, the full CrowdStrike Falcon Platform now encompasses much more. The full CrowdStrike platform, designed to define Cloud Security, includes managed services, security & IT operations, threat intelligence, identity protection, and log management. The power of CrowdStrike’s platform is demonstrated in the financial data, as 63% of CrowdStrike’s subscription customers have 4 or more Cloud Module Subscriptions. This number has grown from 47% two years ago and 55% last year.

The growth of this metric is important to CrowdStrike’s growth, as they have expanded their TAM through acquisitions and the launch of new modules that cover untapped areas of cybersecurity. We are now seeing the majority of CrowdStrike’s subscription customers, almost 2/3, adapt 4 or more modules meaning most customers are subscribing to the idea of having CrowdStrike handle most of, if not all of, their cybersecurity needs. CrowdStrike management has talked in the past about how most customers typically sign up for 1 or 2 modules but adapt more modules over time. This shows the success of the CrowdStrike customer life cycle. From the time the company onboards a new customer to the adaption of more modules, they are able to add new sources of revenue from already existing customers.

In Q4, CRWD grew revenue 77% YoY and added a record 1,480 new subscription customers (+82% YoY), with a number of marquee customer additions including Pfizer. CRWD also enjoyed a record quarter in profitability metrics with its best ever quarter of non-GAAP EPS (+$0.13), Free cash flow (+$97M), FCF margin (+37%), EBITDA (+$45M), and EBITDA margin (+17%).

CrowdStrike guided for 50% YoY revenue growth in FY 2021 and EPS of $0.29. The projected growth rate leads the security SaaS industry and our comparisons of ZS and NET, despite the stock trading at a slightly lower valuation than those stocks.

As previously discussed, with its recent acquisitions of Preempt and Humio, CrowdStrike has enhanced its capabilities beyond endpoint security to also encompass cloud workload security and identity protection. With Preempt Security, CrowdStrike is leading the charge with a Zero Trust solution focused on endpoints and workloads. In its Q4 earnings call, CrowdStrike CEO George Kurtz talked about how customers have become increasingly interested in its Zero Trust offering derived from Preempt following the Sunburst hack.

The acquisition of Humio will combine Humio's data ingestion and analysis engine with CrowdStrike’s technology. CEO George Kurtz discussed the Humio acquisition the company’s Q4 earnings call:

“With Humio, we are now redefining next-gen XDR through a platform that spans endpoints, identities, applications, the network edge and the cloud… Humio provides us the ability to expand our data leg and to solve more security and non-security use cases in real time… providing CrowdStrike with a greater time advantage over the competition and the adversary.”

It has become evident that CrowdStrike has continued to successfully enhance the capabilities it can offer and has taken a big step toward its goal of providing the “fastest, most cost efficient, and extensible cloud data platform that will deliver best-in-class visibility for security as well as observability for IT operations.”

2. Zscaler (ZS)

Zscaler ranks #2 behind CrowdStrike on our list of cybersecurity stocks to own. Like CrowdStrike, we believe Zscaler is well positioned to capture the industry wide shift to Zero Trust and SASE. We covered Zscaler’s Fiscal Q1 Results here. Fiscal Q2 was another solid quarter for Zscaler as they continue to show their strength as a major cybersecurity player. In Fiscal Q2, Zscaler grew revenue 55% YoY and gross billings an impressive 71%. Although Zscaler is an industry leader with strong fundamentals, our analysis shows that the company is not as strong fundamentally as CrowdStrike despite having a slightly higher valuation.

Over the next 12 months, Zscaler is projected to grow revenue 37% versus CrowdStrike’s 51%. ZS has slightly higher gross margins over the trailing 12 months at 78% versus CRWD’s 75% but lags CRWD in Operating Margin and FCF margin. We compare ZS to CRWD and NET fundamentally in the table below.

3. Cloudflare (NET)

We covered Cloudflare’s Q4 earnings here. Although Cloudflare is not purely a security company, approximately half of their products are security related. A lot of Cloudflare’s focus on the future is related, according to CEO Matthew Prince. In its Q4 earnings call, Cloudflare management talked about their expectations for a big shift in 2021 from a traditional hardware-based security approach to a much more modern Zero Trust approach. Cloudflare is well positioned to be one of the leading companies in enabling organizations to make this shift. However, we still view CRWD and ZS as better ways to play the shift in cybersecurity spending.

We feel NET is not as strong fundamentally as CRWD or ZS. The stock is also not as attractive from a valuation standpoint. For these reasons, NET ranks third behind CRWD (#1) and ZS (#2) on our list of security SaaS stocks to own moving forward.

Source: YCharts; data as of 3/25/21

Conclusion:

Selloffs are tough, but the silver lining is getting quality companies at much more reasonable valuations. CrowdStrike is a company that we think will do well when the market remembers that tech is not going anywhere and growth in this sector is not Covid dependent. CrowdStrike is my favorite company that had a stretched valuation throughout this past year and we see the selloff as a buying opportunity.

We hope you’re doing well. The new site is now fully launched at io-fund.com. We are also working on a new Forum Guide, FAQs and customer service flow so we can respond to account access issues faster.

We will continue to update you as we find opportunities in this selloff. Many of the stocks we own, including recent additions like CRWD and SNOW, are gifts at these valuations. We are also looking to add renewables exposure to the LTBH portfolio during this sell-off.

This week, you will get an update from David Marlin on security software stocks and why we entered CRWD. I’m working on a Snowflake update that should be out Monday of next week. There’s a chance the update on SNOW gets bumped for an analysis on renewables so we can figure out our allocation here. In the meantime, please reference this past analysis on Snowflake in Forbes here.

LTBH Update

I posted on the forum that we are adding Ethereum and Snowflake as LTBH positions. When the correction is over, we feel these two will more than make up for our losses in BAND and AMWL, which we have now closed. After the weak relative strength in both these positions on the bounce, we felt it was better to log a small loss and put those funds into stocks that we believe will continue to have stronger relative strength coming out of this correction.

Fundamentally, we closed AMWL because the forward is too low. During a few interviews about Unity, I discussed the downside to being early to a trend. For early trends we prefer to keep low allocations.

We were able to log a nice gain by cutting our position in TDOC in half close to the high. We think telehealth will be an important trend in the future. However, we could be very early to this trend. The health industry in particular is very slow moving and this could also be contributing to the reason telehealth is facing a tough year.

We closed Bandwidth because BAND should have had a breakout year with the digital transformation and work-from-home trend. Instead, we hold a large position in Zoom as we are bullish on Zoom Phone and the platform that Zoom is building that extends beyond a web conferencing app. I also don’t think Zoom is dependent on the work-from-home trend as I believe those who have Zoom accounts will continue with those accounts, except perhaps the education sector. Many of the education accounts were provided for free or at a reduced cost and this weighed on margins recently.

I am writing a free article update on Zoom Video as it’s part of my free coverage since last year. I think the market and financial news is confused as to where Zoom can go next and I am happy to go on record by revisiting my hardware-as-a-service thesis. It’ll also allow me to follow up on my free Bandwidth analysis and to let people know we closed the position.

Quick Note on the New Site

We will continue to have the old site available for six weeks as we expect to launch our new forum in May. At this time, we will archive Beth.Technology so the team can focus on the forum launch. The next six weeks will ensure we have sufficient time to handle any customer service issues due to the site transfer.

There are a few common mistakes we are seeing for access to the new site:

People have two or more emails and are running into issues because the system requires the email address you signed up with through Stripe.

Credit card info was inputted wrong and our system did not return an error message. You can check if your account is active with this link: https://io-fund.com/account. We have fixed this to where an error message is now returned.

Attempting to use the Beth.Technology password on IO-Fund.com. Due to security reasons, passwords can’t be transferred and you must set a new password for the new website.

To access the new site, you must set a new password. To set a new password, go to https://io-fund.com/welcome.

We plan to check in periodically with our returns. Please note, audited returns supersede any information we have provided that was unaudited. We pay an accountant to get our returns audited to build trust with readers and reduce any chance for error as we hold equities and crypto in separate accounts.

