Given the extreme FED action this year that has gnarled the stock market, I think it’s important for investors to look at how we got here to draw conclusions on what may be coming down the line. For brevity, we begin the discussion dating back one year.

In September of 2021, the FOMC decided to keep the Fed Funds rate at 0% and continue their asset purchasing at a regular interval, maintaining a loose policy as a result of the COVID panic. They reiterated rapid growth of the economy into 2022, while most members saw no need for a rate hike in 2022. Some members disagreed that a new tightening cycle would need to be started in 2022, but it was believed that it could be at a slow and tapered pace.

Interestingly, real-time market data related to inflation was flashing signs that inflation was becoming a concern. Here are some examples of data points that contradicted the FOMC’s policy decision at the time:

The NAHB Index, which tracks the sentiment within the home builder’s sector, saw a 160% increase from the COVID low into the September meeting.

The Case-Shiller Home Price Index was showing a ~25% increase in nation-wide home prices. It further showed the highest YoY reading in its history in July with a greater than 20% increase.

The Bloomberg Commodity Index was up 64% since the COVID low into that September, 2021 meeting. This was the highest reading since July of 2015, and also marked one of the steepest increases in terms of rate of change in the Index’s history.

Crude oil was up 47% in 2021, going into the meeting. It was also well above the pre-COVID levels.

The M2 Money Supply was up around 35% since the COVID low going into the September meeting. The M2 layer of the money supply measures the amount of liquid cash in the system, and historically accounts for inflation within an economy.

The S&P 500 was up over 100% from the COVID low going into late September of 2021.

Even the monthly CPI data, which has a built-in lag to some of its metrics, was suggesting inflation was becoming a problem. In February of 2021, the YoY CPI print came in at 1.62%; one month later, it read 2.62%. In September of 2021, it was at 5.3%.

So, what happened, and how could a team of the brightest PHDs, Bankers and Financiers that makes up the Federal Open Market Committee (popularly known as the FED) miss the inflation signals and raise rates so late in the cycle?

The standard policy for central banks is that at the first sign of inflation, they begin a slow and steady pace of rate hikes. For example, in 2004, the FED began their tightening cycle once the YoY CPI print exceeded 3%; in 1999, they began to slowly tighten once it moved above 2%. Even the current Fed Chair, Jerome Powell, started hiking rates in 2017 with inflation around 1%.

In our August webinar, ”This is Still a Warning Sign,” we warned that market risk was high, and that a sharp pullback was ahead. I also mentioned the market was setting up for a reversal going into the CPI print in September, here. Follow me on YouTube here or sign up for the I/O Fund free newsletter to be emailed the weekly webinar.In our August webinar, ”This is Still a Warning Sign,” we warned that market risk was high, and that a sharp pullback was ahead. I also mentioned the market was setting up for a reversal going into the CPI print in September, here. Follow me on YouTube here or sign up for the I/O Fund free newsletter to be emailed the weekly webinar.This is Still a Warning Sign,” we warned that market risk was high, and that a sharp pullback was ahead. I also mentioned the market was setting up for a reversal going into the CPI print in September, here. Follow me on YouTube here or sign up for the I/O Fund free newsletter to be emailed the weekly webinar.

Despite the numerous market indicators pointing towards growing inflation pressures in September of 2021, the FOMC ignored the signs, and instead continue to press their loose monetary policies. They ultimately waited a year after inflation showed up to begin addressing it, putting them much farther behind the curve than investors are used to.

Just over one month after the September 2021 meeting, the FOMC was forced to reverse course. Marking the second sudden policy shift in Jerome Powell’s tenure. As we now know, inflation was not transitory, forcing the FOMC to embark on the steepest rate hike campaign since Paul Volker raised the Fed Funds rate to 20% from a 3-year average of 11.2%.

Rather than engineer a soft landing, the FED did the opposite by raising rates a year too late. What resulted was an aggressive increase and the worst stock market on record in nearly 50 years.

One year later – Inflation is Down, the FED is Up

Fast Forward one year into the recent September, 2022, FOMC meeting, and the same indicators were clearly showing a notable reduction with inflation…

1) Commodities have collapsed, and continue to push lower. Copper prices are down ~30% from their high, while lumber prices have fallen back to pre-COVID levels. Most importantly, Crude Oil is about 16% below its pre-Russia/Ukraine war level, as gas prices declined every day? for 98 consecutive days.

2) Sales of existing homes in August declined 19.9% from August 2021. Furthermore, the Case-Shiller home Price Index showed the largest MoM decline in home prices since 2011.

3) The National Association of Home Builders (NAHB) Index fell for 9 consecutive months and is now below the 50. Anything below 50 is a contraction. The president of the NAHB, Jerry Howard, went as far to state that “we’ve given birth to a housing recession.”we’ve given birth to a housing recession.”

The last time we saw the NAHB Index below 50 was briefly around the COVID low and then again in 2014. In fact, the last 9 months saw the 3rd steepest % decline in the NAHB Index since 1990.

4) The M2 money supply is one of the most important indicators of inflation, and is the layer of the money supply that tracks liquid money in bank deposits, CDs, Mutual Funds, etc. In other words, the money that is ready to be used in an economy. After seeing a 35% increase post-COVID, since February of 2022, the M2 money supply has been negative to flat.

Ultimately, inflation is a monetary phenomenon. The more money in the system chasing the same goods, inherently means goods will increase in price. Following the M2 money supply is the most effective way to track if inflation is growing or shrinking.

The list can be extended into Producer Price Indexes and Manufacturing Costs consistently surprising to the downside. Inflation data does not have a lag built into its calculations, and looks at real-time market information, is signaling a noticeable change in trend with inflation pressures. Yet, just like in 2021, the FOMC appears to have a disconnect between inflation and its policy, except in the opposite direction.

The market was expecting a 0.75% rate hike this round, which it got. What it was not expecting was for the FOMC to raise its target rate, extend the duration for rate cuts, and claim that inflation is still out of control. They further spooked the market by stating that more pain would be needed to bring inflation back to its 2% target. This was backed by lowering their economic growth forecasts for this year, down to 0.2% from 1.7% in 2022, and 1.2% from 1.7% for 2023.

