There is a level of speculation to SPAC investing as the majority of these companies have little or no revenue. There is an obvious risk to speculating on young companies, which is that they will not be able to meet their future projections. This is precisely why we choose to allocate a small portion of our portfolio to SPACs, typically not more than 1-2% of our total portfolio in any one company. We are comfortable adding more to these positions as they grow and as the company begins to successfully execute on its goals. Until that point, it is important to recognize that we are making speculative investments and the stocks may be extremely volatile. Keep this in mind when sizing your own positions.

When evaluating SPACs, we prefer companies with the most upside potential in big, fast growing markets. Below are the companies we think have potential and fit our investment profile.

Lucid Motors (CCIV)

CCIV has fallen sharply since its merger confirmation with Lucid Motors and we took that opportunity to open a position. This is a company with enormous potential in the coming years. As of 2020, only 3% of global car sales were electric vehicles. The EV market is set up for exponential growth this decade and beyond as the world focuses on reducing carbon emissions.

I discussed why Lucid’s technology is a legitimate competitor to Tesla here. In Lucid’s Investor Deck, they are projecting 4% market share of the market by 2030. That number would put them as 8th on the current list of auto manufacturers. Lucid has been incorrectly characterized by some as a “Tesla Killer” or a company that must outperform Tesla to succeed. That could not be further from the truth as management is not predicting this nor modeling this.

Lucid has over 7,000 pre-orders for the Lucid Air Dream that is set to debut in the second half of 2021. The company has a working manufacturing facility in Arizona that can currently produce up to 34k units per year. The company is looking to scale that number to 365,000 annual units per year. They are currently working on building a manufacturing facility in China.

The Lucid Air Dream has been independently verified for each of its capabilities. Lucid has over 20M real-world vehicle miles driven. All OEM racing teams in the world’s premier EV racing series are powered by Lucid battery packs and software. In its investor presentation, Lucid talked about its plan to expand its technology supplier business beyond the EV racing series with potential applications in aircraft, eVTOL, military, heavy machinery, agriculture, and marine. Lucid has confirmed that 6 other car companies have contacted them about using their battery technology already.

The Lucid Air has 32 sensors including LIDAR to support Level 2 hands-free highway driving. The company’s goal is to reach Level 3 hands off and eyes-off capabilities within 3 years, which no automaker currently offers. Eugene Lee, the senior director of ADAS and autonomous driving at Lucid Motors, formerly worked on GM’s Super Cruise.

Lucid now has $4.5B in cash on its balance sheet, a number that Tesla did not accumulate until 2019. Tesla had $106M of cash on it balance sheet when it first IPOed. Fisker, another EV company that has not yet delivered any cars, has $400M of cash on its balance sheet. Lucid is also backed by Saudi Arabia’s Public Investment Fund, the country’s premier investing institution. With a strong balance sheet and heavy backers with lots of cash, Lucid is well positioned to overcome the challenges involved with mass producing cars.

Lucid management contains 8 former Tesla executives and 3 former Apple executives. Peter Rawlinson, Lucid’s CEO, was the former Chief Engineer of Tesla and helped design the original Tesla Model S. Rawlinson believes he’s taken it to a new level with the Lucid Air, beyond what he engineered with the Tesla Model S.

Lucid is projected to reach nearly $23B in revenue in 2026. If the company can reach this mark, it could reasonably trade at least 4x above its current ~$48B valuation.

Source: Lucid Investor Presentation

There are obvious hurdles for Lucid and risks involved with this investment. However, we are comfortable speculating on Lucid because of its world class technology, accomplished management team, outstanding balance sheet, and large backers.

Stem Energy (STPK)

I covered STPK in detail here. Stem has proven to be a volatile SPAC for us, but we remain bullish on the company’s long-term prospects. Stem currently has $200M of contracted backlog and over 100% of 2021 revenue locked in from contracts that have already been completed. There is potential for a big upside surprise on the $147M revenue target this year as the actual number should be closer to $200M. The company is projecting revenue to grow at an 81% CAGR through 2026.

Source: Stem Investor Presentation

Partnerships with Apple, Amazon, Google, Facebook, and Walmart represent a backlog of future business that will drive growth for years to come. Stem’s value is in reducing its client’s electric bills 10-30% without changing the way they operate. Stem’s product also helps its clients meet their corporate ESG targets, making them eligible for potential government subsidies.

Electricity production is the #2 polluter responsible for 27% of greenhouse gas emissions. Over 75 countries including the US have committed to net zero emissions by 2050. Stem management estimated that there is a projected $1.2T in new revenue opportunities for integrated storage that are expected to be deployed by 2050.

There remains a great deal of untapped potential for energy efficiency improvement through implementation of new technologies. Stem is ideally positioned to be an industry leader in the energy storage market as more companies follow the path that Apple and Amazon have already taken.

STPK also stands to benefit from increased investments in the ESG space. Money managers are facing greater pressure from investors, regulators, and activists to direct capital toward businesses that support a greener future. Assets that adhere to environmental, social, and governance criteria are projected to exceed $53T by 2025.

Proterra (ACTC)

I first covered Proterra here. Proterra continues to prove why they are the leading electric transit bus manufacturer in North America. This week, Proterra won a 16 year, $169M contract to lease 326 buses in Maryland’s Montgomery County. This contract is the largest municipal government deal of any kind for buses. The Washington DC suburb ultimately plans to replace its entire 1,422-bus fleet over the next two decades using Proterra’s electric battery technology.

It is only a matter of time until other municipalities and cities make the switch to electric transit buses. Proterra management estimates that its total addressable market in this industry exceeds $260B. Currently, the company has a market cap of under $5B despite being positioned as North America’s #1 electric transit bus OEM. Their buses have traveled 16M total miles, significantly leading all competitors. Proterra also has partnerships in place with BMW, Daimler, Con Edison, and most recently Komatsu to develop all electric construction equipment.

Proterra is projecting revenue to grow from $193M at the end of 2020 to $2.56B by the end of 2025.

Source: Proterra Investor Presentation

Eventually, every form of transportation will need to be electrified. Proterra has a commanding lead in North America’s electric transit bus industry and the inside track on future contracts. Jennifer Granholm, the United States Secretary of Energy, formerly held $1M in Proterra stock options and sat on the company’s board prior to being forced to shed any potentially conflicting investments.

Battery-electricity technology is the future of bus transportation. We are in the very beginning of a transition to zero-emission electric buses across the country. Proterra is the industry leader and proved it by winning the nation’s largest municipal government deal for buses. They are ideally positioned to win more contracts in the future as more cities transition to electric bus transportation.

With many popular stay-at-home stocks pulling back on heavy volume and Bitcoin testing $50,000, investors are wondering what’s in store for the world’s most popular cryptocurrency. While some traders have been—and still are—calling for a crash in Bitcoin, we see no reason to sell out just yet.

View webinar here:

Is This the Top?

After reaching a new all-time high of $58,300 over the weekend, Bitcoin is currently trading just under $49,000.

The downward move came on the heels of a warning by U.S. Treasury Secretary Janet Yellen that Bitcoin is an “extremely inefficient” way to conduct monetary transactions, and a tweet by Tesla CEO Elon Musk that the price seems high.

Bitcoin is still up more than 80% this year, and we’re long since $7,753 for a more than 580% gain in our I/O Fund, which is invested in the most important tech microtrends.

Currently we are monitoring the $53,000 to $56,000 region for Bitcoin, which the digital coin is trying to clear. This is an area we will likely begin to start taking small gains to reduce the percentage allocation of Bitcoin in our portfolio.

If Bitcoin can clear this level, the next level of interest is $70,000/$80,000, which will be the zone at which we will continue to monitor closey. If Bitcoin can clear this region, the next level up will be $100,000 to $108,000.

We believe that between $53,000 to $56,000, and the $70,000/$80,000 region, Bitcoin should make a local top. When stocks or crypto reach these levels, we re-assess to determine if we will buy more, hold or sell in our fund.

We’re Up 580% in Bitcoin! What’s Next?

Bitcoin is one of our largest holding at just under 8% of our I/O Fund.