Our fund was founded on May 9, 2020, and this marks the inception of our fund to where the equities were combined. This is the date the auditors preferred to track returns for 2020, which makes sense because it represents our true YTD for the fund in 2020.

Below are the terms of the audit and our results from May 9, 2020 through December 31, 2020. We narrowly beat Ark with results of 115.5% compared to Ark Innovation’s returns of 113%.

Please note, although we are sharing our final number with you as a courtesy, we own the audit and we do not give consent for you to share this publicly. Although we will likely discuss our final number from time to time, the terms in which we do this are determined by our agreement with the accountant.

The performance of Ark Innovation from May, 2020 through December 31, 2020 was 113.5%

YTD Returns

We were up nearly 2X the Nasdaq on March 19 and more than 4X the Nasdaq with crypto on March 19. You can see this screenshot below.

We decided to start buying, which hurts returns in the short-term as we are fully aware the correction may not be over. Therefore, everything we buy right now immediately weighs on our results – whereas during an uptrend, what you buy immediately improves your results.

By March 19, ARKK was negative (1.7%) per Ycharts on equities alone compared to our positive 3.7%. With crypto and equities, our returns on March 19 is positive 15% with Bitcoin being up 96% and Chainlink being up 149% YTD.

After buying many equities last week, we have now dipped to negative (5%) on equities for March 26 compared to ARKK’s negative (8.5%). However, with crypto we are at positive 7.78% YTD with 12% allocation to crypto and 88% allocation to equities.

We started the year with a higher allocation to crypto than 12%, so the 7.78% YTD is conservative.

We hope our transparency and investment in an auditor demonstrates our integrity and builds trust with you. We realize you have a choice in who you subscribe to and we want you to know that we invest in our convictions and are right alongside you during the ups and downs. Competitively speaking, we think a research site that is audited is putting forth their best effort to earn your trust in what can be a very convoluted and (sadly) sometimes unprincipled space.

As we continue to build out our services with integrity, we believe the strength of our team will become even more apparent. Please keep in mind, we launched in July of 2019 and are about 18 months from the launch. I can only imagine what the team will be capable of over the next five years as we were comfortably positive with crypto during a major and severe selloff in tech.

We are also accomplishing this as a 4-person team compared to Wall Street funds who have hundreds of analysts contributing to portfolio decisions and machines calculating entries and exits.

We do understand that we are often painfully slow in making changes to our site and the forum. We do this to make sure we don’t take our eye off the ball with the market.

With that said, the site is now live and the new customized forum will be launched in May. We think the new site is simple, effective and fast to load. The forum is an important project that we plan to continually improve on and we can’t be more excited to share this with you in May.

Thanks for your readership and for being part of the I/O community.

We began covering cryptocurrency and the blockchain after a month of launching our premium site because we felt it was an important component to any tech portfolio. The debate around crypto/blockchain is distracting investors from the opportunity that the blockchain will deliver.

Below is a full-length analysis on Ethereum as the Ethereum Network is going through extensive iteration that will propel the platform to become the backbone for crypto payments and decentralized apps. If you like my Nvidia thesis on the CUDA platform for AI development or if you understand the Apple thesis over the past ten years which centers around developers supporting the iOS ecosystem (rather than only the iPhone) – then you should like Ethereum.

The blockchain is coming … and debates over Bitcoin can’t stop the blockchain from maturing. If you don’t like Bitcoin, then that’s okay. But it shouldn’t deter you from considering blockchain investments. Ethereum is another choice and Chainlink is one I’ve been particularly keen on. In fact, Chainlink was my choice for the inaugural LTBH one-hour webinar because I think there could be notable upside and I don’t want my subscribers to overlook the technology because it trades as a crypto.

In my opinion, Ethereum also has notable upside and we want the I/O Fund to have some allocation here. As many of you know, we lean heavily on Knox for entering, exiting, or trimming crypto as it’s especially volatile. We will not necessarily enter right away — and also be prepared for Knox to require more than one entry if the crypto market turns. However, it’s well worth the effort as its early days for the blockchain.

You could see us trim Bitcoin and add to Ethereum in an attempt to participate in the blockchain trend while having proper allocation as Bitcoin had neared 10% of our portfolio and it’s now at 7% through trimming. Ethereum also helps diversify us for decentralized applications and other tokens. Or, we could add more to LINKUSD.

The analysis below describes what Ethereum is setting out to achieve and why some of the best blockchain investments are not likely to come from a traditional stock (they’ll come from crypto). In other words, if you want to participate in the early blockchain trend, then you’ll have to get comfortable with crypto.

History of Ethereum

In October of 2008, the markets came to the realization that the Lehman Brother’s bankruptcy was likely not an isolated incident. While the world was scrambling to discern the severity and extent of financial crisis, the stock market hit a new low that resembled a genuine panic. At the same time, a mysterious person or group of people, under the pseudonym of Satoshi Nakamoto quietly published a white paper. This report described a new monetary system that would rely on a decentralized network of computers to verify all peer-to-peer value exchanges through a digital token called bitcoin.

Largely unnoticed at the time, while the centralized banking system was in a full melt down, Bitcoin was suggesting a new monetary system that could make the centralized banking system largely obsolete. It wasn’t until January of 2009 that Bitcoin was released with an initial market price of $0.08/bitcoin. Still, it took just over 10 years, and over 15,800,000% appreciation before Bitcoin’s stated thesis gained public acceptance from institutional buyers.

Next to Bitcoin’s dominance, the undisputed runner-up is Ethereum, which is the second most valuable coin in terms of market cap, as well as public mindshare. Without a full understanding of why this is, most people would assume that Ethereum must have been launched soon after Bitcoin. This is not the case.

The second cryptocurrency to launch in April of 2011 is known as Namecoin. Nearly identical to bitcoin, including the same number of coins in existence, it’s stated goal was to improve anonymity for miners. Roughly six months later, Litecoin was launched and was able to take on the moniker of being known as silver to bitcoin’s gold. It also was similar to bitcoin, but offered double the number of coins, and allowed for quick mining transactions.

Most altcoins track a similar path – using the same, if not closely identical mathematics in an attempt to provide slight variation of bitcoin and compete as the dominant cryptocurrency of choice. We saw hundreds of these alt coins hit the markets prior to Ethereum’s launch in 2015, including Ripple, Monero, and Dash. Unlike the previous altcoins, what Ethereum offers is a network and platform for developers to expand the use of blockchain rather than to compete with Bitcoin as a cryptocurrency.

Ethereum Network 2.0

The primary difference between Ethereum and Bitcoin is that Ethereum is not trying to compete as a currency. The focus of Ethereum is on its network, not the coin. Butkin’s vision is to create an open network for decentralized applications (dapps[1]) and smart contracts based on the Turing complete programming language Solidity.

The main issue that Ethereum has had to overcome is the constraints in transactions per second (TPS) and how to overcome the high energy costs of mining that comes with decentralized security. The network simply couldn’t scale without the recent release of Ethereum 2.0.

To understand this further, we need to break down Proof of Work (PoW) and Proof of Stake (PoS). The previous method for decentralization was run through PoW, which is an algorithm that requires a miner and large amounts of computational power to create blocks and to confirm transactions. Due to the high costs in terms of both speed and energy, the Ethereum Network struggled to scale. Last November, Ethereum 2.0 was released and introduced PoS. Instead of a large consumption of energy, PoS requires a financial commitment of 32 ETH to become a validator. The network required 524.224 ETH or 16.384 validators by December 1st in order to start the new phase of Ethereum 2.0. As of mid-December, more than 1.1 million ETH had been staked from 33,000 validators. The most recent number is 1.6 million ETH.

The Ethereum that is staked in the new protocol receives interest with early yields up to 20%. The more Ethereum that is staked, the lower the interest. Interestingly, Ethereum has not built the algorithm that will allow you to unstake them, so this is a long-term bet on Ethereum for anyone that is staking their coins.