This meeting caught the market by surprise, triggering a sell-off that has pushed the S&P 500 to new lows in just under 2 weeks. I provide weekly webinars that discuss what I/O Fund is buying and selling. We also have a proprietary hedging signal that we monitor in real-time. Following the free analysis, Why The Next 2 Weeks Could Determine The Rest Of 2022 Why The Next 2 Weeks Could Determine The Rest Of 2022 we hedged going into the CPI number for a nice gain in a tough market. That analysis dated September 8th stated:

“Historically, this grid tends to accompany the C wave down in a bear market. However, in 2022, the market exhibited a sell-now-and-ask-questions-later mentality, as we saw the S&P 500 decline by 24% and the NASDAQ-100 decline 34% over a 5.5 month period. These are rare moves, and one has to wonder if the worst is priced in – including the global slowdown in growth? I do believe it’s cavalier to assume that at this point, and prefer to let the broad market prove it to me over the coming month. We will remain cautious until then, and respect the Big Risk-Off grid that we are now in.

If we have, in fact, found a meaningful low, we would not only need to see the S&P 500 give us that 5th wave up, but we would also need to see rates, the USD and oil move down or sideways. Bull markets do not happen in vacuums and tend to be supported by various markets firing in unison. As of today, this confluence of inter-market dynamics is not supporting a direct uptrend in equities.”

Just like in the September of 2021 meeting, the FED appears to be ignoring market signals about inflation. By ignoring the real-time market data regarding inflation, the markets will once again force their hand, as it always does. The only question remains is what will have to break before they flinch? As stated, we believe it is prudent to wait for the clear reversal before getting too aggressive in equities. This is why our service has hedged the majority of September with real-time trade alerts sent to our Members.

SPX Levels to Watch

The S&P 500 is tracing out what appears to be a 3-wave pattern down from the August high. This is important, because it is not suggesting an immediate breakdown from current levels. Instead, we are seeing extreme oversold conditions that tend to lead to a short-term bounce, at minimum.

If the coming bounce can break above 3800, then a major low is likely developing. However, once SPX pushes into 3730, the risk will be elevated, as the above structure does not look complete until we get at least into the 3550 range.

To further support a bounce, today we saw the broad market make a new low; however, it did so with notable divergences. For one, the VIX did not make a new high, which tends to precede a turn. The market also went down with less stocks making new lows than last week’s low. This was met with the Advance Decline line also not making a new low with price. These are common signs we see prior to a turn.

On the I/O Fund premium site, I provide weekly webinars that discuss what the I/O Fund is buying and selling. We also have a proprietary hedging signal that we monitor in real-time. Following the analysis I provided for free on YouTube last month “This is Still a Warning Sign” and also in this article “Why the Next Two Weeks Could Determine 2022” we hedged going into the CPI number for a nice gain in a tough market and have had a hedge in place most of September.On the I/O Fund premium site, I provide weekly webinars that discuss what the I/O Fund is buying and selling. We also have a proprietary hedging signal that we monitor in real-time. Following the analysis I provided for free on YouTube last month “This is Still a Warning Sign” and also in this article “Why the Next Two Weeks Could Determine 2022” we hedged going into the CPI number for a nice gain in a tough market and have had a hedge in place most of September.I/O Fund premium site, I provide weekly webinars that discuss what the I/O Fund is buying and selling. We also have a proprietary hedging signal that we monitor in real-time. Following the analysis I provided for free on YouTube last month “This is Still a Warning Sign” and also in this article “Why the Next Two Weeks Could Determine 2022” we hedged going into the CPI number for a nice gain in a tough market and have had a hedge in place most of September.

The next premium webinar will be on Thursday, October 6th at 4:00 pm Eastern where I will discuss how I plan to trade the broad market signals discussed in this article plus new information on an important time factor in mid-October which I believe is lining up with the Q3 earnings season. Learn more about Premium I/O Fund Services here.The next premium webinar will be on Thursday, October 6th at 4:00 pm Eastern where I will discuss how I plan to trade the broad market signals discussed in this article plus new information on an important time factor in mid-October which I believe is lining up with the Q3 earnings season. Learn more about Premium I/O Fund Services here.Premium I/O Fund Services here.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

Marvell’s management team did an excellent job of acquiring Inphi and executing. Typically, we avoid M&A for a year to allow the financials to merge, yet in this case, leaning into the acquisition was a good choice.

The Marvell management team’s execution skills are needed once again because Marvell has an opportunity to greatly increase its revenue and profits if management can execute in a new market one more time. The opportunity is a new architecture called CXL that disaggregates memory from the CPU. CXL is attracting a lot of attention at industry events, such as Hot Chips 2022, because it’s focused on optimizing one of the most expensive parts of the data center – which is memory.

Before we go into the 2023-2024 Marvell product road map, and why it’s key to the company’s future, I want to discuss the fiscal Q2 2023 earnings.

Fiscal Q2 2023 Earnings Overview

The market is concerned over Marvell’s data center guidance of 20% growth next quarter. This is a slowdown from the most recent quarter at 48% YoY growth and earlier quarters at >100% growth.

At an estimated $600 million, it will also mean a sequential decline both from Q2 and Q1, which were at $643M and $640M, respectively. Marvell stated it’s the on-premise business weighing on their cloud data center business and supply issues (more below).

Notably, Q2 of last year was an important moment for the company when 56% sequential data center growth grew from $277 million to $434 million in the span of three months following the close of the Inphi acquisition in April 2021. From there, the company has sustained Inphi’s already high growth levels for over a year.

The company is now at an annualized run rate of $6 billion, which the CEO reminded analysts, was the target for October of 2023. The company met the target originally provided at the October 2021 Investor Day one year earlier than expected. Notably, this was six months after Inphi was closed so M&A not a factor here.

Marvell’s Segment Overview:

The data center represents 42% of revenue at $643 million and grew 48% year-over-year.

The carrier infrastructure segment, which is wired and wireless and reflects 5G growth, reported 45% YoY to $285 million.

Enterprise networking grew handily at 53% YoY to $340 million and is expected to grow at 70% next quarter. We break this segment down below.