In August 2019, when Bitcoin was trading at around $10,000—well below the 2017 high of nearly $20,000—Beth predicted that global unrest would help establish the digital currency as a safe haven for institutional and retail investors, pushing the market value to $1 trillion.

At the time, it was a contrarian call. But Beth’s analysis proved correct when Bitcoin’s total market value surpassed $1 trillion on Feb. 19.

We purchased Bitcoin in mid-March at around $7,750 and sent an alert to our premium subscribers. We alerted premium subscribers for additional entries at around $10,000, $11,000, $12,000, $20,000, and $49,000.

When Bitcoin was breaking out around $7,000 earlier this year, it was insane to predict Bitcoin would reach over $50,000. But that is what the technicals were suggesting at the time and this is what we published for our premium readers.

Is Bitcoin Due for a Pullback?

Remember when analysts and investors called for a top in Bitcoin at around $32,500? Instead of a top, we predicted a relatively mild pullback. We monitored $28,000 for a shallow pullback and $22,000 for a deeper pullback.

Over the long term, we believe there are a lot more gains to be made in Bitcoin.

In the short to intermediate timeframe we are due for a pullback, which we will view as a buying opportunity and alert premium subscribers. Until we see clear divergences at key technical levels, we plan to hold. However, once we start seeing signs of weakness at key levels, we often take gains and notify our subscribers.

Want to learn more about Bitcoin? Download our free e-book. To receive in-depth analysis on popular technology stocks, and alerts for key entries and exits, subscribe at research.beth.technology.free e-book. To receive in-depth analysis on popular technology stocks, and alerts for key entries and exits, subscribe at research.beth.technology.

The electric vehicle trend seems bubble-like because of the valuations compared to traditional carmakers. However, these are growth companies where traditional carmakers are value stocks. Therefore, you'll need to decide if you see EVs as innovative tech that is pressing the envelope or if EVs should be valued like traditional automakers.

I had made a comment in my free newsletter about playing pickle awhile back with a trend. I was referencing Tesla, of course, where we have remained on the sidelines. Tech growth investors should figure out – do you plan to own Tesla or one of its competitors –or do you plan to not participate in the EV market? When there are significant gains in one company and this marks the start of a trend, then not making a decision is making a decision.

Moving forward, we will allocate a portion of our portfolio to "EVs" and this may include any of the companies listed below. This is a real trend that we want to participate in. David is leaning into Lucid Motors, and I am covering China's EV market.

Here is the summary of the analysis below:

• David is keen on Lucid Motors as a long-range EV that rivals Tesla founded by the former Chief

Engineer at Tesla. Although the initial price point is very high the company plans to release lower-priced models in the near future.

• I am interested in the lower price point that Xpeng offers and for its strategy to target the mid-tier and lower premium market. This makes sense to me in light of China's subsidies, especially since Tesla, Lucid, Nio, BMW, Mercedes – and now Apple will compete in the higher price range.

• Nio is appealing for its battery-as-a-service program and ability to compete with Tesla head-on in China as a domestic car company. Battery charging stations are a serious issue in China and Nio stands out for the battery swap described below.

• We also cover Li Auto, which is more family-oriented.

• Please also look for Knox’s coverage of Tesla from a technical analysis standpoint on the forum and any future webinars – especially as Tesla has added Bitcoin onto its balance sheet. We don't have much to add to this story fundamentally as the stock is well covered by other analysts but if Knox sees a breakout, then he may take it.

Part 1: Lucid Motors by David Marlin

Lucid is a disruptive, innovative company and we think there is more than enough hype and buying interest for this momentum to continue far longer than people expect. Knox is monitoring CCIV for an entry as the latest report shows that the merger with Lucid Motors is essentially done and will be formally announced as soon as this week.

A quick note on valuation …

Many investors will look at Lucid Motors, see they have $0 current revenue and dismiss the stock. It's important to know the market is always forward-looking. Money managers, analysts, and professional investors will typically look 1-2 years out when researching a company.

In the current market environment, they seem to be looking 3-5 years out in some cases. Why? The main reason is the Fed’s policy coupled with the low risk-free rate.

Professional money managers know the risk-free rate is the guaranteed return they can achieve by taking zero risk. When buying equities, investors are making a conscious decision that their returns will be worth the extra risk they are taking.

It’s important to note that the 10-yr rate has risen to 1.29% from 0.66% over the past few months putting some short-term pressure on the market. However, 1.29% is still a historically low rate and not yet a cause for concern for investors. If the 10-yr continues to rise, it will become a much bigger concern, but we are not at that point right now.

Lucid Motors Product Overview …

Somewhere over the last 10-15 years, the auto industry became the tech industry. It started with Tesla disrupting the traditional auto manufacturers by developing extensive proprietary technology for electric vehicles. The relentless rally in TSLA stock has sent every auto company in the world scrambling to produce EVs to capture the industry-wide shift. Even Apple has entered the arena with reports that they are actively working on car tech and plan to produce a vehicle in the next 3-6 years.

As in other subsectors within tech, we expect the company that produces the best and most advanced technology to capture the most market share. That is the case right now, as no company has been able to successfully challenge Tesla’s EV lead. The gap in innovation and technology could not be clearer as Tesla is essentially lapping its competition.

Enter Lucid Motors. Lucid’s CEO Peter Rawlinson said in an interview with CNBC last month that he was “disappointed the traditional auto industry hasn’t taken up the baton to compete with Tesla.” He went on to call the industry a “technology race”, which is exactly how we see it.

Lucid plans to deliver the Lucid Air, its first car, this spring from a new factory in Arizona. The first version of the Air — the Dream Edition — will go for $169,000 (see below for future pricing strategy).

CEO Peter Rawlinson was the former Chief Engineer of Tesla when the company first produced the landmark Model S. He told Forbes that in 2012, nobody believed him when he said the Tesla Model S would be lauded as the world’s best electric car. He said that he is receiving similar disbelief and hostility in response to claims that the Lucid Air will be a big breakthrough.

Even before they have delivered a single car, Lucid Motors is the only legitimate competitor to Tesla in the technology race. In his CNBC interview, Peter Rawlinson noted that the most important metric for measuring EVs is efficiency. The Lucid Air can achieve more than 4.6 miles per kWh versus the Tesla Model S record of 4 miles per kWh. Rawlinson has said that Lucid's efficiency is so much better than any other EV that the car uses 17% less energy to go a certain distance than their closest competitor.

The upcoming 2021 Lucid Air EV has a battery capacity of 113.0 kWh and a range as high as 517 miles. In comparison, Tesla’s 2021 Model S Plaid + announced a range as high as 520 miles, but the car will not be available until the end of 2021. The Lucid Air will also be the fastest charging battery-electric car in the world. The car can charge for 20 miles in one minute, or 300 miles in 20 minutes.

Below, we take a look at a more detailed comparison of the Lucid Air Dream Edition versus the Tesla Model S Plaid Plus:

As you can see, Lucid is a very real competitor to Tesla. We did not put a third automaker for comparison because there is not a third automaker that is even close technologically.

So, what about the valuation?

It is difficult to value Lucid right now because there is no revenue and have not delivered any vehicles. According to Forbes, Lucid could generate $900 million in 2021 revenue by making 6,000 Airs. Rawlinson told Forbes that volume could “top 25,000 units in 2022 as versions of Air priced at $77,000 arrive.”

We believe the best way to value Lucid is as a percentage of Tesla. Tesla has a current market cap of $755B, while CCIV’s implied market cap is around $70B. This would value Lucid at 10-11% of Tesla. Tesla should obviously be valued much higher than Lucid because they have proven the ability to scale, mass produce, and have built one of the best brands in the world. The question is, do those factors mean Tesla should be worth ~11x Lucid, a company that appears to be its equal in terms of technological development? We believe Lucid can be valued at 10-25% of Tesla for now, and potentially more in the future when they start successfully delivering vehicles.

In any event, Tesla may very well hit a $1T market cap at some point this year. At that point, Lucid should command a market cap north of $100B. I am expecting both companies to reach these milestones at some point this year.

The Future of the EV Industry

Elon Musk has said many times that his mission for Tesla is not to produce EVs for wealthy individuals, but to drive EV adoption globally and on a grand scale. Tesla has made great strides in making more affordable vehicles but still has a way to go.