Shards are another critical improvement for network bandwidth and the low transactions per second (TPS) as Ethereum 2.0 (ETH2) allows for improved data processing. Nodes in the previous network must download a transaction, calculate it, archive it and read every transaction in Ethereum’s history, which is terribly inefficient. Shards create a subset of the network where nodes are dispersed for more efficient processing. The Beacon Chain ensures the nodes are synchronized and the validators are reporting the blocks of transactions.

The original Ethereum network will run in parallel with ETH2.

Phase 0 of Eth2 went live on December 1st and there are a total of four phases. Phase 0 included the launch of Proof of Stake Beacon Chain.

The most recent road map released by Ethereum does not show the subsequent phases. The shaded green shows the current progress in the link provided. Missing deadlines is an issue with Ethereum so perhaps the removal of these phases is to make it easier on the team/network.

The term Rollups refers to ZK Rollups, which allows for hundreds of transfers to be rolled into a single transaction. This will replace Plasma, the current option where only a single transfer is made per transaction. In this case, the smart contract will verify all of the transfers in the Rollups. The goal is to reduce computing and storage resources by reducing the amount of data held in a transaction.

In the ZK-Rollup scheme, a transactor and relayer are needed. The transactors create a transfer and broadcast it to the network. In this case, a shortened 3 or 4 byte indexed version of the address helps to reduce resource needs. The relayers collect hundreds of transfers and roll them up, essentially, to generate a hash that compares a snapshot of the blockchain before the transfers and a snapshot of the blockchain after the transfers. In most cases, the transfers will be recorded by a change in the wallet values. The hash that represents the wallet values or the delta to the blockchain is called SNARK proof. The changes to the hash are reported to the blockchain.

Relayers are established by staking a required bond, or token amount, in the smart contract. The result will be fewer transaction fees that are processed faster than the previous Plasma framework. In the ZK-Rollup framework, blocks are computed in a parallel computing model that lends itself to decentralization. There will be less data than the previous framework which increases throughput and scalability.

Zero-knowledge proof techniques use mathematical equations for authentication without requiring passwords or sensitive information. The words “Zero-knowledge” means that the verifier can prove the first party can be trusted without revealing sensitive information. This is done through probabilistic assessments where the validity has a high probability.

Zero-knowledge is essential to cryptocurrencies because a crypto transaction can be verified without revealing information about where the payment came from, where it was sent or how much currency was exchanged. Bitcoin does not use zero-knowledge as all of this information is revealed and recorded.

The Ethereum network has more security risks than the Bitcoin protocol. The initial setup of ZK-Rollups assumes a trusted state and relies on a small group of developers to establish this initial trusted state and one of the developers could manipulate the code. The initial setup is not a decentralized.

Quantum computing could crack ZK-Rollups if the correct hash is guessed by the computer. This is more likely than guessing an encrypted protocol.

Ethereum is becoming the blockchain of choice through the Enterprise Ethereum Alliance, which is a list of over 200 companies, including AMD, Banco Santander SA, FedEx, Intel, JP Morgan, Microsoft, and VMWare. These companies have agreed to build smart contracts on the Ethereum blockchain, further increasing the value of Ethereum. We think the number of endorsements as Ethereum 2.0 is built out.

Decentralized Finance (DeFi)

DeFi, or decentralized finance, began in a telegram chat between Ethereum developers in August of 2018. The term refers to the open ecosystem of financial applications built on the Ethereum blockchain. Peer-to-peer (P2P) is used interchangeably as the network is verified by peer computing systems rather than one centralized source.

1) No Custodian. In other words, there is no bank or custodian in-between transactions. Each individual controls access to their own crypto, transactions and data around their activity.

2) The network is Global. There are no borders, exchange rates, currency differentials, or waiting for global transfers. Everyone on the network, regardless of country, will be able to transact instantly with anyone else in the world with ease.

3) The network is open source. This allows developers to view the code of any and all applications on the Ethereum blockchain and for the ecosystem to evolve.

4) Decentralized network. The Ethereum blockchain is run off of thousands of “nodes.” These nodes are constantly computing the transactions within the blockchain from around the world, making it nearly impossible to hack as well as regulate.

There is $24 billion locked into DeFi projects as of 2020.

Decentralized applications (dapps)

We discussed the difference between centralized and decentralized in the Chainlink webinar and why decentralized results in a more secure protocol or transaction. Ethereum’s network is often called a platform or the “world’s computer” because it allows for decentralized applications. Rather than having backend code on a centralized server, backend code is run on a decentralized network when built for the Ethereum platform. Developers use the Ethereum blockchain for data storage and smart contracts for the app logic.

We also discussed smart contracts on the Chainlink webinar. Ethereum is primarily set up for currency right now while Chainlink addresses off chain data for non-currency smart contracts. However, the principal is the same where there is a set of rules which self-execute like a vending machine. Dapps will rely on smart contracts.

Dapps deployed on the Ethereum network are controlled by logic written into the smart contract and cannot be altered by the developer. Smart contracts function like APIs (we also talked about this in the Chainlink webinar). This allows applications to build on one another similar to the way applications use APIs today; except blockchain applications will build on smart contracts.

The front-end application can be written in any language with calls made to the backend. The main qualities are that the applications are decentralized, can perform any action given the required resources (whereas Bitcoin is not Turing complete) and are executed in a virtual environment such as the Ethereum Virtual Machine. The virtual machine acts as a buffer to where if the application is faulty, it does not affect the blockchain network.

There are a few key benefits to dapps:

• Dapps are more secure and inherently protected from denial-of-service attacks.

• Censorship will be nearly impossible as a single entity will not be able to block users from utilizing the blockchain.

• Fraud and other malice will be prevented as the data has complete integrity from the decentralized and cryptographic qualities of the blockchain.

• Because smart contracts are self-executing, they remove the need for a centralized institution. Realworld identities can also be anonymous with dapps.

There are also some drawbacks to dapps:

• Most developers do not want to relinquish complete control over their creation*.

• If there is a bug that need to be fixed, that developer is unable to take back control of the dapp once it’s launched onto the Blockchain*.

• Dapps will need Ethereum 2.0 to achieve its final phase as applications will create too much network congestion at the 10-15 transactions per second.

• User experience needs to evolve in order for users to interact with the blockchain in a secure fashion.

• Some developers may utilize centralized servers for the frontend or to store business logic which could eliminate many of the decentralized security/anonymity benefits of the blockchain.

There are some applications that are decentralized but not built on the blockchain, like BitTorrent for peer-topeer file sharing. Tor is open-source software that enables anonymous communication and is also decentralized.

Some of the early DeFi applications allowed for seamless swapping of coins for Ethereum and lending of collateralized loans with built in interest payments to the borrowers. Contracts can also be created between crypto and non-crypto assets like gold, silver, stock, currencies, etcetera. People are allowed to deposit what are known as “synths”, or synthetic coins that allows for the contract to be written and then exchanged. This allows individuals to trade assets on Ethereum without the intermediary of exchanges and broker/dealers.

There are even applications known as yield farms that allow investors to deposit their crypto into liquidity pools, which are loaned out, which allows them to receive yields on their crypto.

Conclusion:

The Ethereum Network is becoming the backbone for decentralized finance and decentralized applications. Ethereum 2.0 needs another year minimum or about three years maximum to reduce energy use and increase throughput for transactions per second (TPS). Once this is achieved, Ethereum will be able to process payments faster than Visa, Mastercard or Paypal combined– going from 15 transactions per second to 100,000 transactions per second. For reference, most major credit card companies process about 2,000 TPS with 5,000 TPS as the upper limit.

Cardano and Polkdot are competitors yet Ethereum is receiving global acceptance among developers and major endorsements from companies who are likely to be the first to develop dapps and embrace defi, as well. If Ethereum 2.0 delivers what it promises to, I believe ETH will become the backbone for the blockchain and this will be hard to disrupt.