Consumer was down (1%) to $164 million and is expected to be down (10%) next quarter. Marvell has exposure to the storage market and this can weigh on the more robust segments.

Automotive was up 46% YoY to $84 million and is expected to be up 40% YoY next quarter. We also break down this segment below.

Marvell Financial Overview

Marvell was reporting negative top line revenue when we first covered it in 2019 and Marvell took another hit on revenue during Covid before accelerating to the 50%-74% revenue growth range.

The current quarter’s top line revenue in Q2 was at 41% which is a deceleration from Q1 with 74% revenue growth. The company guided for 29% year-over-year growth, which was a slight miss as analysts were expecting 30.3% growth in the fiscal Q3 quarter. The company reported EPS in line with adjusted EPS of $0.57. The guidance on EPS was a slight miss, however, at $0.59 reported versus $0.61 adjusted EPS estimated.

Semiconductors make a tougher investment as analysts can’t model too far into the future beyond what management teams provide. That is why there were many questions looking for help with how to factor in the “acceleration” in the data center the Marvell team is expecting in Q4 and what this will mean for CY2023.

An analyst asked if they can assume 10% QoQ in the data center for $1.7 billion overall revenue and the CEO said it sounded “a little on the high side.” This has led to analysts modeling $1.65 billion in revenue in Q4, for 22.5% growth. Therefore, despite a single-digit acceleration in the data center segment, there will still be a top line deceleration, if today’s forecast does not change.

The company’s margins and cash flow are a bright spot, and I believe this is being overlooked. If we get an acceleration in the data center into next year, then Marvell is fundamentally a much stronger company than it was during the previous data center streak.

On a GAAP basis, the gross margin was at 51% in the most recent quarter, up from 35% in the year ago quarter and up from 46% in FY2022. The company is guiding for the same GM of 51% next quarter.

The GAAP operating margin has improved quite a bit YoY to 8.3% in the current quarter compared to (25%) in the year ago quarter. This is also an improvement from Q1 with GAAP OM of 4.80%. The adjusted operating margin “hit a record” at 36.5% and is guided for 37% next quarter. Stock based compensation was at $139 million in the most recent quarter.

Cash flow is also improving with operating cash flow at $332 million, or 22% of revenue. This compares to $194 million last quarter and $819 million in FY2022. However, the company carries debt of $4.6 billion and has $617 million of cash on the balance sheet. This is a 1.8X net debt to EBITDA ratio.

Therefore, there has been substantial improvement yet Marvell does have a weaker debt profile than a company like AMD or Nvidia.

Source: YCharts

Note on Supply:

Marvell is aligned with AMD in that they believe supply chain issues will ease in Q4 and into 2023. Here is what Marvell said in the opening remarks:

“Therefore, for our overall data center end market, we project revenue in the third quarter to decline sequentially in the mid-single digits on a percentage basis. However, we expect our data center revenue in the fourth quarter to increase on a sequential basis, anticipating an improvement in supply and new product ramps in cloud.”

Here is what AMD said:

“The visibility with our customers, especially our large cloud customers’ second half of this year into next year is very good. And we’re planning really for the next four to six quarters, and that gives us good visibility” and later provided many references toward supply coming online in Q4, such as: “But overall, the 7% increase [in gross margin], I think, is very well supported given all of the new product ramps that we have going on in addition to some additional supply that’s coming in as we get into the fourth quarter.”

It never hurts to have two management teams agree on the larger broad-based issue. However, since those reports, we’ve seen analysts cast doubts on the effects of macro for the rest of the year: “[Mizuho analyst Rakesh] checks show hyperscale orders are seeing "pushbacks" but no cancels, with Q3 trending flat quarter-over-quarter and Q4 "potentially soft." Rakesh lowered estimates for AMD "with macro headwinds clouding the near-term outlook."

Marvell’s Products:

In six brief years, Marvell has pivoted away from consumer (storage) products as the revenue mix was previously 62% consumer/38% infrastructure to being 11% consumer/89% infrastructure today.

This was driven partly by hyperscalers building data center infrastructure and AI/ML driving the need for faster data speed. Inphi also contributed to this.

Data Center Segment

PAM Solutions:

Marvell offers 200-gig and 400-gig PAM-based electro-optics — and the company recently added 800-gig solutions. This market sees tailwinds from the need for more bandwidth as the electro-optics connect short distances and long distances to increase data rates. PAM4 has replaced NRZ data transmission with the benefit of doubling the bit rate.

Hyperscalers are going through an upgrade cycle that requires high bandwidth and port density. PAM4 connects networking ASICs and machines, like servers and AI machines. Digital-based PAM4 uses analog-to-digital converters to clean up the signal in the digital domain before converting it back to analog to transmit.

Artificial intelligence and machine learning drives demand for the 800-gig PAM to increase the speed of input-output and to process the data flows. This doubles the throughput (bandwidth) due to an 8x100Gpbs optical transceiver for inside and between AI clusters.

In the fiscal Q1 results ending in April, management had stated: “our first quarter results benefited from a ramp in volume shipments of our 800-gig PAM solutions at two large customers.” The company has also stated that their products will see increase demand with the release of more powerful CPUs.

COLORZ 400:

COLORZ allows regional data centers to be linked together in the same metro region to function as one single mega data center. COLORZ silicon photonics technology allows data centers in the same metropolitan region to function like a mega data center through a “network fabric.” This facilitates faster edge computing within an 80/120 km distance for 30-megawatt data centers as they will be linked together and function like a 120-megawatt data center.

“As artificial intelligence (AI), machine learning (ML) and high-performance computing (HPC) applications continue to drive greater bandwidth requirements, cloud-optimized 400G solutions are needed to support high-speed data center interconnections. These requirements can only be met through high bandwidth connectivity offered in a small, cost-effective form factor. The Marvell COLORZ II 400ZR enables cloud data centers the ability to increase the speed of data movement while keeping the power and cost low.”

Another press release stated the company shipped 100,000 units.

Here is what was said on the call about how/why the growth in the data center can continue:

Harlan Sur

Good afternoon. Thanks for taking my question. On the cloud optical connectivity business, this is both inside and between data centers, the upgrade cycles have been this really great multi-year tailwind for the team.