Peter Rawlinson shares a similar mission for Lucid, as noted in Forbes: “He plans to use the Air’s 1,080-horsepower propulsion technology to “power cheaper electric vehicles [enabling Lucid to sell] hundreds of thousands of mid-

$40,000 electric cars and help big automakers sell $25,000 mass-market EVs” by 2026.”

Lucid is starting out as a premium, luxury EV that will appeal to wealthy individuals. However, the company plans to produce cheaper cars ultimately and use its technology to help other automakers produce EVs.

We believe the auto industry will consolidate over the next 5-10 years as companies with inferior technology are squeezed out of the market. Similar to the mobile phone industry where Blackberry, Nokia, and others could not keep up technologically, we will likely see a similar scenario play out in the EV market. It would not be surprising to see the global EV market dominated by a few companies that offer the best capabilities.

In the past, automakers like Mercedes and BMW would target a certain area of the market while Honda and Toyota would target another. With Tesla and Lucid planning to ultimately target the mass market, that will no longer be the case. Many legacy automakers targeting niche markets will likely fail because it will become abundantly clear which companies produce the best product. We would not expect consumers to pay a similar price to buy a mobile phone that has 50% the battery life that an iPhone has. The same will be true in the EV industry, as well.

Tesla has been called the Apple of the EV market as the innovative leader in the industry. In Lucid, Tesla has its first real challenger. We believe Lucid is positioned to be one of the few EV companies that dominate the industry along with Tesla. May the best technology win.

Xpeng has dipped about 25% since we first covered the stock. We think now is a good time to expand on EVs and why we are bullish on this company.

As noted in the original Xpeng blog post, please keep in mind the company's lock-up expires on February 23rd with earnings out on March 8th. We’ve kept some dry powder for this position to allocate after the lock-up. We do expect volatility in this category as Tesla has proven is par for the course.

The company released January 2021 results with 6,015 vehicles delivered, a 470% increase year-over-year. The delivery consisted of 3,710 P7s and 2,305 G3s. This compares to 5,700 EVs in December and 8,500 vehicles sold in Q3.

At this rate, Xpeng will grow annual deliveries (and implied revenue) by 266% if you assume 6,000 deliveries a month for FY2021 at 72,000 vehicles compared to FY2020 at 27,050 vehicles. There will be new record months in 2021 and we believe the annual run rate of 72,000 vehicles is low. The estimated deliveries will put revenue at around $2.2 billion for Xpeng in 2021, which puts us at a 14.5 forward P/S. There will be times we see a 10 forward P/S or lower and a 20 forward P/S or higher in this category.

The goal here is for Xpeng to beat 6,000 deliveries a month because this will lead to revised estimates for 2021, which then leads to a higher stock price. That's the number we want to meet or exceed. I won't be too concerned if this isn't met every single month (i.e., we all saw the Tesla ups and downs tied to deliveries) but I also think Xpeng is more than capable of exceeding this number which is why we are invested.

The main catalyst that should help Xpeng meet these numbers is the lidar-equipped XPILOT sedan coming out in 2021. This will be the first electric vehicle equipped with lidar for autonomous driving and is based the Nvidia Xavier Drive system. Notably, Nvidia is releasing a more powerful drive system called Orin which is scheduled for production in 2022.

According to the deputy chief engineer of China Association of Automobile Manufacturers, China’s EV sales might reach 1.8 million units in 2021, up 40% from a year earlier due to economic growth, continuous stimulus policies, and sales promotions from manufacturers.

The company recently added assisted highway autonomous driving through the Xmart OS 2.5.0 on January 26th.

NIO:

The key driver for Nio is that China’s well-off and affluent population has exceeded 500 million.

NIO provided a delivery update on January 3rd with 17,353 vehicles delivered in Q4, representing an increase of 111% year-over-year and exceeded the quarterly guidance.

For FY2020, the company delivered 43,728 vehicles for an increase of 113% year-over-year. Cumulative delivered reached 75,641.

In the month of December, the company delivered 7,007 vehicles compared to the previous record in October of roughly 5,000 vehicles. The company continues to show strength in doubling its numbers.

In Q3 2020, NIO reported revenue growth of 146% year-over-year for $666 million. This represented quarterover-quarter growth of 22%. The company reported 13% gross margins compared to (12%) in the year-ago quarter. Vehicle margins also improved at 15% compared to (6.8%).

As with Tesla, the losses are the more concerning issue with electric vehicle manufacturers. Nio reported an adjusted net loss of $147 million which equates to an adjusted loss of ($0.12) EPS. The company had $3.3 billion in cash and $1.2 billion in debt as of September 30th. On January 19th, the company closed $1.5 billion in Convertible Senior Notes.

Battery Swaps and Battery-as-a-Service (BaaS)

NIO designs its cars around the battery pack with an interchangeable tray for 70-kWh and 100-kWh battery packs. The three models the company offers all use the same battery packs which helps facilitate battery swapping and battery leasing. Although a handful of attempts at battery swaps and battery leasing have failed, NIO is making this strategy work by offering free battery exchanges that are strategically located near their customers. The company is currently swapping over 4,000 batteries a day.

In August, NIO launched Battery-as-a-Service which provides car owners with the choice to either buy the battery or to lease the battery. Leasing the battery will cut down the price of the vehicle by 20% from around $52,000 USD to $42,000 USD. This means you can buy a luxury NIO for less than a BMW, Audi or Mercedes with the battery lease.

The monthly lease costs $140 per month for the 70-kWh battery pack. There is a flexible upgrade offering to the 100 kWh for a longer trip at $230 per month. Keep in mind, the fuel costs nothing so the lease is equal to the cost of gas.

In November, NIO launched the 100-kWh battery pack with 37% higher energy density than the 70-kWh battery. According to the press release, the 100-kWh battery can reach up to 615 kilometers compared to Tesla’s roughly 500 kilometers for its most expensive model.

NIO delivers a faster battery than a charging station. The strategy of battery swaps is popular in China where many residents live in apartment buildings.

As stated, various companies have attempted this before such as Renault. However, NIO connects all of the dots to offer a complete ecosystem supporting the battery swap and leasing programs. NIO also offers performance parity which means the customer does not need to worry about battery degradation as NIO guarantees the EV will perform years later as if its brand new.

NIO has formed a partnership with CATL to handle the battery business. CATL is the supplier that will repair and replace battery packs and also recycle cells. After the life of the battery has been used, they will be repurposed for bikes and scooters.

Valuation and Forward Guidance

The median analyst’s revenue estimate for 2020 is 63% year-over-year to $2.46 billion and for 2021 is 94% growth to $4.77 billion. The median EPS estimate for 2020 is ($0.58) and for 2021 is ($0.33).

Total revenue for Q4 is estimated between $921.8 million and $947.9 million for approximately 120% to 126% growth YoY and 38% to 42% QoQ.

On January 9th, NIO Day was held in Chengdu, China where the first sedan model ET7 was introduced with autonomous driving features and a larger 150 kWh battery pack for a range of 621 miles. Tesla’s Model S has a range of 402 miles and Lucid Motors has the longest range on the market of 517 miles. Nio’s ET7 will start at $69,000 with a 70kWh battery pack or $58,000 with battery-as-a-service (BaaS).

The ET7 is enabled by a sensor system called NIO Aquila and a super computing platform called NIO Adam. NIO Aquila has 33 sensing units and 11 high-res cameras and one long-range lidar laser. NIO Adam features four Nvidia's DRIVE Orin SoCs with over 1,000 TOPS of performance. Per this press release, Nvidia and NIO will work together on future fleets.

Nio has a high forward P/S of 17 although if the growth continues in the 100% range then there will be room in the valuation as the quarterly results come in. We fully expect to see EVs trade at a forward P/S of 10 at times and forward P/S of 20 at times although it’s becoming apparent the market is valuing EVs (and AVs) as tech companies with growth valuations.

EVs will be hard to time which is why we initiated in Xpeng and prefer to layer in. They are hard to time because the growth is phenomenal and the tailwinds are strong yet there is major volatility in this category. We think the information presented above justifies having exposure to this category and to continue layering in.