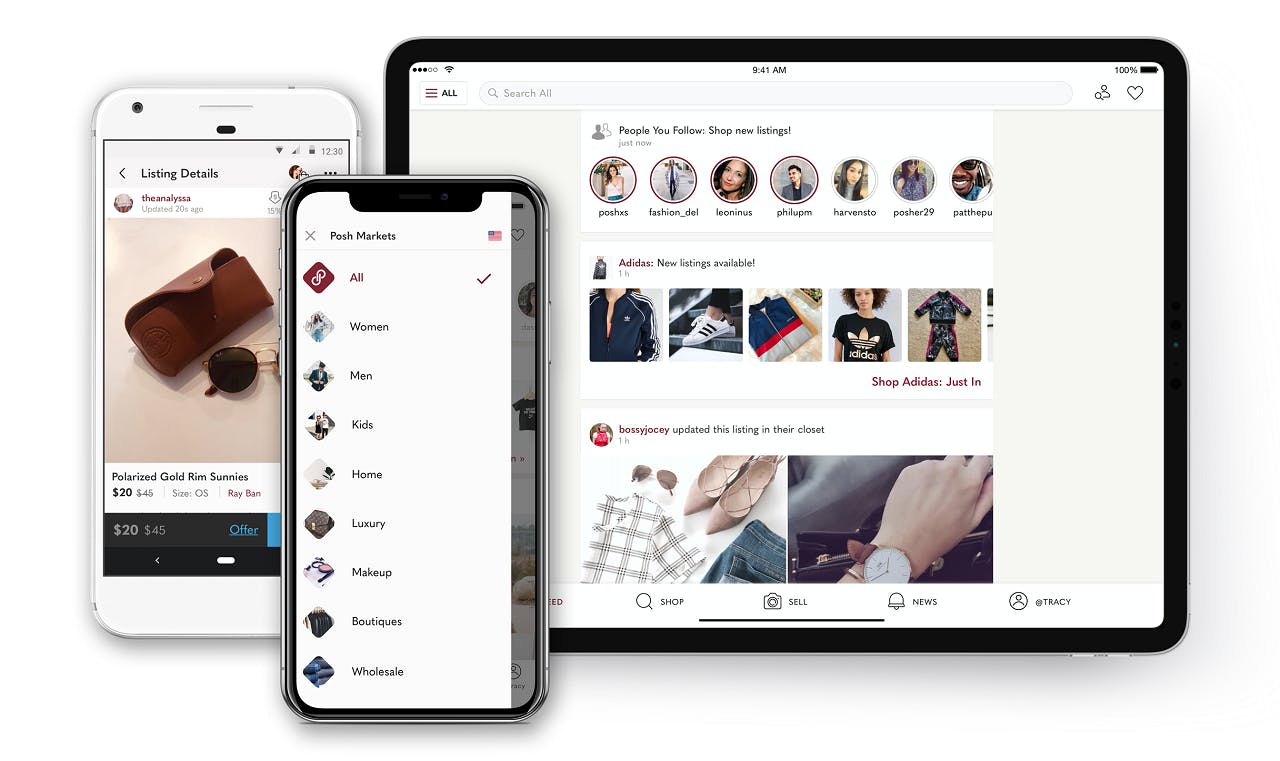

Poshmark sits at the intersection of three key trends: non-new, sustainability, and social e-commerce. A consumer-to-consumer online marketplace for pre-owned items, Poshmark is a fashion-oriented platform that offers apparel, accessories, beauty and wellness, footwear, home goods, toys and games, and a new pets category.

The app makes online shopping social, with a user experience similar to Etsy, Instagram, and Pinterest. Poshmark encourages users to follow each other, and like and share items for sale in users’ closets. It also offers video through Posh Stories, free virtual events known as Posh Party Live, and virtual meetups. Prior to the pandemic, Poshmark also supported in-person events.

As the largest fashion-oriented online C2C marketplace in the U.S., Poshmark’s IPO generated significant excitement. The company initially planned to offer 6.6 million shares at $35 to $39, but due to demand priced the IPO at $42.

In its first day of trading Jan. 14, the stock opened at $97.50 and closed at $101.50, with an intraday high of $104.98. The stock has been falling ever since and reached a new low March 25 when it closed under $39.

Now that the valuation has come back down to earth, Poshmark may offer a good opportunity for investors who believe the future of ecommerce will be social. Below we look at competitors, fundamental, quarterly results, market opportunity, and potential tailwinds.

Ebay Posts Record Growth

To understand the potential opportunity in Poshmark, first we need to look at one of the largest online marketplaces in the world, Ebay. As more shopping moves online, specialized ecommerce platforms like Poshmark are fighting for current and potential Ebay customers.

Founded in 1995, Ebay is the grandfather of the online auction. Like its much larger rival, Amazon, Ebay facilitates B2C and C2C sales through its website and makes money on transactions. Unlike Amazon, which has strict guidelines around used items, sellers can list almost anything on Ebay.

But it has faced stiff competition from a new generation of online marketplaces that cater to niche interests, including public companies like Poshmark, Mercari, and The RealReal, which encourage users to clear their closets to make extra cash.

In the universe of private companies, there is also a platform for every niche, from gently used children’s apparel on Kidizen to used tech on Gazelle.

After years of declining growth, Ebay may have turned a corner last year. Due to tailwinds from Covid-19 and the resulting economic lockdown, the company reported double digit revenue growth in 2020. Here are the full year 2020 highlights:

Revenue was $10.3 billion, up 19% on an as-reported basis.

Gross merchandise volume (GMV) was $100 billion, up 17% on an as-reported basis and an FX-Neutral basis.

GAAP and non-GAAP operating margin were 26.4% and 31.3% respectively.

Due to a strong holiday season, Ebay also reported strong Q4 results:

Revenue of $2.9 billion, up 28.1% YoY, beat expectations by $160 million.

Non-GAAP EPS of $0.86 beat by $0.03.

GAAP EPS of $1.12 beat by $0.48.

GMV was $26.6 billion versus consensus of $25.18 billion.

Annual active buyers grew 7% to 185 million.

Still, this pales in comparison with high growth e-commerce marketplaces, not all of which are young companies.

Overstock, founded only a few years after Ebay in 1999, grew 2020 Q4 revenue 84.4% YoY. Wayfair, founded in 2002, grew Q4 revenue 45.1% YoY. Fintwit favorite Etsy, founded in 2005, grew Q4 revenue an astounding 128.7%.

With the tailwinds from Covid looking ready to expire for Ebay, and the entire ecommerce sector, the market is dubious about whether Ebay can continue growth and beat tougher comps. Executives were upbeat in the most recent report, noting the progress the company made in executing on the three pillars of its long term vision:

Defend the core business by building compelling next-gen experiences.

Become the partner of choice for sellers.

Cultivate lifelong trusted relationships with buyers.

It is clear from the report that Ebay executives are aware of the risks to its core business from other ecommerce platforms. To execute on its strategic vision, Ebay is focusing on seasonal opportunities and non-new, including refurbished, which was a top trend for holiday shopping.

How Big is the Opportunity in Non-New?

The online U.S. resale market for apparel and footwear was estimated at $7 billion in 2019 and is expected to grow to an estimated $26 billion in 2023, according to data from GlobalData cited in Poshmark’s S-1.

A report last June by Poshmark competitor Thredup, which filed for IPO recently and is expected to begin trading on the Nasdaq March 26, valued the secondhand apparel market at $28 billion and predicted it would reach $64 billion within five years. It said the resale market grew 25 times faster than the overall retail market in 2019, with an estimated 64 million people buying secondhand products.

Good opportunities attract competition, and competition for the online secondhand apparel and accessories market is fierce.

In addition to Poshmark, Depop, Grailed, Mercari, Thredup, Tradesy, The RealReal, other notable competitors include Vestiaire Collective, a French company that recently raised $216 million in fresh funding, and Vinokilo, a German company that has not raise any venture capital and has been consistently profitable.

Luxury brands and platforms are also starting to consider controlling the lifecycle of their own products. For example, luxury marketplace Farfetch launched Farfetch Second Life in November 2020. It allows customers to trade in high-end bags in exchange for a credit to shop new collections.

Authentication is a key feature of the luxury resale market, such as designer handbags, shoes, and apparel. As part of its strategic vision, Ebay rolled out its own authentication program for secondhand watches over $2,000 and sneakers over $100 last fall.