And if I look into next year, I believe that there's still at least one of the top four US hyperscale titans that's going to start the 400-gig PAM4 transition. You still have China CSPs that need to fire. You've got multiple customers on DR that's going to fire as well. Historically, like these transitions, I don't think have been impacted by a slowing macro demand environment. They're viewed as, I think, very strategic.

But is that how your cloud customers are thinking about these upgrades and your views on continued upgrade momentum in this segment for next year? And just relatedly, is the Innovium team on track to drive $150 million in revenues this year?

Matt Murphy

Hey. Thanks, Harlan. Yes, I think the first part of it, you got pretty well in terms of the transition on 200 and 400 gig PAM4 inside the data center. And then, the new ramps we're seeing in 400 gig ZR for DCI between data centers.

What I'd add on top of that is — which has been extremely strong and also, in some ways, a little bit of a constraint we've seen in terms of being able to keep up is, the demand on 800 gig, which is happening right now really around, obviously, very advanced AI workloads.

That is an area where, if we could obviously produce more material, we would be shipping it in Q3. So that's also a positive trend. So you've got sort of the transition going on all the way up to 800 gig, and that continues to look pretty good.

NOTE: Innovium is an acquisition that closed in 2021 and at time of acquisition was expected to add $150 million in revenue for CY2022/FY2023.

Compute Xpress Link (CXP): 2024-2025 Data Center Catalyst

Marvell is launching a new product line called CXL, which will improve how data centers add memory. Right now, a server must be opened to add DRAM and the DIMM slots are limited in number and don’t pass service history or bit-error history, which is needed by hyperscalers.

Memory pooling allows memory to scale independently from processors by taking memory for a task and then releasing the memory. The new fabric removes the need for local DRAM, which adds a bit of latency from 100ns to 140-160ns, however, there’s a possibility of adding a CXL accelerator to be more “cache coherent.”

The CXL switch will be used to accelerate protocol-level processing across ethernet, DPUs, SmartNICs and solid-state drive controllers (SSD).

What Marvell is proposing with CXL is a new server architecture to “dynamically assign memory resources between servers.” The result is boosted memory bandwidth and also the ability to enable memory pooling. The company sees a future where a new architecture will separate compute, memory and I/O racks with the interconnect being CXL.Partially-disaggregated racks are expected to deploy in 2024-2025.

Marvell is at the forefront of the shift toward “disaggregate memory from the CPU” because it currently supplies the optics that this new fabric will disrupt. Inphi is the leader in silicon optics, PAM-4, and the encoding of PAM-4 for PCIe 6.0.

2024 seems like a long ways off yet the market will be paying attention to this In Q2/Q3 2023.

“As you recall from our discussion last quarter, we see CXL as the next big evolution in cloud data centers that will enable us to increase our reach into the memory ecosystem and presents a multibillion-dollar SAM expansion opportunity for Marvell.

This includes a host of new products such as CXL expanders, cooling devices, switches and accelerators and the potential to embed CXL IP and a broad range of our data center products. Events and presentations at FMS strongly validated our excitement around CXL. This is the hottest topic at FMS with standing room-only presentations by many leading industry participants.

The Marvell booth, we demonstrated the industry's first CXL memory pooling solution, addressing the challenges related to memory scaling and cloud data centers. While the industry is still in the early stages of CXL adoption, we are working on closing significant opportunities right in front of us at key customers and envision a strong design win pipeline.”

Why Marvell for CXL?

There are a handful of companies going after the CXL opportunity. Marvell could be front runner as the company already works closely with memory OEMs by supplying HDD controllers, SSD controller and preamplifiers. The company also has an aggressive PCIe roadmap with the company shipping Gen 5 sockets whereas most SSD device are shipping Gen 4 solutions. Marvell is already investing in Gen 6, which in turn, attracts more Tier 1 memory OEMs.

Marvell acquired Tanzanite, a developer of advanced CXL technologies. The company plans to expand to CXL expanders, cooling devices, switches and accelerators.

The company has stated this will drive “a multibillion-dollar PAM expansion opportunity driven by CXL overtime.” (Note: Marvell is referring to PAM, their premiere product)

We will focus on this more next year. You can listen to a recent tech talk here on CXL. The presentation is located here. This is an article about Microsoft’s interest in CXL with a statement that “50% of their server costs are taken up by DRAM.”

Carrier Infrastructure:

The OCTEON processors and platform is an Arm-based compute architecture for embedded applications, such as wireless networking equipment including 5G, including switches, routers, firewalls and monitoring solutions.

The OCTEON DPU is used with SmartNICs and security accelerators with a 5nm design that delivers to the infrastructure industry the same processing node as consumer smart phones and high performance computing and shipped in 2021. The most recent release from last year was the OCTEON 10 DPU and Prestera carrier switches which combined consumes 50% less power than competitors (according to Marvell).

Marvell’s processors help 5G networks meet latency and bandwidth demand while also allowing the networks to upgrade as cellular standards evolve. Marvell also offers customized solutions, which is ideal for Tier 1 customers who can combine their IP with Marvell’s Arm v8 processors and accelerators.

Recently, Dell and Marvell partnered to develop a server-class accelerator card for 5G base stations based on Marvell’s arm-based OCTEON Fusion processor. The hardware accelerators deliver more processing power including processing solutions for smart radio heads to support massive MIMO antenna rays.

We wrote about MIMO a few years back in a reference guide: “Massive Multiple Input and Multiple Output (MIMO) sends the data through multiple data streams called layers, which increases parallelism and throughput. MIMO helps avoid lost signals with multipathing, which allows the base station to send multiple copies of the same signal for increased redundancy.

Note: The antenna array is one fundamental change to 5G infrastructure. The initial 5G rollout will use existing cell towers, however, newer, dedicated 5G network infrastructures will require many more antennas than used in previous generations. Read more.”

The distributed unit (DU) shares the load with the radio unit by running L1 functions on the RAN protocol. Marvell has been a proponent of OpenRAN with the O-RAN platform, which is an open protocol and open platform that allows Marvell’s hardware to be used with various software vendors. Facebook (Meta) is a partner with Facebook Connectivity.