Analyst views

Nomura has a buy rating on Nio Limited. They like the company’s top-down launch of its EV pipeline – starting with luxury flagship model ES8, followed by more consumer-friendly models and variants.

As a first mover in BaaS, Nio "should benefit from the price advantage over other OEMs." The analyst believes that by "improving swapping time to only three minutes without human-labor, and with plans to add minihotspots (around the size of three parking spaces) covering most parts of the major cities in China, NIO hopes to redefine the whole user experience of owning an EV.”

Citi downgrades Nio to a neutral rating from Buy. It warns of potential competition for ET7 from Tesla Model S facelift. Citi turns cautious on its shipments forecast for Nio and now expects 2021 shipments of 82K vs. 92k prior and sees 2022 shipments of 144K vs. 162K prior.

Li Auto

Li Auto’s lockup expired January 26th.

Li Auto released its delivery update on January 1st with 6,126 Li Ones delivered in December 2020 for an increase of 530%, which is not very relevant given the first delivery started on December 4th of last year. However, the company did grow quarterly revenue by 67% quarter-over-quarter with 14,464 deliveries in Q4.

The first quarterly release as a new company was Q3 with total revenues of $369 million, up from 29% in Q2. Gross profit margins are better with Li Auto than peers Nio and Xpeng at 19.8% when compared to 13.3% in Q2 2020. Adjusted loss from operations was $6.6 million and adjusted net income of $2.4 million. The (thin) profit margin separates Li Auto from its EV peers.

The company has cash of $2.79 billion and debt of $380,000 as of September 30th.

Guidance for Q4 is between $457.8 million and $499.4 million representing an increase of 23.9% to 35.1% from Q3. The median analyst revenue estimate for 2020 is $1.41 billion to $2.94 billion for growth of 109% year-overyear. The median EPS estimate for 2020 is ($0.11) and for 2021 is $0.01.

Li Auto Key Differentiators

Li Auto announced the adoption of NVIDIA’s next generation autonomous smart driving chip Orin. According to the company, Li Auto will be the first OEM equipping its vehicles, the full-size extended smart SUV to be launched in 2022 with the powerful NVIDIA Orin SoC chip.

Li Auto is focused on SUVs priced between $20,000 USD and $70,000 USD.

One of the key differentiators for Li Auto is extended range EV technology (EREV) which allows drivers to charge the battery pack with electricity or gas. Battery EVs (BEV) are the more popular EV in China per Li Auto’s S1 filing with 81.3% of the sales volume in 2019 with Li Auto being the “first successfully commercialized EREV in China.”

In the S-1 Filing, Li Auto points out that Battery EVs face challenges, such as a lack of charging stations and limited residential parking spaces compounds this issue. The ratio of parking to car is 2 to 1 in first-tier cities with less than 25% of families in China having access to a suitable space for home charging compared to 70% in the United States. This causes Chinese EV customers to rely on public charging infrastructure with EV to public charging station ratio of 7.4 to 1.

Li Auto also highlights their early profitability as an advantage over its battery-powered competitors with bill of materials being 40% to 50% higher than ICE vehicles. the cost of lithium-ion batteries has decreased from $855 per kilowatt-hour in 2010 to $166 per kilowatt-hour in 2019 – yet the cost is only expected to decrease to $111 per kilowatt-hour in the next five years. The end result is that Li Auto can be more competitive on pricing compared to EVs while also more profitable. Li Auto also benefits from the 10% extra vehicle purchase tax on ICEs in China.

Li Auto provides this plot graph showing its range and cost is competitive in the SUV segment. Nio also looking good here with Xpeng not pictured.

In my opinion, one drawback is the lack of a sedan. Xpeng is an attractive stock for the P7 (and the growth that followed this release) and Nio for its upcoming sedan. Li Auto makes a case that China is relaxing the one-child rule yet having two children does not necessarily require a SUV. Despite relaxing this rule, the number of births in 2018 was at its lowest rate since 1961.

The sales numbers for sedans illustrated by Xpeng don’t agree with the statistics that the SUV segment is expected to become the largest segment by 2020 as measured by sales volume with a penetration rate at 45.4% now and growing to 49.2% by 2024.

ByteDance has invested $30 million in a Series C round.

Or Telephone:

Dial(for higher quality, dial a number based on your current location):

US: +1 346 248 7799 or +1 669 900 6833 or +1 253 215 8782 or +1 312 626 6799 or +1 929 205 6099 or +1 301 715 8592

Webinar ID: 861 9245 0555

In the excitement about SPACs and the flood of IPOs that have listed recently, it'd be easy to forget about the tried-and-true.

Quick Note on the Current Climate …

My main thesis about cloud has not changed: it's secular and insulated from geopolitical risks and economic drawdowns. Generally speaking, cloud software reduces costs for enterprises and SMBs. Therefore, the category is more insulated from economic drawdowns. You can read more about my views on cloud’s resiliency here.

There's a caveat to this, which is that the market is flooded with cloud software solutions and tools – both in the public markets and private markets. This is because cloud software has a low barrier to entry. The costs to develop cloud software and go-to-market is very low compared to hardware or a solution that requires specialty engineers, like AI, ML, robotics, etcetera. Venture capitalists are drawn to cloud software because it's relatively cheap to create, and the margins are healthy due to recurring subscription revenue.

The window of time that you have to be wary is between years 8 and years 12 for a software company. Prior to year 8, it's common for software and new tech startups to report rapid growth. VCs know this and are taking companies public sooner to capitalize off momentum traders (and trading machines), that indiscriminately pile into companies with high growth rates.

In this case, a VC firm can see a very large exit and move onto another company while the public markets sort out the long-term growth rate and the company's ability to scale. Every startup looks strong at the beginning of the marathon but which ones endure past mile 13? VCs don't have to worry about this as the goal in today's market is to exit before the marathon is half-over.

The ramp-up period for startups is exciting because the product finds early adopters. Can the product sustain long-term after year 8 and continue to take market share? This is a much more complex question. Private investors exit before the long-term viability of a company surfaces and (us) public investors have to extrapolate the longerterm trajectory.

Consider the fact that 9 out of 10 startups fail. If you’re a VC, you’re going to get the startup to the public markets as fast as possible to get your exit. If the company fails or the growth slows down, as it does for most tech startups, then it's of no importance as the exit was made. Because of this dynamic (that startups are essentially experiments) and there are many new SPACs bringing to market roughly 165 unvetted companies, I believe we will see a string of failures at the peril of public investors. According to these statistics, we could see 148 fail out of the 165, or on the low-end, 132 of the 165 fails. The low-end is the 80% failure rate for VC-backed companies indicated by the statistics.

SPACs are not inherently wrong (and David pointed out a few benefits compared to IPOs). However, young companies fail very frequently and the public markets are becoming the exit grounds for pre-revenue companies. This piece is new and public investors aren’t prepared for the high failure rate that is a daily reality in the private markets.

That’s a bit of a tangent to say we will continue to have plenty of exposure to cloud in our portfolio as a hedge against any high-fliers we take. The fact that cloud is out of favor in the market right now is not a concern to us because we know cloud has a resilient growth rate.

We also want to communicate that we are well-diversified. We have exposure to SPACs and small caps, but we use cloud and semis as a safe haven. I think these comments will become more apparent as we move through the year. Basically, I am contrasting why cloud deserves attention right now despite the fact speculative trading in SPACs and Momentum has been in the driver’s seat.

Regarding valuations — I've stressed this point with companies like Snowflake because we will see more of this as time goes on and investors need to be careful of merely providing exits for VCs at sky-high valuations. Being patient is an important tool in a retailer's arsenal when a valuation is high.

Please keep in mind, that we discouraged readers from buying Zoom Video when trading in the forward P/S range of 50 despite owning this stock at a lower cost basis. Therefore, I am not singling out Snowflake but instead using it as an example to illustrate why we have not bought this excellent company as "growth at any price" can lockup your money for a few quarters while the financials catch up to the valuation. This is exactly what has happened with Zoom Video (it took a long breather) although the forward P/S is much more reasonable now.

Our Focus: Product-Market Fit and Valuations

For our portfolio, cloud is a hedge as valuations may fluctuate, but growth will march onward for the companies with product-market fit in this resilient category. The best illustration of product-market fit is Shopify and Zoom Video as both their top and bottom lines prove they are efficiently meeting market demand.