Based on the results, it is a potentially profitable niche for Ebay, and validates part of the opportunity Poshmark and its competitors are trying to exploit. Ebay saw a double digit increase in GMV growth in Q4 versus Q3 for watches over $2,000, while sneakers over $100 grew triple digits YoY in Q4.

Investors should note that authentication has been controversial for sites such as The RealReal, an online and brick-and-mortar marketplace that offers authenticated luxury clothing, jewelry, and watches.

The RealReal has been plagued by claims in the media, and on social platforms, that fraudulent products slip past low paid authenticators and are sold on the platform. The RealReal is also being sued by Chanel, which alleges that The RealReal is selling counterfeit Chanel bags.

Poshmark has faced similar claims from users. So far, accusations against The RealReal seem to be more prevalent and much higher profile. The potential risk is real to any company that claims 100% authentic designer goods.

Tailwinds from Sustainability

Consumers are increasingly aware of the fashion industry’s impact on the environment. The U.S. sustainability market is projected to reach $150 billion in sales this year, according to Nielsen.

In Europe, 67% of surveyed consumers consider the use of sustainable materials to be an important purchasing factor, and 63% of consumers consider a brand’s promotion of sustainability in the same way, according to July 17 report from McKinsey & Company on Sustainability in fashion.

Secondhand is inherently more environmentally friendly, as it extends the life of consumer products.

Seller Ecosystem: Size is a Moat

Sellers create marketplaces by offering the products that attract consumers. That is why one of one of Ebay’s three key priorities for its long term vision is becoming the partner of choice for sellers. In a virtuous cycle, sellers create the marketplace that keeps buyers coming back, which keeps sellers engaged.

For example, of all buyers who activated on Poshmark between 2012 and 2018, 34% also activated as sellers by the end of 2019. Of all sellers who activated between 2012 and 2018, 39% activated as buyers by the end of 2019, according to the company’s S-1 Registration Statement.

For sellers, every marketplace has advantages and disadvantages. Poshmark’s fees are less complicated than Ebay’s but significantly higher:

· Poshmark. For sales under $15, Poshmark charges a flat rate of $2.95. For sales above $15, the fee is 20%.

· Ebay. Ebay has been working to simplify its notoriously complicated fees. For most categories on Ebay, managed payments customers pay 12.35% up to $7,500, plus 2.35% on the portion of the sale over $7,500.

Poshmark has been criticized for its high fees. But the company acknowledged in its S-1 the potential for future reductions:

“In the future, we may be unable to attract new sellers or retain current sellers at these fee levels, as they may choose to sell their merchandise on other platforms with lower fees. Furthermore, pricing pressures and increased competition generally could result in having to decrease fees, which could cause reduced revenues, reduced margins, or losses, any of which would harm our business, results of operations, and financial condition.”

For Ebay, size is a moat. With its gargantuan user base, that moat is not easy to disrupt. The same may be true of Poshmark, which is the leading C2C marketplace for fashion, according to data from May 2020 from Statista, a German company that specializes in market and consumer data.

Founded in 2011, Poshmark has grown significantly larger than other fashion oriented secondhand marketplaces, most of which were founded around the same time.

Notable competitors in secondhand fashion include Depop, founded in 2011; Grailed, founded in 2014; Mercari, launched in the U.S. in 2014; The RealReal, founded in 2011; Thredup, founded in 2009; and Tradesy, founded in 2009.

Mercari, a Japanese company, had 3.4 million monthly active users in 2019, according to a company press release. It can be difficult to sell on platforms with much smaller user bases, although it helps to offer desirable brand names, according to user reviews.

Some sellers dislike Poshmark’s social aspects—it creates extra work by forcing sellers to like and share items, and negotiate with potential buyers—the size of the marketplace means sellers and buyers keep coming back. In 2020, Users who spent an average of 27 minutes daily on the app continue to re-engage over time as buyers and sellers, according to Poshmark’s Q4 report.

Fundamentals: User and GMV Growth

Poshmark launched in the U.S. in 2011 with a valuation of more than $600 million. The company has an asset light model and does not own or manage inventory, as items are listed, sold, and shipped by sellers.

In May 2019, Poshmark expanded to Canada, growing its community to more than 1.4 million users in that country within the first year.

International GMV was $6.4 million in 2019, according to the company’s S-1. It grew to $32.6 million in the nine months ended Sept. 30, 2020. For each of these periods, revenue from international operations was less than 10% of the company’s net revenue.

As of Sept. 30, 2020, Poshmark had 31.7 million active users in North America, 6.2 million active buyers, and 4.5 million active sellers, according to the S-1.

Executives did not update the total number of active users or active sellers in the Q4 report. It did note an increase in active buyers to 6.5 million, a 20% increase YoY from 5.4 million in Q4 2019. Social interactions also grew 48% to 30.4 billion in 2020, according to the Q4 report.

Poshmark Active Buyers (Thousands)

Source: S-1

Poshmark doubled the number of active buyers from June 30, 2018 to June 30, 2020, which it says has been a key driver of GMV growth.

GMV in Millions

The company plans to continue growing through increased engagement, new product categories, and international expansion, starting with English-speaking countries. Last month, Poshmark launched in Australia.

Poshmark chose Australia as its first market outside of North America due to the well-established thrift shop culture, high rates of e-commerce adoption, environmentally conscious consumers, said Chief Executive Officer Manish Chandra, in an interview with Bloomberg.

Quarterly Results and Valuation

Poshmark had a market capitalization of $3.35 billion and an enterprise value-to-sales ratio of 12.60 as of March 24. The company reported Fiscal Q4 2020 earnings March 11 for the period ending Dec. 31.

In Q4, Poshmark achieved its third consecutive quarter of profitability and had revenue of $69.3 million, a 27% increase from $54.7 million in the fourth quarter of 2019, according to the report.

Income from operations was $1.6 million, compared to a loss of ($15.1) million in the fourth quarter of 2019. GMV was $387.2 million, an increase of 28% YoY from $302.1 million in Q4 2019. Quarterly GMV has increased YoY for the past 11 quarters.

Adjusted EBITDA was $4.2 million which increased from a loss of ($12.6) million in the fourth quarter of 2019. Adjusted EBITDA margin was 6.1%.

GAAP diluted net loss per share attributable to common stockholders was ($0.31). Non-GAAP diluted net income per share to common stockholders was $0.05 a share and excludes non-cash expenses related to convertible notes and warrants due to the increase in the fair market value of our common stock share price.

For the full year 2020, income from operations was $23.4 million, compared to a loss of ($49.8) million in 2019. Net revenue was $262.1 million, a 28% increase YoY from $205.2 million in 2019.

GMV was $1.4 billion, an increase of 29% YoY from $1.1 billion in 2019. GMV has increased YoY since the company was founded in 2011.

Trailing 12 months Active Buyers reached 6.5 million in the fourth quarter of 2020, a 20% YoY increase from 5.4 million from Q4 2019. The company did not update the number of active sellers. Adjusted EBITDA was $34.3 million which increased from a loss of ($37.1) million in 2019. Adjusted EBITDA margin was 13.1% in 2020.

GAAP diluted EPS attributable to common stockholders was $0.22. Non-GAAP diluted net income per share to common stockholders was $1.25 a share and excludes non-cash expenses related to convertible notes and warrants due to the increase in the fair market value of our common stock share price, and the impact from the undistributed earnings attributable to participating securities.

Cash, cash equivalents, and marketable securities were $262.1 million as of Dec. 31, 2020. During the third quarter, Poshmark issued a $50.0 million three-year convertible note which converted into 1.4 million shares of Class A Common Stock upon completion of the IPO on Jan. 14, 2021.

Guidance for Q1 2021 is $76.5 at the midpoint versus $80 million expected, with adjusted EBITDA of $1.5 million at the midpoint.

The company plans to continue executing on its four growth strategies: focus on innovation to drive user engagement, growing international footprint and capability, growth through category expansion, and deliver robust, easy-to-use, effective seller services, according to the report.