DPU processors, or digital processing units, are gaining traction for 5G transport, 5G RAN intelligent controllers, edge computing and cloud data center workloads. These hardware accelerators enable high speed connectivity and can improve packet processing rates by 5X. DPUs are ideal for power sensitive edge applications. Marvell’s strength in DPUs is one reason it may be able to stave off competition, which in the narrow field of 5G base stations includes Qualcomm/HPE and Analog Devices. Beyond 5G, Marvell has other competitors for DPUs such as AMD/Pensando and Nvidia.

Regarding 5G, over 7 million of the Octeon processors have been used in 3G, 4G and 5G base stations with Tier 1 customers. In the past, we reported that Samsung and Nokia use Marvell, and supplying these particular companies was a tailwind when Huawei was blacklisted. More recently, Marvell has stated they have design wins with four of the top five global OEMs and next-tier OEMs building base station equipment. These design wins are based on the 5nm platform.

Marvell uses TSMC for the 5nm OCTEON DPUs and this is an advantage because Marvell has the 5nm now and is able to move quickly on a 3nm release.

Notably, 5G has been a long time coming but I do believe it will reward investors over the next few years. Technavio has a CAGR of 67% for 5G equipment through 2025. The growth trend of 5G/edge computing is not one that we plan to complacent on as it will provide the next leg up for substantial capex spending similar to data center capex spending.

Enterprise Networking:

Marvell sells ethernet switches and ethernet PHYs to IT managers and networking equipment manufacturers. The company uses DSP technology for CAT5e ethernet cables to supply data rates up to 5Gbps with support for CAT6 and CAT6a.

Management discussed on the call that the main driver for this market right now is wireless, specifically WiFi 6 as the wireless rate line is now faster than the wired rate. The call also pointed toward content per port going up in the transition to multi-gig. According to the CEO, “it's not like 10%, 20%, 30%. It's sort of multiples on a per port basis of where it was before.”

Increased enterprise share and content gains from wired and wireless enterprise networking drove 53% YoY revenue growth and 19% QoQ revenue growth.

Automotive:

Similar to the networking that Marvell supplies enterprises and the data center, Marvell also supplies auto manufacturers with ethernet PHY transceivers, camera bridges and switches for in-vehicle networks. This is used for things like collision detection, lane warnings, and autonomous driving.

Marvell believes Ethernet will be the backbone for connected and autonomous vehicles to connect the electronic control unit (ECUs), cameras, sensors, and central compute devices. The Ethernet device is called Brightlane.

ON Semi has partnered with Marvell on use cases such as pairing a standardized protocol, such Ethernet PHY, with ON’s portfolio of ultra-dynamic range image sensors.

Automotive was up 46% to $84 million, yet was down 6% sequentially. Management cited supply issues rather than demand. Marvell counts eight of the largest 10 OEMs worldwide and 36 OEMs total. The company believes revenue growth will be 40% next quarter.

Note on Consumer Market:

Marvell sells hard disc drives (HDD) and solid state disc (SSD) controllers. This is a weaker segment, declining 1% YoY and 8% sequentially to $164 million. For next quarter, Marvell expects revenue to be down 10% YoY and flat sequentially.

Conclusion:

There is a new, powerful trend on the way that is on par with the cloud computing trend. This trend of edge computing will rely on distributed computing rather than centralized processing. Both will exist and rely upon each other but edge computing will have a stronger growth trend when it breaks ground (by virtue of being new/rapidly expanding). Much of this will be in sync with the 5G buildout.

Marvell has the potential to be a strong stock during this buildout as the company provides the base station hardware, supports MIMO antenna rays, beamforming, and accelerates 5G transport and controllers which results in high-speed connectivity.

The company also provides electro-optics and silicon photonics for increased data rates and a network fabric for edge computing. The edge is defined as many things, but what all definitions can agree on, is that the edge needs superior connectivity/networking. Electro-optics, silicon photonics, DPUs, SmartNICs and ethernet in the data center are a warmup for Marvell supplying edge servers and edge devices. As this occurs, the demand for Marvell’s product suite will increase.

In addition to this, Marvell is thinking outside the box by focusing on restructuring memory while most companies are focused on more powerful chips. CXL drives down costs on DRAM and is likely to rapidly adopted by hyperscalers once it becomes available. There’s no guarantee that Marvell will be the one to win the contracts but it’s certainly a front runner.

This article was originally published on Forbes on Sep 23, 2022,04:33pm EDTForbes on Sep 23, 2022,04:33pm EDT

Nvidia had a big week with GTC 2022 and management is clearly ready to rumble against any excess inventory from crypto mining. The negative catalyst from crypto mining and Nvidia's price action is eerily similar to Q4 2018/Q1 2019 —- yet the company is not the same company it was four years ago. This is apparent by Nvidia flexing some major product muscle by timing it's best-ever gaming release and it's best-ever AI chip to hit the market in October.

We draw important parallels (pun intended) between the last crypto mining selloff and this selloff with key reasons as to why this time the stock's comeback will be quicker.

Nvidia stock has been in the clutches of a steep drawdown after the company has faced nearly every headwind imaginable: United States-China tensions, supply chain disruptions spanning many components, tough comps on the data center, tough comps on gaming, and a less-than-rosy macro environment.

The most impactful headwind, however, was Ethereum’s merge to Proof of Stake (PoS), which ultimately lowers demand for gaming GPUs. This contributed to a $2.5 billion cumulative miss in revenue driven by the gaming segment.

Nvidia’s stock performance in 2018 and 2022 feels eerily similar as the stock sold off 54% in 2018 specifically because of a gaming miss tied to crypto mining. Today, Nvidia is currently 57% YTD.

It took eighteen months for Nvidia to recover its all-time high from the Q4 2018 selloff (Sept 2018 through Feb 2020). Despite the uncanny similarity that 2018 and 2022 may have — Nvidia is actually a much stronger company today than it was four years ago.

Below, we discuss a few key reasons Nvidia stock will recover quicker this time around.