An example of a company that I have picked on for not having product-market fit is Uber and Lyft as they must subsidize rides. The market price that customers will pay is lower than its operational costs. The market may still move the stock based on the promise of autonomous vehicles or robotaxis but today's financials do not suggest there is product-market fit.

Opendoor has a similar issue. The financials are upside down as the more the company makes, the more the company loses, and this is inherent to the current business model (not a one-time event or the cost to scale).

Opendoor was hoping to charge 10% in commissions which is about 4% more than Realtor fees for the convenience of buying the house in cash. The market will not pay this extra 4% and Opendoor is forced to match Realtors at 6% commissions. Like Uber, the price does not cover the operational costs. However, we are in a period of historic liquidity and QE. The market may pile in based off sentiment or other speculative reasons (we’ve entered this stock ourselves and it’s performed well), but the financials today do not show a company that has achieved product-market fit.

You could argue Fubo does not have product-market fit as seen in the financials. The cost of licensing the content does not cover the cost of operations. So, why am I invested? Because this is the yearthe year for CTV ads and OTT live content so we think the trend is so early and so massive that we are comfortable taking a flier on this company. I’ve said before that OTT live sports is the holy grail and cable networks/media conglomerates will do what it takes to own this transition. There are many market forces at play here and Fubo is centered perfectly in the middle. Therefore, this is an investment in the trend of Live Sports OTT.

Product-market fit is important to this discussion because finding the gems will protect us from any downside in the market. Even if the market temporarily sells-off in certain names, we can rest easy if we stick to quality.

The best examples of product-market on the public markets are the FAANGs – where the top line defies the odds, and the bottom line continues to deliver. There are others in the $200B+ market cap range that illustrate this: Salesforce for CRM, Adobe for design and its developer moat, Nvidia for the CUDA platform and its developer moat, etc. Sticking with these companies through market ups and downs did well for early investors.

Cloud investing was fairly predictable in the previous years because there were clear winners in terms of forward growth. Due to tougher comps, nearly half of all cloud stocks guide between 20% and 40% with very few above this range and priced dearly if they are (see the chart below).

The other factor we will be considering as we move into 2021 is valuation. There is a disconnect in a few names where the market has not been perfectly efficient. Below, we pull out a few names that have room and rely on Knox for any breakouts in valuation.

As was posted on the forum last week, those with room in valuation include Bandwidth, Asana and Crowdstrike. We are also pleasantly surprised to see Kingsoft Cloud having quite a bit of room although some of this likely represents the risk in China. In the Macro section, you'll see that China's Cloud IaaS is set to take off with Alibaba surpassing Google Cloud for the number three spot. We think this foreshadowing growth for Kingsoft.

Macro Outlook:

The big takeaway from the cloud market going into 2021 is that hybrid work-from-home is here to stay. The market is pricing cloud productivity software as a temporary COVID tailwind but the analysis shows a permanent shift that will accelerate this year.

According to IDC, the cloud market will grow at a CAGR of 15.7% through 2024 to become a $1 trillion market in 2024. This forecast includes software-as-a-service (SaaS), platform-as-a-service (PaaS), and infrastructure-as-aservice (IaaS).

The research firm also states that by 2021, 90 percent of enterprises will be relying on a mix of onpremise/dedicated private clouds, multiple public clouds and legacy platforms. Therefore, IDC predicts this to be the year of multi-cloud, which we covered in our Microsoft earnings report write-up here. We see multi-cloud as the first step towards edge computing to where servers from various hyperscalers or CDNs work cooperatively to deploy 5G workloads.

On a trailing basis, cloud spending grew from $183 billion in 2018 to $233.4 billion in 2019. This puts the $1 trillion prediction into context as IDC calls for roughly 400% growth over the next five years. In 2019, SaaS accounted for $148 billion, or about 64% of the public cloud market.

SaaS dominating the IT spend for cloud is important because it means there will be many winners in this category as it marches onward to the $1 trillion mark.

According to IDC, more than half of the global revenue in the PaaS and IaaS markets was captured by AWS (33.6%) and Microsoft (18.0%) leaving 34.90% for the rest of the market.

This is not the case with SaaS where the rest of the market captured 73.9% and the top two vendors, Salesforce and Microsoft, caught 7-8%.

This is also important for perspective as smaller companies own the SaaS market while Big Tech dominates IaaS and PaaS. Therefore, there is a solid opportunity for investors in cloud software now and into the future. The graph below helps to visualize the opportunity for smaller players:

According to Gartner, worldwide public cloud spending will grow 18% in 2021 to total $304.9 billion. Relative to overall IT spend, cloud still has a long runway and is projected to make up 14.2% of total global enterprise IT spend in 2024 compared to 9.1% in 2020.

Gartner’s survey indicates that there is still quite a bit of growth ahead despite the harder comps the cloud software leaders face in 2021. The data shows that 70% of organizations using cloud services plan to increase their spending, stating “the proportion of IT spending that is being allocated to cloud will accelerate even further in the aftermath of the COVID-19 crisis.”

The analyst firm points towards mobility, remote working and hybrid workforces as trends that will lead to further market growth.

In the graph above, we see survey respondents and Gartner forecast an increase in work-from-home. Meanwhile, the market has been cautious about cloud software post-vaccine, which may be unwarranted with hybrid workforces.

Here is what Gartner states, “For example, customers and citizens shifted their activity online during the lockdown, but that shift will increase, not reverse, in 2021.”

Forrester’s recent survey showed similar results with 47% of North American managers anticipating a permanently higher rate of full-time remote employees and 53% of employees wanting to work from home postpandemic.

Although budgets will only increase 2% in 2021, according to Gartner, CIOs' top priorities are digital workplace technologies to support work-from-home, and then AI/ML, robotic process automation (RPA), distributed cloud and multi-experience platforms.

Forrester states 35% of companies will double down on workplace AI with one in four workers supported by automation either directly or indirectly by the end of 2021. B2B sellers will rely on AI and automation with predictions that 60% will rely on tools with these functionalities embedded.

The analyst firm also states the hyperscale cloud market will “return to hypergrowth” of 35% to $120 billion in 2021. This is up from the original prediction that cloud IaaS would grow 28%. The analyst firm also predicts Alibaba will take the number three spot instead of Google Cloud.

Adopting serverless apps and containers will continue to grow with increased demand for multi-cloud container development platforms and public-cloud container/serverless services. Forrester also believes a leading trend will be disaster recovery moving to the public cloud.

Cloud Stocks for H1 2021

I wrote my first thematic PDF on cloud in December of 2019 during an intense cloud sell-off. The First Trust Cloud Computing ETF (SKYY) had posted 22% returns YTD at time of writing in December and closed the year with 24.55% returns for full-year 2019.

Last year, cloud performed much better due to its fundamental, secular strength during COVID with the SKYY ETF closing out with 57.41% returns in 2020.

We covered many cloud names at their lows during Q3 and Q4 2019 due to our thesis that cloud is insulated and secular. At the time, we pointed out that cloud services were expected to grow 4.5 times more than the IT industry and that future growth through 2022 would be 3 times higher than IT (page 3 from this report).

I believe we are here again in a very similar spot. The market thinks cloud is going to be stunted and forward guidance isn't saying otherwise. However, the analyst firms are predicting we will accelerate and are raising forecasts. We will side with Gartner, IDC and Forrester who do a particularly great job in the cloud category.

Prior to COVID, our thesis was this: “cloud software is more sheltered from overseas economies, supply chains, trade wars and shifting government policies” and “truly, there is few safer places to invest in technology if the trade war resumes or we see the recession that many economists are predicting.”

My thesis this year is that work-from-home and hybrid work environments will be the new norm which will keep cloud growth steady and that AI and ML will be another catalyst. You simply can’t compete with AI and ML with on-premise servers and software. Edge computing and 5G is another accelerant for cloud IaaS, PaaS and software.

Below are the top 35 cloud stocks listed by revenue growth that we consider to be in our universe. The top 10 are shaded in yellow.

In a Motley Fool podcast, I had said that this would revert to about a 30 forward P/S and we are here now.