As part of that plan, in 2020 the company launched two new product categories: Beauty & Wellness and Toys & Games and launched several new features. Poshmark also completed the rollout of “Posh Stories,” the company’s first video feature which enables sellers to showcase and sell their listings with short videos and photos, released “Drops Soon,” feature that allows Poshmark sellers to pre-market items not yet available for purchase, and launched Reposh, a feature that provides users with a one-click way to resell items purchased on the marketplace.

Conclusion

Poshmark is the largest online C2C marketplace in the U.S. that specializes in fashion, in a space with fierce competition. Its success is not limited to the U.S. After expanding to Canada in 2019, Poshmark grew its community there to 1.4 million users within the first year. Users apparently enjoy the social aspect of the platform, which uses an asset light model that been profitable for the last three quarters.

The pandemic has created uncertainty for Poshmark, and the entire ecommerce sector. But with the recent expansion to Australia, and the launch of new categories and features, Poshmark has room to grow. It benefits from long term tailwinds, including an increased interest among consumers in sustainability and the rise of social commerce.

Some investors have criticized the company’s social platform, saying it is a waste of time for sellers who will leave the platform. Poshmark has also been criticized for its high fees. We think these are relatively minor complaints about a platform with a record of success.

Any company can lose market share to competitors. But Poshmark’s competitors have a lot of catching up to do. Now that the valuation has come down to earth, and sentiment with it, the stock may provide a good long-term opportunity—even if the growth is not what hypergrowth investors are used to.

Disclaimer: This article represents the opinion of the writer, who may disagree with the official position of Beth Kindig and I/O Fund. Jessica Ablamsky does not currently own shares of Poshmark but may initiate a position within the next 72 hours. Beth Kindig and the I/O Fund does not currently own shares of Poshmark. The content in this article is intended to be used for informational purposes only. The author has not received any compensation from any third party or company discussed in this article. The content is the expressed opinions of the author and is intended for educational and research purposes. Any thesis presented is not a guarantee of any particular stock’s future prices, so please factor this risk into your own analysis. It is very important that you do your own analysis before making any investments based on your personal circumstances. The author is not a licensed professional advisor. Please seek counsel form a licensed professional before acting on any analysis expressed in this article, to see if it is appropriate for your personal situation.

Long term technical signals suggest the current selloff is a buying opportunityLong term technical signals suggest the current selloff is a buying opportunity

Coming out of the 2008 Financial Crisis, we saw a shift from value to growth for the first time since the 90s. Growth stocks took the lead and have been the general theme of the current secular bull market that we are in. With a multitude of tech focused microtrends like the internet, mobile, social media, e-commerce, now cloud and soon to be 5G and AI, the tech sector has led growth stocks.

From a broad market perspective, the NASDAQ100 (NDX), and index of predominantly large cap stocks, has been the most important index to track within the current cycle. It has led the broad market into and out of almost every major correction since this bull market began.

This pattern has even continued since the quick bear market in March of 2020. From peak to trough, while the S&P 500 saw a 35.40% drawdown, the richly valued NDX only saw a 30.50% drawdown. Since the March 23rd low, we have seen a consistent trend where the NASDAQ100 has led us into each correction and also bottomed before the S&P 500.

However, since the recent correction began on February 16th, we have seen a meaningful shift from growth to value. Where the DOW is at new highs, the S&P 500 and DOW Transports are down less than 2%, while the NASDAQ100 is still about 7% away from new highs.

This is a meaningful rotation, which we see as healthy. The microtrends in tech are not over or at the end of their cycle, regardless of stock prices. Also, we want to see as many sectors and stocks participating in this bull market, which is happening.

Considering the importance of tech’s leadership, as well as the overall weight of tech within the S&P 500, which currently sits at about 24%, without the NASDAQ 100 participating in new highs, I would consider any bottom to be suspect. For this reason, we believe tracking the NASDAQ100 to be crucial right now in order to glean broad market cues.

I/O Fund has been preparing for a correction since late February. We built up a nice cash position, which we were vocal about with our readers as well as on Twitter (hereherehere). We also added a series of hedges prior to the selloff, and have recently added them back due to the possibility of a lower low. As of now, the long-term technical signals, and trend is still up. This suggests the current selloff is a buying opportunity, which we have been taking advantage of.

NDX: Levels to Watch

From a technical perspective, there are two scenarios we are tracking:

The correction is over. For the green count in the chart above, we finished the final leg in the March 5th correction. If NDX holds 12,600 and we see a breakout above 13,300, the low is likely in for this correction. To confirm this scenario, we need NDX to breakout above 13,300, at which point our small hedge will come off.

NDX makes a new low. If NDX breaks 12,600, that would put us in the red count. This count has us in the final leg of the correction, with a potential bottom at 11,715 to 12,050.

Regardless of what path NDX takes, we view this pullback as a buying opportunity and when the correction is complete we expect the uptrend to resume. We have been building key positions as we feel you can’t time the market and you most certainly can’t time a bottom.

There are many tools we use to guide our entries as well as risk management. One is the RSI, which I believe will be a key technical indicator to focus on based on the pattern in the daily chart. The trendline that was acting as support has become strong resistance. NDX needs to break back above the trendline before we can call this correction over. Furthermore, NDX has major support at the blue line. This was the final capitulation point for the March 2020 lows. If NDX reaches that level, we will take it as a strong buy signal.

Disclaimer: Beth Kindig and the I/O Fund currently owns shares of TSLA. The content in this article is intended to be used for informational purposes only. The author has not received any compensation from any third party or company discussed in this article. The content is the expressed opinions of the author and is intended for educational and research purposes. Any thesis presented is not a guarantee of any particular stock’s future prices, so please factor this risk into your own analysis. It is very important that you do your own analysis before making any investments based on your personal circumstances. The author is not a licensed professional advisor. Please seek counsel form a licensed professional before acting on any analysis expressed in this article, to see if it is appropriate for your personal situation.

Since the market topped on February 16th, the current correction is a very different experience depending on if one’s style of investing (value or growth). While the S&P500 only dipped 5.6% and is currently at new highs, the tech-heavy NASDAQ100 dipped 12% from peak to trough, and is still 7% from new highs. After value has underperformed for years, we are finally seeing a meaningful rotation out of tech and into beaten down value names.

The story on the rotation has to do with the quick rise in the US 10-year treasury yield. There are many reasons why bonds are being sold off, which inversely pushes up yields – inflation pressure has the bond market believing the FED will have to raise rates, which would likely stop this economic expansion. Also, the amount of fiscal debt written since the pandemic is creating a glut of supply, which the FED will likely not be able to fully absorb and this will put pressure on rates

Regardless, since many high growth stocks are projecting positive cash flow into the future, higher yields on longer duration bonds will affect future cash flows, causing a reset of current valuations. While the speed of the rise is unusual and unnerving to some investors, it is important to zoom out to gain some perspective on the recent move in yields.

As we can see above, the US 10-year treasury yield is still at historically low levels. In the chart above, bear markets are highlighted in gray. Going back to 1970, we have never seen a bear market begin with a US 10-year treasury yield below 3%. Our current rate is around 1.75%.

Further assurance comes directly from the Fed Chair, Jerome Powell, when he recently said the Fed expects to observe a momentary bump in inflation in March and April as the $1,400 stimulus checks shows up in economic data, but that they are not concerned about inflation rising above their 2.5% tolerance threshold. If inflation start to rise more than expected, Fed officials believe they have the tools to control it.

The Fed further claimed that they will be able to control inflation and has stated they will want to see maximum employment before changing their policy. This suggests it could be at least 2023 before we see major policy changes from the Fed, which is in line with the timeline they have outwardly discussed.

What’s Next?

With numerous microtrends in play, and recent earrings reports confirming or even raising future guidance, we view this correction in tech stocks as normal and temporary. We believe central banks are and will continue with an accommodative monetary policy for the foreseeable future. Corrections in growth stocks are not uncommon or unusual, no matter how painful they may be. A short-term price correction does not ultimately affect the underlying businesses of the stocks that we own.