Drilling into Parallels Around the Gaming Miss

During the Q3 2018 results released in November 2018, Nvidia gave Q4 2018 revenue guidance of $2.7 billion, below the analysts’ consensus estimate of $3.4 billion. In January 2019, the company again lowered revenue guidance from $2.7 billion to $2.20 billion, which suggests a total revenue miss of $1.2 billion. Gaming revenue in Q3 2018 was $1.76 billion, up 13% YoY and down 2% QoQ. In Q4 2018, gaming revenue was $954 million, down 45% YoY and down 46% QoQ.

In the most recent quarter ending July 2022, the company missed on gaming with revenue of $2.04 billion, which is 33% lower than the year ago quarter and 44% lower sequentially. The company is expecting a further decline in gaming sequentially for Q3. According to one analyst on the call, they are modeling for a further 30% sequential decline in gaming and professional visualization offset by low to mid-single digit growth in data center and automotive. The CFO affirmed this understanding is correct.

After 2018, although it took Nvidia eighteen months to reclaim its all-time highs, in 2020-2021, Nvidia would go on to stage a remarkable turnaround as the stock led tech mega cap stocks in gains. This was not simply because all tech performed well during those years – if you compare Nvidia to Meta, Amazon and Google, you’ll see something unique occurred with Nvidia that caused the stock to outpace its peers. In all cases except Apple, Nvidia doubled, tripled or quadrupled the performance of other mega cap stocks.

Source: YCHARTS

Perhaps most impressive, Nvidia is still in the lead over all mega cap stocks despite a 57% drawdown this year. It’s the company’s past performance that makes it well worth the time to answer: can Nvidia do it again?

Sign up for I/O Fund's free newsletter with gains of up to 403% – Click hereSign up for I/O Fund's free newsletter with gains of up to 403% – Click hereClick here

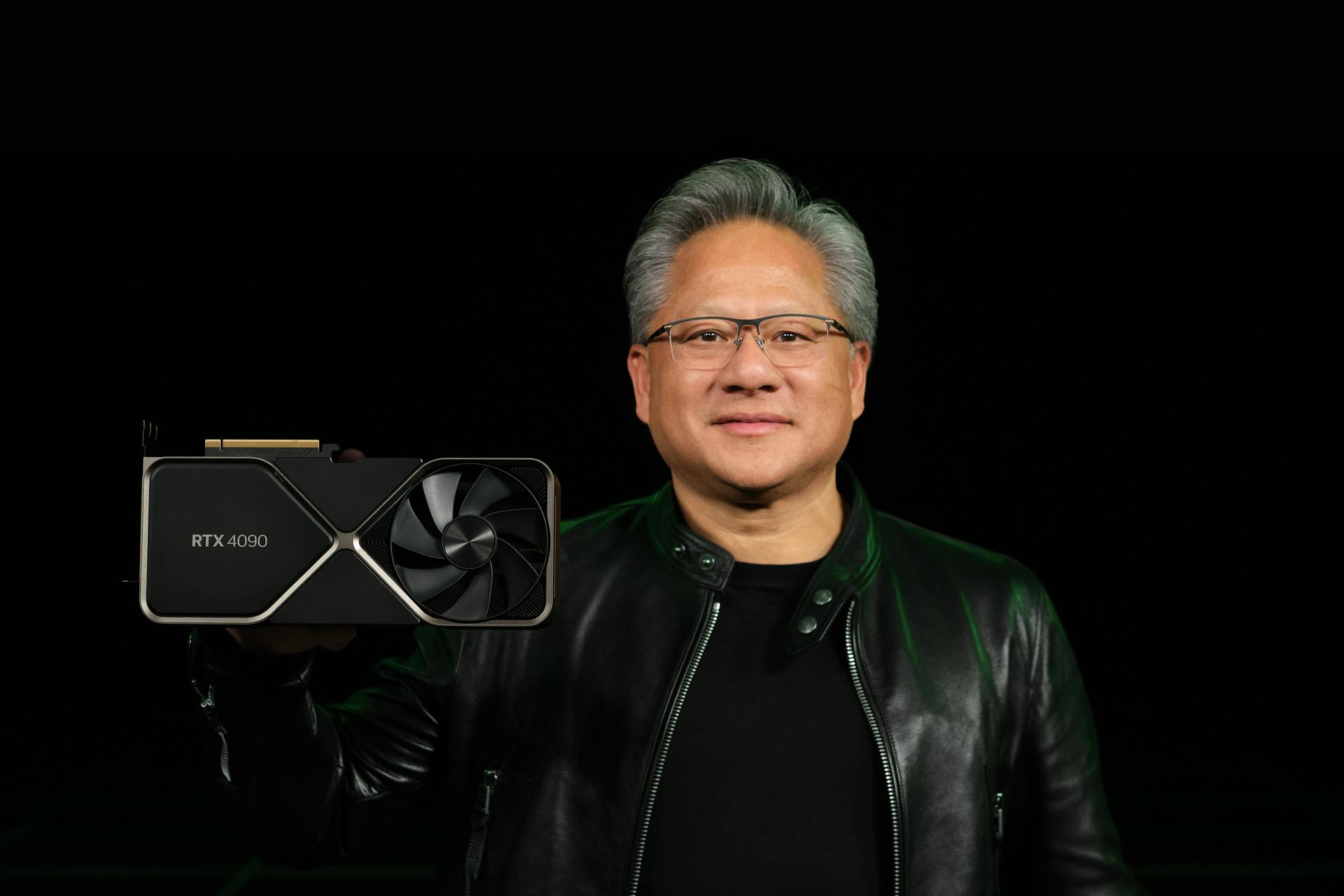

Nvidia’s GeForce RTX 40 Series is Perfectly Timed

Next quarter, Nvidia was expected to report $6.92 billion and the company guided for $5.9 billion. This is down from $7.10 billion in Q3 of last year. This will be a 17% decline in revenue. Due to this, analysts expect Nvidia to end fiscal year 2023 with 0.8% revenue growth, or $27.13 billion in total revenue.

It’s not only the top line valuation that is affected by this cut in guidance but it’s the bottom line, as well. In previous quarters, high average sales prices drove $2 billion to $3 billion in operating profits and net profits, whereas in the most recent quarter, the company is reporting $500 million and $656 million, respectively.

The GAAP EPS reported was $0.26 compared to $0.94 in the year ago quarter. Adjusted EPS was $0.51 versus $1.04 for the year ago quarter.