Some Conclusions:

• Kingsoft Cloud has a compelling risk/reward ratio as the company will deliver Snowflake-level revenue at rock-bottom valuation.

• Bandwidth has the ingredients to pass the pack of cloud stocks stuck in the sub-40% growth range. Let’s see if the company can do this – and if the valuation will finally match its potential.

• Asana is not in our top 10 due to competition across productivity tools, but we see room here in the valuation. This will be something Knox spearheads as he sees the right setup including this one from last week.

• Crowdstrike and Zscaler are both leaders in revenue growth and EPS growth.

• Zoom Video and Shopify are both strongest in terms of a large base in EPS and we think the products will perform well in the face of tough comps this year.

• This year is very unique for cloud software because so many stocks are sub-40% growth and tightly ranked (see the chart above). We are not surprised to see mixed-reactions to the earnings reports as the market is holding its breath to see what the covid comps will be for the March quarter.

• We are not too concerned about the market taking a breather or responding to uncertainty. There is only one way forward for SMBs and enterprises (which is adopting cloud IaaS, platforms and software).

Traditional IT is expensive and will only hinder a company from taking advantage of AI and 5G. Competitively it can be very harmful to not transition to cloud right now as we've seen in my past reports citing McKinsey.

• The last time I talked about cloud on the Motley Fool podcast, I thought valuation was a serious risk as we saw many names trading in the 50 forward P/S range whereas 30 forward P/S is the mean for highgrowers and 20 P/S is the mean for average growers.

• Now that we have reverted to the mean, we plan to allocate for cloud while the trend is out of favor.

My Top 10:

We stand by Zoom Video and Shopify as the relationship between the top-line and the bottom-line proves product-market fit. We understand there will be harder comps this year but these companies are releasing new products to grow market share and continue to be centered in important trends. These were strong companies prior to COVID and we thnk they will be strong companies post-COVID.

Crowdstrike and Zscaler are stocks that David follows closely and are the best positioned cybersecurity companies to benefit from the growing security spending cycle. The Covid-19 pandemic and the Sunburst hack uncovered a number of major gaps, highlighting the need for organizations to transform their legacy security architectures. Credit Suisse’s recent CIO survey suggests that security spending is the top spending priority in 2021, even more so than in July.

Kingsoft Cloud and Bandwidth are both undervalued in terms of forward-growth. China's cloud IaaS should be in the breakout year as Alibaba takes over Google Cloud as number three. Bandwidth is centered in the hardwareas-a-service trend, which may not be as exciting as EVs or SPACs but is essential to the digital transformation we've seen this past year and a hybrid work environment.

We could not be more bullish on Twilio’s long-term trajectory. The company has a moat in cloud communications for native apps and the management is taking on the omni-channel marketing to increase the addressable market. Should the management pull this off (and we think they will), then Twilio is setting up to be a leader in marketing and sales data with Adobe/Salesforce long-term potential.

Datadog has auspicious positioning for hybrid cloud and multi-cloud. The three analyst firms agree that the public cloud is going to accelerate this year and we want exposure. The market taking a breather does not affect our conviction and we think DDOG is the best way to participate in the growth of Azure, AWS and Google Cloud plus the trend towards multi-cloud (which also directly relates to edge computing).

Teladoc’s low forward P/S (comparatively) is a mystery as this is a mega-trend that will be unstoppable as artificial intelligence continues to merge with health care. We can't think of an industry more ripe for disruption as health care costs have risen 400% in the last decade while wages have stagnated. AI and genomics are able to cure terminal diseases, although TDOC is centered in the first problem (health care costs).

DocuSign is a steady performer with solid top-line and solid bottom-line growth. The market tends to overlook this one, but we like DocuSign as the primary choice for legal, real estate and financial industries. There is very little room for competitors as DocuSign delivers a superior product that can become the universal standard. We do not think the world will reverse to paper.

We continue to want exposure to telehealth and so have allocated to Amwell as an 11th position in cloud.

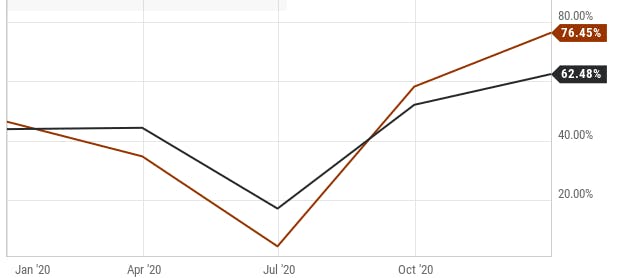

2020 earnings from ad-tech stocks have shown us that digital advertising has rebounded sharply from the pandemic recession lows. Pinterest’s growth rate dropped to 4% YoY in Q2 but has since rebounded to +77% in Q4. SNAP’s growth rate bottomed at 17% in Q2 and has recovered to +62% in Q4.

In total, global digital advertising spend grew less than 5% in 2020 but is expected to accelerate with 17% YoY growth in 2021 as we head into a higher GDP environment.

Global digital ad spend now makes up 52% of all ad spend, the first year it has eclipsed over 50% share. Over the next 4 years, global digital ad spend is expected to grow 61% from its current total and will exceed 60% of all advertising dollars. The industry growth we are expecting to see will provide a powerful tailwind for digital ad stocks. Pinterest and Snap have proven to be two of the industry’s leaders, with both companies announcing record results in Q4.

Pinterest

Pinterest reported Q4 results on February 5th, beating estimates on both the top and bottom lines. Revenue of $706M (+77% YoY) came in 9% above the consensus projection of $647M. Adjusted EPS of $0.43 exceeded the street estimate of $0.33 while adjusted EBITDA of $299M far outpaced estimates calling for $226M.

The company announced that Global Monthly Active Users (MAUs) grew 37% YoY to 459M vs. 450M consensus, US MAUs were 98mm vs. 97M consensus, and International MAUs were 361M vs 360M consensus.

Management also indicated that it is expecting revenue to grow in the low 70% range YoY for the March quarter.

In its Q4 earnings call, Pinterest CFO, Todd Morgenfeld, attributed the strong Q4 to the investments the company has made in technology and the expansion of their sales coverage:

“Over the last year, we’ve invested in our ability to better deliver returns [through] accountable performance advertising, including scaling, conversion optimization, ads, shopping, ads, and building improved automation to help advertisers of all sizes more easily onboard and realize the value of being on Pinterest…We also expanded our sales team in Western Europe to monetize our engagement there.” One of the standouts from the company’s Q4 results is the international growth they saw. Pinterest grew international revenue 146% YoY, international MAUs 79% YoY, and international ARPU 67% YoY. All three metrics represent record results for Pinterest.

On the technology front, Pinterest has created value for advertisers through the onboarding of catalogs and automation tools to make spending on the platform easier. The investments Pinterest has made in improving their technology to deliver more value to advertisers paid off with record numbers in Q4.

Management’s commentary and guidance indicate that they expect this momentum to continue in Q1: “we expect positive trends from our investments in ad tools like shopping and automation, and sales coverage expansion to continue. We plan to expand our international coverage further in existing geographies, and also expand monetization into Latin America in the first half of the year.”

Recently, Microsoft attempted to buy Pinterest according to news sources. At $51 billion, Pinterest is twice the valuation of LinkedIN at the time of acquisition. Last year, Microsoft put in a bid for Tiktok.

Snap

Snap announced Q4 results on February 5th, topping consensus estimates on both the top and bottom lines although guidance for next quarter came in under expectations on adjusted EBITDA.

In Q4, revenue grew 62% YoY to $911M, topping Wall Street’s estimate of $855M by 7%.

Adjusted EPS of $0.09 beat by $0.02 while adjusted EBITDA of $166M comfortably exceeded expectations calling for $142M.

Global daily active users (DAUs) rose 22% YoY to 265M, surpassing expectations for 258M. Daily active users exceeded expectations across all geographies, including North America, Europe and ROWS.

For Q1, Snap sees revenue of $730M at the midpoint and adjusted EBITDA of -$60M. The adjusted EBITDA guidance came as a surprise as analysts were expecting positive EBITDA for Q1. Still, -$60M would be an improvement over -$81M in Q1 2020.