In 2019, we saw a similar correction in tech growth. That year, the focus was on cloud pure plays, where the popular narrative at the time was stressing the overvalued cloud stocks as the neo-bubble stocks. While the S&P500 dipped 6.6%, and quickly recovered, many names like Twilio, Zoom, Fastly, Shopify, Okta, etc. saw corrections between 30-50%.

Our portfolio is geared towards taking advantage of powerful, long-lasting industry microtrends that will shape future generations. It is therefore illogical to stress over daily price movements in these innovative companies.

Growth Vs. Value and the NASDAQ100

Since the current secular bull market began in March of 2009, there is not an extended period of time where value has outperformed growth. This has been a growth driven bull market, with tech leading the way.

Even since the March low in 2020, tech has continued this trend. After the pandemic shutdown, many tech names saw outsized growth due to ongoing microtrends, while others saw a bump due to a stay-at-home economy leaning heavier on tech for support. Many of the value names were hit exceptionally hard, further widening this gap. With valuations stretched in the tech sector, rates on the rise and the economy opening up, we are starting to see a real value rotation.

As the chart above shows, the 14% Gap between Tech Growth and Value has nearly closed. In fact, while many growth names are down, much like the cloud names in 2019, value stock in the same timeframe are actually up.

We view this rotation as a positive sign for the overall market. We need all sectors participating in a bull market for it to remain healthy. Furthermore, we do not believe this market will continue with value leading the charge. There are simply to many exciting and profitable microtrends unfolding in tech, which we do not see ending anytime soon. Instead, we view this moment as an opportunity.

We have been focusing on the NASDAQ100 for several reasons. For one, it is predominantly tech focused. Also, it has been leading this bull market, and for the market to continue higher, we don’t see that being possible without the NASDAQ100. We really need it to join the other major indexes to new highs before we can count this correction as being over.

In short, if the NASDAQ100 can break above last Wednesday’s high at 13300, the probability increases that the low is in for this growth selloff. However, if we fail to break above this level, we could see another leg lower before we can write this correction off.

With the NASDAQ100 showing a negative RSI reversal signal, coupled with many charts we track whose current corrections appear to be incomplete, we may add hedges going into next week. We are 3% from the 13300 breakout, and about 10% from our downside target, if the NASDAQ100 cannot breakout above the 13300 region. This is the type of risk/reward we are willing to take for a hedge, if this final leg lower does unfold.

Relative Strength

Regardless, if we breakout and continue up, or need one final leg lower, we do not believe this bull market is over yet, and that this drawdown has provided some fantastic opportunities. In periods of market weakness, it is important to look at areas of strength. The future leaders tend to be stocks that go down less than their peers, bottom first, and lead out of a correction. That being said, the bounce off the March 5th low has provided some clues on where who might lead the next leg higher.

As the above chart shows, to lump all of tech into one category would be a mistake. Even though the S&P500 Tech Sector is showing poor relative strength in the chart above this year, as well as from the March 5th bottom, it’s important to identify what dominates that sector. Being a market cap weighted index, Apple and Microsoft makes up over 40% of the index, so it is heavily influenced by big tech.

If we dive into other microtrends within tech, there are a handful of sectors that are showing strong relative strength, even in light of the tech sell-off. What interests us are the sectors that are showing the most strength since the March 5th bottom.

Bitcoin/Crypto Currencies

The number one performer since March 5th is bitcoin/cryptos, and the businesses around this microtrend. Bitcoin is up over 58% YTD, and more notable is that it has continued its strength since the March 5th bottom. Bitcoin is our largest position, and though we are forecasting a bout of weakness in the near future, we do believe the uptrend will ultimately continue into 2022.

However, there are several businesses that benefit from the crypto market, such as Square, Silvergate Capital, eToro, Coinbase, Voyager Digital, just to name a few. We currently own Voyager Digital (VYGVF), which is a crypto exchange as well as a fintech company.

After being up over 500% YTD, we believe Voyager’s best days are ahead of it. It’s also the leader of the group just mentioned in terms of projected forward growth. If Voyager Digital continues with the revenue it already posted in February at $20 million per month, the valuation below will be cut in half.

China Tech and Green Energy

Another trend we have seen since the March 5th bounce is green tech and Chinese tech. In fact, they rank as the #2 and #3 micro sectors within tech since the March 5th bottom.

This falls in line with one of our favorite tends in 2021 – Chinese EVs. XPeng has been in a large downtrend, which we have thoroughly tracked and bought into along the way. Since the March 5th bottom, XPEV has bounced as much as 48%, showing outstanding relative strength. Nio has also bounced as much as 38% from the bottom. We used this bout of weakness in Nio to begin our position. Even if we do see another leg lower in the market, the reaction from March 5th further confirms the opportunity we see in the Chinese EV market in 2021, which we will continue to target.

You can read Beth’s analysis on XPEV and NIO here and here.

OTT/CTV Ads

Finally, OTT/CTV Ads has also shown considerable relative strength since the March 5th bottom. Going into 2021, it was one of our biggest convictions and we allocated our portfolio accordingly. This micro sector has been considerably strong YTD, outperforming all major sectors in the broad market, short of beaten down energy stocks. It currently ranks #4 in terms of strength since the March 5th bottom, suggesting that this trend still has more room to run.

We currently own Roku, Magnite, Fubo within this trend. Even after a considerable drawdown in these names, they are still showing outperformance against the NASDAQ100.

Stocks on our Radar that are Showing Solid Relative Strength

Two more stocks that made news from a relative strength perspective include UPST and VUZI. UPST recently raised 2021 revenue guidance by over 50% and the stock roared higher, while VUZI stock also reacted very positively to its earnings beat.

Conclusion

We do not believe that this is the end for tech leadership in the bull market. There simply too many important microtrends at play, and more about to go online. This rotation is healthy. We want as many stocks and sectors participating in the bull market, which is typically what we see going into the strongest leg of a bull market.

We believe this correction has provided a fantastic opportunity to buy shares of out-of-favor tech names, which we do not believe will stay out of favor for long. The relative strength in certain micro sectors is telling us what areas will likely lead into the next leg up, and we are pleased to see that they are lining up with Beth’s 2021 thesis so far.

After reaching a new all-time high of more than $61,200 per coin last weekend, Bitcoin is currently trading around $59,000.

After a large bounce off a low of $45,260, Bitcoin cleared the lower level we indicated in our last Bitcoin analysis: $53,000 to $56,000, which we used to trim our position. We stated the next level to watch is $70,000/$80,000 and we continue to believe that Bitcoin will make a local top.

After recent price action, my target is now $65,000/$75,000 before we potentially see a larger drawdown. We will continue to hold our position as long-term it will trade higher but we think there is an opportunity where we see Bitcoin trade at lower levels in the near future.

Below we look at what might be next for the world’s most popular cryptocurrency.

Levels to Watch

Bitcoin is now approaching our upside targets for the end of this larger 3rd wave, which is on the chart in blue. Several cues are pointing to this region, with a focus on $65,000, $75,000 and $107,000.

However, the internal momentum is weakening, which suggests that the lower targets are more probable than breaking the $100,000 region on this uptrend. The RSI may be particularly important. The RSI has respected the upward trend channel since the 3rd wave started in March of 2020. If this breaks to the downside, the 3rd wave is likely over.

Even more concerning is the negative divergences developing in the RSI on the daily chart. As the price makes a higher high, the RSI is making a lower high. This suggests that price is on faulty support at these levels.

Bitcoin is one of our largest holdings in our I/O Fund. We purchased Bitcoin in March 2020 at around $7,750 and sent an alert to our premium subscribers. We alerted premium subscribers for additional entries at around $10,000, $11,000, $12,000, $20,000, and $49,000.

Even with the potential for a larger drawdown in the near future, we do not have any intention to make any drastic moves with Bitcoin. We have trimmed some in the $55,000 region, and may trim some more if we reach the $65,000. However, we see any large drawdown to be an opportunity for Bitcoin and we will likely enter again if/when this happens.

Bitcoin is up almost 100% this year, and we’re long since $7,753 for a gain of more than 650% in our I/O Fund, which is invested in the most important tech microtrends.