Although it’s tempting to redirect the conversation toward higher-growth segments, the $2.5 billion total miss between two quarters came from gaming and it’s prudent for investors to start here (for now) when analyzing the stock for a potential recovery.

The company stated the miss was driven by both lower units and lower average sales prices including reduced consumer demand. The company is not commenting on crypto as they state they have no visibility here as to how the GPUs are being used, however, it’s certainly contributing to the bulk of this decline.

Notably, AMD reported gaming growth of 32% to $1.7 billion which provides a better picture of reduced gaming demand minus crypto. Nvidia believes some of their weakness is also from preparation for a new product generation that will be announced this month.

Per the earnings call, there are two ways that Nvidia plans to overcome the crypto mining selloff which could produce a faster rebound than 2018.

First, Nvidia is restricting supply on its current gaming model. Per the CFO: “Across those two quarters, the Q2 of ‘23, the Q3 of ‘23, we have likely undershipped gaming to our end demand significantly.”

Following the call, we estimated for our premium members that the amount undershipped is a minimum of $1 billion. The reason behind this is to help keep prices stable and to increase demand for the RTX 40 Series.

Second, Nvidia announced its GeForce RTX 40 Series at the GTC 2022 Conference this week.

The new Ada Lovelace architecture which uses 76 billion transistors and a 4nm production process. In the keynote, the CEO stated: “Nvidia engineers worked closely with TSMC to create the 4N process optimized for GPUs. This process let us integrate 76 billion transistors and over 18,000 CUDA cores, 70% more than the Ampere generation.”

The improvement from 8nm to 4nm means more transistors on the GPU, which results in better performance as the 4nm processes data faster.

In the gaming world, this much anticipated release is expected to be 2-4X faster than the RTX 3090 Ti. The flagship AD102 GPU model will have 144 individual streaming multiprocessors (SMs) in one die compared to 84 SMs in the Ampere architecture. As stated, the AD102 will also have a 70% increase in CUDA cores over the RTX 3090 Ti.

In addition to this, Nvidia is releasing a new feature called Shader Execution Reordering (SER) which will improve ray-tracing performance by 3X with 25% faster frame rates. Rather than deliver workloads sequentially, the GPUs are able to reorder the workloads to process more workloads at once which results in more power and better performance.

Deep learning super sampling (DLSS) refers to using AI to predict the next pixel. The new DLSS 3.0 not only predicts pixels but will also use AI to predict frames. This results in “up to four times” better performance over traditional rendering.

The first release date for the RTX4090 models is October 12th with a starting price of $1,599. There is a second release date in November for the RTX4080 models with prices of $1,199 and $899. Notably, mid-range RTX 40 series will outperform the previous generation’s high end models. This is due to the Ada Lovelace architecture which offers 1,400 Tensor TFLOPs versus 320 Tensor TFLOPs which means the DLSS is superior and the high-end RTX 30 Series cannot compete with the mid range RTX 40 series.

The popularity of this release will help determine if Nvidia can stage a comeback in the gaming segment. Here is what analysts are saying:

“Morgan Stanley analyst Joseph Moore said his "biggest takeaway" from the keynote at Nvidia's GTC conference were the higher prices of gaming GPUs, which increases his conviction about the pace of gaming revenue recovery next year. Prices that are 28% higher than the baseline price from two years ago for the higher volume 4080 should drive material growth in revenue, said Moore, who sees revenues in the gaming segment rebounding from the current quarter run rate of $5.5B or so to $9.5B next year.”

“Given the channel inventory work downs in the July and October quarters, the products should be "strong demand catalysts" into 2023, Harlan Sur of Chase tells investors in a research note.”

Nvidia Continues to Build a GPU Moat with H100

In 2018, we stated in our free newsletter that Nvidia had built a moat in the GPU-powered data center. This was a bold statement as the company would go on to have negative year-over-year data center revenue in 2019. Yet, fast-forward and it’s quite clear that Nvidia is unshakeable in this segment, which has surpassed gaming as Nvidia’s most valuable segment.

I’ve written quite a bit about Nvidia, which you can reference here and also here. However, I will keep it simple by saying the A100 GPU is what led the company’s gains since Q2 2020 (detailed here) and the Hopper H100 GPU is what will lead the company’s gains for the next two yearsdetailed here) and the Hopper H100 GPU is what will lead the company’s gains for the next two years.

In the most recent quarter, data center revenue of 61% is down from 83% last quarter yet accelerated YoY from 35% growth in the year ago quarter. The earnings call reviewed some of the challenges Nvidia faced in the quarter that led to the 1% sequential growth.

First, Chinese hyperscalers slowed their infrastructure investment this year yet the slowdown is unlikely to last much longer. Due to being a large market for Nvidia, the data center growth was impacted by this. The reason Nvidia was able to meet expectations is because “North America doubled year-over-year in revenues.” As of now, supplying the Chinese military is restricted for Nvidia, but this does not include supplying the hyperscalers.

Second, demand continues to outstrip supply yet there are many components to Nvidia’s systems and they are experiencing supply chain issues.

“We were challenged this quarter with a fair amount of supply chain challenges because as you know, we don’t just sell the GPU chip, but these systems are really complex with a large number of chips in the system components that we offer like HGX […] all of the components that have to come together for us to be able to deliver the final component.”

H100 Hopper Coming in October

On the earnings call, an analyst asked if the company expects data center growth to re-accelerate when Hopper ships: “Do you think that Hopper, as that comes fully available, it sounds like in fiscal 4Q, that you actually see Data Center growth reaccelerate as that product cycle materializes.”

The CFO Kress stated: “Our Data Center yes, we do expect it to grow. It may grow about what we just saw between Q1 and Q2. We’ll continue to look at it.”

I believe this means the data center will accelerate above 61% but not to exceed the 83% from Q1. Ultimately, the CFO may not have full visibility into Hopper sales until the units ship and are tested by customers, who in turn, often buy more if the product exceeds expectations.

On that note, the new 4nm chips are bound to impress. The H100 GPUs and the DGX H100 server pods and super pods offer Nvidia the next leg-up as the company has solved an important bandwidth issue.