In its Q4 earnings call, Snap CFO Jeremi Gorman discussed the rebound the company observed after Q2: “in Q3 and Q4, we saw many existing advertisers return to Snap and so many new ones leverage our innovative ad formats and bidding capabilities to drive real business value on our platform. This drove active advertisers to an all-time high.”

Snap currently has an average of 200 million people engaging with AR on Snapchat every day. The company noted that they will continue to invest heavily in AR to create new cutting-edge tools and capabilities that allow advertisers to reach their audience in new ways.

Snap believes there is tremendous value in giving advertisers the ability to engage with their audience directly via the camera. Management disclosed that businesses leveraging AR as one component of a larger multi-product campaign on Snapchat tend to achieve stronger results.

Another key area for investment moving forward for Snap is video advertising and the growth of Spotlight: “We see more opportunity over time to grow video inventory particularly via the growth in viewership of Spotlight and Stories.” This is the primary way Snap monetizes its users, but the company believes there will be even more opportunity here in the future.

Snap has invested in content to support the launch of spotlight and plans to continue to make this a focus area moving forward. These investment areas are the main reason for Snap’s adjusted EBITDA target coming in below consensus.

Snap management tempered expectations for 2021 when discussing how the iOS platform policy changes could affect their business: “We anticipate that the iOS platform policy changes to be implemented later this quarter will present another risk of interruption to demand in the period immediately after they are implemented. It is not clear yet what the longer-term impact of those changes may be for the top-line momentum of our business, and this may not be clear until several months or more after the changes are implemented.”

Snap showed tremendous growth in Q4 and continues to be a key tool for advertisers that are trying to reach a younger audience. On average, DAUs opened the app 30 times a day in the fourth quarter with an average of over 5 billion snaps created each day. CEO Evan Spiegel indicated that he expects Snap to accelerate its full year growth rate in 2021 to above the 46% number the company recorded in 2020.

Cloudflare

Cloudflare (NET) announced Q4 earnings results on February 11th. Adjusted EPS of ($0.02) beat consensus estimates by $0.02 while adjusted operating margin of (7.9%) improved 1.7% on a YoY basis. Revenue of $126M grew 50% YoY, topping consensus expectations by $7.6M.

Gross margin declined slightly on a YoY basis to 77.6% from 78.2% a year ago. Management attributed this decline to the fact that they did not raise prices because they did not want their customers to end up with a surprise bill during the pandemic. FCF was negative $23.5M, representing a FCF margin of (18.7%).

For Q1, Cloudflare sees $130.5M in revenue at the midpoint, coming in above the $126.2M consensus. Loss per share is expected between $0.02-0.03 vs. the $0.03 loss estimate. Full year 2021 guidance also topped analyst estimates with management expecting revenue of $591M versus a $561M consensus. On the bottom line, Cloudflare is expecting a loss per share of $0.08-0.09 for the FY21 versus the $0.09 loss estimate.

Q4 was a strong quarter for Cloudflare despite the initial 6% decline in the stock on Friday following the announcement of these results. NET shares were up 20% YTD coming into the earnings report, creating a potential profit-taking scenario following Q4 results.

CEO Matthew Prince highlighted the company’s growth in paying customers accounts and large customer accounts in Cloudflare’s Q4 earnings call: “Our paying customer accounts grew to over 111,000, up 10% quarter-over-quarter and our strongest quarterly growth in several years.

Large customers, those that spend over a hundred thousand dollars per year with us, continue to be our strongest growth area adding 92 new customers in Q4 and bringing our total large customer account to 828. Revenue from these large customers increased sequentially to 49%, up from 47% in Q3 as our sales team continues to close larger and larger enterprise accounts.”

Cloudflare announced that their Dollar-based net retention of 119% improved 3% sequentially, driven by continued strength from large enterprise customers. Management attributes the growth in large enterprise customers to the company’s expanded product portfolio.

The company has launched a number of products and features that are important to customers, including its zero-trust network security solution, Cloudflare 1, and Magic Transit. CEO Matthew Prince believes Cloudflare’s zero trust solution is the best in the industry, noting that Cloudflare “is the only company with a zero-trust solution that really understands and is built for the needs of developers”. Cloudflare’s mission is to provide value for developers in a way that other companies do not.

Cloudflare management highlighted a few significant customers wins in Q4. They attributed these customer wins to the platform’s ease of use, technical innovation, and the way multiple products fit together into a unified solution. CEO Matthew Prince believes his company is on the path to more significant customer wins in the future: “Developers are the future of IT and having won their trust we expect will help us win, retain and expand more and more customers over time.”

Looking ahead, Cloudflare management believes the strong business momentum they observed in Q4 will continue into Q1 and throughout 2021. The company raised its outlook on both these numbers. Management noted that in 2020 companies were simply trying to survive.

In 2021, management believes there will be a big shift from a traditional hardware-based security approach to a much more modern zero trust approach. The company is confident that Cloudflare will be one of the leaders in enabling companies to make that transition.

Voyager Digital is a high-risk/high-reward opportunity that offers exposure to the Bitcoin and crypto trading trend. The company is part of a consortium for stable coins, including USD Coin (USDC) and Tether’s USDT, which in total have surpassed $7 billion in circulation.

In other words, Voyager provides exposure to both decentralized coins (Bitcoin, Ethereum, Litecoin, Chainlink, etc.) and coins based on the fiat system.

Big Tech and the Fed will push for stable coins based on the fiat system, while crypto enthusiasts and developers will want blockchain to remain decentralized. Although I am personally in the decentralized camp (you can read my Facebook Libra article here), I am also aware that the powers-to-be are likely to put immense pressure on adopting stable coins. This company allows exposure to both at a $2.15 billion market cap.

Voyager Digital strives to offer more coins than its competitors, including the $30 billion market cap Coinbase that is going public soon, Kraken and Gemini.

Voyager does not charge commissions on crypto trades and offers 9% interest on stable coins. We break down how this is possible below.

Please note, the I/O fund does not hold large amounts of crypto on trading platforms. Instead, we do this in wallets and use trading platforms for trading only. We explain the nuances of why and various choices if you do want to hold coins in “hot storage.”

Below, we offer a thorough analysis of how Voyager stacks up against Coinbase and Gemini. Crypto-related stocks and assets are more volatile than others – although less so over the recent year.

We think it's essential to go through this company thoroughly and how it stacks up to its competitors as anything crypto-related promises to be volatile — although less so over the recent year.

Financial Overview

We published a quick blog on Voyager two days before the company released a substantial report on its recent growth, which can be found here.

Voyager is on a growth streak fueled by the Robinhood issues and a rise in brand awareness from offering the meme-token Dogecoin. The company solves one of the more significant pain points for crypto investors, which is commissions. To illustrate, a $5000 crypto trade on Coinbase can cost as much as $80 ranging from 4% to 1.5% commissions. These are not small stock trading fees of $4.99. Although Coinbase was first to market, there is plenty of room for competitors to disrupt the non-existent customer service and excessive commissions. We discuss Gemini below as a better alternative to Coinbase if you do choose a commission-based platform.

Voyager is FDIC-insured. However, the crypto held with Voyager is not insured. Gemini, which operates as a trust, has private insurance. For the most part, crypto investors (including ourselves) store their assets on a "cold storage" crypto wallet.

The risk is minimal in this case in the event there is no insurance.

Significant Growth from Robinhood Tailwinds

Voyager reported roughly 400-500% growth from December to January and roughly 1000% growth from December to early February from the most recent report released in early February. Crypto is a tight-knit niche and we think word-of-mouth will grow nicely in this community as it actively looks for new platforms.

In December, the company reported $1.7 million in revenue and has grown to $8.5 million in January of 2021, for roughly 600%. The company reported $2.5 million in revenue between February 1st and February 4th — which could lead to $17 million in revenue in February.

Trades per day averaged more than 30,000 for the month ending January 31st, up from approximately 6,500 in December of 2020, representing 450% growth in daily trade volume. By early February, daily trades averaged 60,000 trades per day or nearly 1000% growth.

In January, the value of customer trades increased over 500% to $840 million, up from $150 million in December of 2020.