While some traders were calling for a crash in Bitcoin after the last dip, we saw no reason to sell, and instead identified the $28,000 as a likely shallow bottom to target.

Download our free e-book on Bitcoin.free e-book on Bitcoin.

Disclaimer: Knox Ridley and the I/O Fund is currently invested in Bitcoin. The content in this article is intended to be used for informational purposes only. The content is the expressed opinions of the author and is intended for educational and research purposes. Any thesis presented is not a guarantee of any particular stock’s future prices, so please factor this risk into your own analysis.

The author is not a licensed professional advisor. Please seek counsel from a licensed professional before acting on any analysis expressed in this article, to see if it is appropriate for your personal situation.

Voyager Digital is a smaller cap that gives investors exposure to the Bitcoin and crypto trading trend at a reasonable valuation. The company offers zero commissions and more coins than its competitors, including the rumored $100 billion market cap Coinbase that is going public soon, Kraken and Gemini. The stock is listed on the OTC market, which is higher risk than the Nasdaq as these stocks tend to be thinly traded.

Voyager is a zero-commission competitor to Robinhood, and due to many PR mishaps, has opened a door for Voyager to become a replacement for customers who seek fewer politics around their crypto trading app.

Voyager also comes with the added benefit of offering 9% interest on stable coins as the company is a consortium for stable coins, including USD Coin (USDC) and Tether’s USDT, which have surpassed $7 billion in circulation. As such, it provides exposure to decentralized coins like Bitcoin and stable coins based on the fiat system.

Although I am personally in favor of decentralized crypto and not stable coins, Big Tech and the Fed are likely to put immense pressure on adopting stable coins. Voyager allows investors exposure to both at a market cap of $2.18 billion, at time of writing. You can read my Facebook Libra article here where I am especially against this company entering the stable coin market.

Below we explain what makes Voyager a compelling investment, including what it does, how it makes money, valuation, catalysts, management, and potential risks.

Voyager: Zero Commissions, More Coins

As longtime crypto investors, we know all too well the issues around Coinbase and the other sites. The primary issue is the commissions that Coinbase charges, which are exorbitant to say the least. To make a $5000 trade on Coinbase, you will be charged about $80 in commissions. This isn’t competitive in an environment where stocks are traded at $0.

Voyager does not charge commissions on crypto trades and offers 9% interest on stable coins. One thing to note is that Voyager does not offer insurance like Gemini, and that our fund does not hold large amounts of crypto on trading platforms. Instead, we store crypto in cold storage wallets and use trading platforms for trading only. We discuss how Voyager makes money below, the differences in crypto platforms and how investors typically store their crypto below.

The fallout with Robinhood over GameStop has created an influx of customers for Voyager. Total revenue growth between December and February was over 1000% from $1.7 million to $20 million in monthly revenue.

Please note, my readers often ask me about the volatility of crypto and my answer to this is that crypto promises to be some of my most volatile investments. Stocks and crypto prices can drop 60% or more – and this has happened since my official coverage on bitcoin when it was priced at $12,000 and saw $4,000 before finding a base. You can read my past coverage here on Bitcoin in the summer of 2019.

Financial Overview

Although Coinbase was first to market, there is plenty of room for competitors to disrupt the company’s non-existent customer service and excessive commissions. For those who don’t trade crypto, you might be surprised to know that after paying such high fees, you are given no customer service whatsoever. The I/O Fund prefers Gemini as a commission-based platform as there is insurance offered to offset the cost of commissions.

Voyager is FDIC-insured. However, the crypto held with Voyager is not insured. Gemini, which operates as a trust, has private insurance. Like us, crypto investors generally store their assets on a cold storage crypto wallet, which means it is not connected to the internet. In the event there is no insurance, the risk to cold storage wallets is minimal.

Significant Growth from Robinhood Tailwinds

Crypto investors are a tightknit community and we think word-of-mouth will grow nicely in this niche as it actively looks for new platforms. In December, the company reported $1.7 million in revenue and has grown to $8.5 million in January of 2021.

The company reported $2.5 million in revenue from Feb. 1 to Feb. 4—which we predicted could lead to $17 million in revenue in February. The company exceeded this and reported $20 million in revenue for February.

Assets under management (AUM) grew from $230 million in December to $800 million by early February. Total assets under management by the end of February was $1.7 billion.

Trades per day averaged more than 30,000 for the month ending Jan. 31, up from approximately 6,500 in Dec. of 2020, representing 450% growth in daily trade volume. By early February, daily trades averaged 60,000 trades per day or nearly 1000% growth. In the March earnings report, the company reported a total of 70,000 trades in February.

In January, the value of customer trades increased over 500% to $840 million, up from $150 million in December of 2020. Over twelve months, the overall number of trades increased from 8,500 trades in December of 2019 to 1 million trades in January of 2021, an increase of 117,000%. This number may be irrelevant as most of this is priced in right now, yet we think it's important to look at the ongoing strength before the Robinhood issues.

Basic users grew from 150,000 in December to 440,000 by early February. The company reported 605,000 verified users at the end of February.

Here is the full statement from Steve Ehrlich, cofounder and CEO of Voyager, regarding the Robinhood catalyst and what investors can expect moving forward:

"While we believe our recent business metrics reflect the growing interest in the cryptocurrency ecosystem and long-term benefits of our business model, the unprecedented external events over the past week, including decisions made by competitive products, have brought significant upside to our metrics.

While we don't expect a repeat of the unprecedented external events of the past few weeks that have catalyzed the recent growth, we anticipate continued meaningful growth in our business, including from the pipeline of approximately 80,000 customers who have signed up and that we are presently onboarding.

We remain focused on executing our long-term business plan and expect Voyager will continue to grow the business in a more traditional pattern throughout the balance of 2021. To support this growth, we anticipate increased expenditures to materially increase our employee headcount during this period, while also growing our technology architecture stack in the near-term to accommodate significantly more users."

The company closed a private placement of $46 million on January 21st, 2021.

Voyager has seen 75%+ sequential quarter growth with increasing operating margins in 2020. Per the Investors Presentation, Voyager had a previous goal of reaching $20 billion AUM based on $500 million AUM as of Q1 2021 (this was achieved at nearly 3X the company’s original goal with currently $1.7 billion AUM). The company believes it can achieve 90% CAGR on number of funded accounts and 35% CAGR on average account size.

The company also states it takes $35 to acquire an account, and the company makes $30 per account in monthly revenue—which is excellent unit economics. Customer acquisition costs have averaged from $20 to low $30s per new account, according to Stifel Research.

In contrast, monthly revenue per account has accelerated from $40 per month at the calendar end of 2020 to $80 per month in C2021. A catalog of research reports are available from various funds and analysts covering the company, which is fairly extensive coverage considering the company's small market cap.

Voyager is a strong choice for alternative coins, as the app allows you to trade many tokens that Coinbase or Kraken does not support. For example, Voyager offers Dogecoin, a meme coin pushed by Elon Musk. It also offers interest on Bitcoin, Ethereum, Polkadot, and Chainlink.

Voyager sees its diversification across revenue streams as a way to minimize volatility. The revenue streams include listing fees, interest revenue, alternative coins and major coins.

Quarterly Financials

Voyager reported Fiscal Q2 2021 results March 1 for the period ending Dec. 31. The company had $3.56 million in revenue with $2.06 million in fees and interest income of $1.51 million. There was a net and comprehensive loss of $9 million.

Voyager expects to continue bringing new products to The Voyager platform, according to the report. In 2021 and beyond, executives anticipate adding debit cards, credit cards, stock trading, and the ability to trade on margin. Voyager will also look to grow internationally by expanding into Canada and Europe.

Fiscal Q1 2021 results were reported on November 30th for the period ending September 30th. The company had $2 million with $1.6 million in fees and interest income of $400,000. There was a net and comprehensive loss of $3.97 million or ($0.04) EPS.

The company had cash and cash equivalents of $7.48 million and debt of $1.12 million at the last earnings report, which includes a PPP loan. There was an update for fiscal Q2 2021 on January 5th with quarterly revenue expected to reach $3.5 million.