Over twelve months, the overall number of trades increased from 8,500 trades in December of 2019 to 1 million trades in January of 2021, an increase of 117,000%. This number may be irrelevant as most of this is priced in, yet we think it's important to look at the ongoing strength before the Robinhood issues.

Basic users grew from 150,000 in December to 440,000 by early February. The company has a pipeline of 80,000 customers the company is trying to onboard.

Here is the management’s statement in full regarding the Robinhood catalyst and what investors can expect moving forward:

"While we believe our recent business metrics reflect the growing interest in the cryptocurrency ecosystem and long-term benefits of our business model, the unprecedented external events over the past week, including decisions made by competitive products, have brought significant upside to our metrics," said Steve Ehrlich, Cofounder and CEO of Voyager. the unprecedented external events over the past week, including decisions made by competitive products, have brought significant upside to our metrics," said Steve Ehrlich, Cofounder and CEO of Voyager.

"While we don't expect a repeat of the unprecedented external events of the past few weeks that have catalyzed the recent growth, we anticipate continued meaningful growth in our business, including from the pipeline of approximately 80,000 customers who have signed up and that we are presently onboarding. While we don't expect a repeat of the unprecedented external events of the past few weeks that have catalyzed the recent growth, we anticipate continued meaningful growth in our business, including from the pipeline of approximately 80,000 customers who have signed up and that we are presently onboarding.

We remain focused on executing our long-term business plan and expect Voyager will continue to grow the business in a more traditional pattern throughout the balance of 2021. To support this growth, we anticipate increased expenditures to materially increase our employee headcount during this period, while also growing our technology architecture stack in the near-term to accommodate significantly more users." expect Voyager will continue to grow the business in a more traditional pattern throughout the balance of 2021. To support this growth, we anticipate increased expenditures to materially increase our employee headcount during this period, while also growing our technology architecture stack in the near-term to accommodate significantly more users."

The company closed a private placement of $46 million on January 21st, 2021.

Per the Investors Presentation, Voyager has an ambitious goal of reaching $20 billion AUM based on $500 million AUM as of Q1 2021 (this was achieved and more so with currently $800 million AUM).

The presentation also points out that Voyager has seen 75%+ sequential quarter growth with increasing operating margins in 2020. The company also states it takes $35 to acquire an account, and the company makes $30 per account in monthly revenue – which is excellent unit economics.

According to Stifel Research, the customer acquisition cost has averaged $20 to low $30s per new account. In contrast, monthly revenue per account has accelerated to $80/month in C2021 from $40/month at the calendarend of 2020.

You can read a catalog of research reports from various funds and analysts covering the company, which might help see the fairly extensive coverage considering the company's small market cap.

Voyager is a strong choice for alternative coins as the app allows you to trade many tokens that Coinbase or Kraken does not support. Dogecoin, for instance, which is a meme coin pushed by Elon Musk is offered on Voyager. The company offers interest on Bitcoin, Ethereum, Polkadot and Chainlink.

Quarterly Financials

Fiscal Q1 2021 results were reported on November 30th for the period ending September 30th. The company had

$2 million with $1.6 million in fees and interest income of $400,000. There was a net and comprehensive loss of $3.97 million or ($0.04) EPS.

The company had cash and cash equivalents of $7.48 million and debt of $1.12 million at the last earnings report, which includes a PPP loan.

There was an update for fiscal Q2 2021 on January 5th with quarterly revenue expected to reach $3.5 million.

Voyager also completed a private placement during the quarter, which increases gross proceeds raised during fiscal 2021 to C$13.8 million. It completed the acquisition of LGO, SAS, an AMF regulated entity that provides Voyager with a fully licensed European entity to accelerate its European strategy.

How does Voyager Make Money?

Voyager’s revenue is not dependent on commissions or fees. The company plans to introduce a debit card, credit card, margin, loans, and advisory products over the next year or so.

Right now, the business model creates revenue in two specific ways:

1) Smart Order Routing: When you place an order to buy or sell a cryptocurrency, they will provide a listed price at which you accept. They will then connect your order to 12 exchanges. Unlike securities, which by law, must have the same price across all domestic exchanges, cryptocurrencies are priced at variable levels. In other words, the same coin can be listed at two different prices at the exact same time.

Voyager uses your order to capitalize on this inefficiency by performing an arbitrage across various exchanges. The profits from such a move would typically surpass any commission or fee, allowing them to provide exceptional pricing. Voyager will thus share the profits from this arbitrage with you in an attempt to execute your order at a lower price than you agreed to.

This specific business model will likely remain profitable until either regulations change or there is too much competition in the arbitrage. Changes to the process would appear in the margins.

2) Voyager also operates like a bank. In their terms and conditions, they very clearly state “We will lend, sell, pledge, rehypothecate, assign, invest, use, commingle or otherwise dispose of funds and cryptocurrency assets to counterparties, and we will use our commercial best efforts to prevent losses.”

Basically, if you receive a loan from a bank, the loan is used by the bank as collateral for other investments. This creates multiple derivatives on a single asset.

This piece is similar to Robinhood in that the users take on counterparty risk. Should Voyager become insolvent, you will need to stand in line behind other creditors to receive your money back.

For taking on this risk, Voyager offers significant yield in a yield-starved economy. Like a bank, a minimal deposit must be kept to receive this interest payment, which can be as high as 9%. As part of this program, it may take up to 7 days for you to withdraw any crypto from your account.

Voyager Digital is engaging in fractional lending practices, which banks have been doing for centuries. However, unlike banks, Voyager is not considered a bank or a broker-dealer, so it does not provide FDIC or SPIC insurance for your crypto if there is a run on the bank, per se, or if something occurs that would prevent them from meeting obligations.

To conclude, FDIC insurance applies to the cash you hold at Voyager, but there is no insurance for the crypto held there.

Catalysts: Stablecoins and Global Expansion

Last March, Voyager acquired Circle Internet Financial’s trading app which gave them a boost of 40,000 clients. The acquisition strengthens Voyager in offering the USDC stable coin that has $7 billion in circulation. Circle is backed by Goldman Sachs and is the founder of the consortium for USDC. The USDC coin allows global transfer of dollars at an instant and for a very low transaction cost. The stable coin is part of a consortium that is also sponsored by Baidu, IDG Capital and Bitmain with participation on trading apps, such as Voyager and Coinbase. The supply of USDC has grown by 41% since the start of 2020.

A recently announced acquisition of France-based digital asset exchange LGOUY expands Voyager Digital’s reach into Europe. Similarly, the firm is targeting to grow its footprint in Canada. We believe this global expansion should further boost Voyager's platform in terms of customers and revenue.

Valuation

If we assume Voyager has doubled its revenue to $5 million (which we think is a very low estimate), the company is trading at a forward P/S of 100. There's a possibility that Voyager reports a 400% sequential increase due to the numbers presented above.

If so, Voyager is trading at a forward P/S of 50 if we assume $40 million in revenue for FY 2021 at a $2.15 billion market cap. It is plausible that Voyager will achieve this with the critical metrics provided on February 5th.

This is obviously a very high forward P/S but we think its growth will continue at an attractive trajectory due to the information presented above.

Management:

In our brief blog last week, we mentioned that the management checks out and we don't see any flags there. The CEO, Stephen Ehrlich, has experience running brokerages and financial companies. He was the CEO of E-Trade Professional Trading arm before it was bought out by Lightspeed and was then the CEO of Lightspeed Financial, the CEO of PennTrade and CEO of Tradier.

Oscar Salazar is a Co-founder and he was early in Uber as the CTO. The one issue that I do see is that they are involved in another company called Pager, a digital health startup. I prefer a founding team that has only one focus.

Risks:

It would not be a proper analysis on a crypto exchange unless we discussed the risks involved. Hacks that result in a loss of assets are no longer as likely due to enhanced security measures and custodians, yet it bears mentioning that Mt. Gox was hacked in 2014.

At the time of the hack, Mt. Gox was the largest crypto exchange globally, handling around 70% of all transactions worldwide, totaling $3 billion. The hack resulted in a loss of about 6% of all bitcoins in existence at the time. The company went bankrupt as all remaining assets were frozen. An investor who held their crypto at the Mt. Cox exchange lost most, if not all, of their investment.