Hopper tackles some of the bigger issues around previous generations like speeding up algorithms by offering dynamic programming on GPUs to break down problems to simpler subproblems. The new GPUs also boost bandwidth by 3X with SHARP in-networking computing and Infiniband Switches, and the H100 can leverage NVLink to connect eight H100s into one giant GPU for 640 billion transistors, 32 petaflops, 640GB of HBM3, and 24 terabytes per second of memory bandwidth.

The H100 has about 50% more memory and interface bandwidth than the A100. That’s 1.5X more bandwidth with the NVLink connection and PCIe 5.0 doubling the bandwidth of PCIe 4.0. The H100 will ship with support for 80GB of HBM3 memory at 3 TB/s speed

Where the H100 really stands apart is the leap in performance with about 3X more performance than the A100 and the H100 is up to 6X faster. The A100 lacked support for FP8 compute at default whereas the H100 will leverage a transformer engine to switch between FP8 and FP16, depending on the workload.

According to Nvidia, the H100 delivers 9X more throughput in AI training, and 16X to 30X more inference performance. The company also states in HPC application-specific workloads, the H100 is 7X faster. The goal of the H100 was not only to add more transistors and make the H100 faster, but to also offer function-specific optimizations. This is achieved through the transformer engine.

Last week, MLPerf published artificial intelligence performance tests. The parent company MLCommons provides the industry standard for benchmarking deep learning, AI training, AI inference and HPC. The H100 Tensor Core GPUs delivered 4.5X more performance than the A100 in offline scenarios and 3.9X more in the server scenario compared to its predecessor the A100.

The Hopper H100 GPUs are in full production and availability starts next month and will have over 50 server models by the end of the year and “dozens more in the first half of 2023.”

Sign up for I/O Fund's free newsletter with gains of up to 403% – Click hereSign up for I/O Fund's free newsletter with gains of up to 403% – Click hereClick here

Nvidia’s Automotive Opportunity is Massive

Nvidia’s lead in automotive across dozens of OEMs requires its own analysis, which we will write for our free newsletter subscribers next year. Hyperion 8 is shipping in 2024 and Hyperion 9 will ship in 2026. However, as long-term Nvidia investors, now is a good opportunity to remind my readers of the long-term vision for yet another large and sweeping revenue segment.

Although a small segment today of only $220 million, automotive grew 59% sequentially and 45% year-over-year. The company has a $11 billion automotive design win pipeline.

At GTC this week, Nvidia announced a new superchip named “Thor” which will deliver 2,000 teraflops of performance, up from 200 teraflops from the current generation “Orin.” The chip has a transformer engine which can process video data as a single perception frame and offers 8-bit floating point (FP8) precision to avoid task loss when converting model data from one platform to another platform.

More on the Omniverse

We’ve covered the Omniverse platform in the past including an interview with Nvidia’s Richard Kerris you can view here.

At GTC this week, Nvidia launched Omniverse Cloud, which is a infrastructure-as-a-service software offering to reduce the complexity around building 3D virtual worlds and assets. This removes the need for local compute power and opens up the ability for more creators to access 3D world creation.

Regarding the China Restrictions

The United States government is restricting sales of high-performance chips to China as Nvidia’s AI chips could be used for military purposes. A spokesperson for Nvidia stated the products where the new licensing requirement applies is the A100, H100 and systems that include DGX.

The restrictions apply to Russia yet Nvidia has stated there is no exposure to Russia for their products. In a recent SEC filing, the company stated: The Company’s outlook for its third fiscal quarter provided on August 24, 2022 included approximately $400 million in potential sales to China which may be subject to the new license requirement if customers do not want to purchase the Company’s alternative product offerings or if the USG does not grant licenses in a timely manner or denies licenses to significant customers.

At this time, Nvidia has applied for an exemption and there has also been a clarification that Nvidia can continue to develop the H100 in China through September 1, 2023 through the company’s Hong Kong facility.

Per the SEC Filing dated August 31, 2022:

The U.S. government has authorized exports, reexports, and in-country transfers needed to continue NVIDIA Corporation’s, or the Company’s, development of H100 integrated circuits after the Company filed its Current Report on Form 8-K with the U.S. Securities and Exchange Commission on August 31, 2022. The authorization also allows the Company to perform exports needed to provide support for U.S. customers of A100 through March 1, 2023. Additionally, the U.S. government authorized A100 and H100 order fulfillment and logistics through the Company’s Hong Kong facility through September 1, 2023.

Some analysts have stated that being granted an exemption is “feasible.” Mark Lipacis of Jefferies is modeling for a $200 million hit to October rather than the $400 million identified risk. Harlan Sur of JP Morgan noted AMD is working on getting export licenses for its customers and helping them transition to products that fall below the performance threshold to help mitigate the downside risk.

According to a new report, Nvidia has asked TSMC to rush high-end GPU orders before the US sanctions begin. The report says that TSMC has a special program to speed delivery of orders at a higher negotiated price and can help to cut the delivery time in half. This could lead to a surprise bump in Q4 revenue for the company.

Conclusion

Nvidia is not the same company that it was four years ago. In 2018, Nvidia was a gaming company with promising AI tailwinds. Today, Nvidia’s AI products serve nearly every enterprise company’s artificial intelligence and machine learning ambitions.

The company has an impressive launch schedule starting in October for two flagship products – the RTX 40 Series and the H100 GPU. The timing of these releases is no coincidence as it’s a rapid two months following the crypto/gaming revenue miss. Suffice to say, Nvidia’s management team is prepared to rumble —- putting its very best release in gaming and its most powerful AI chip to-date up against the crypto mining selloff. If history is any indication, the turnaround will only be a matter of time.

Please note: The I/O Fund conducts research and draws conclusions for the company’s portfolio. We then share that information with our readers and offer real-time trade notifications. This is not a guarantee of a stock’s performance and it is not financial advice. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis. Beth Kindig and the I/O Fund own shares in NVDA at the time of writing and may own stocks pictured in the charts.

Snap has a rock bottom valuation of 4 P/S and the stock has not traded here in the entirety of its public market history.

In fact, this is nearly 50% lower than the March 2020 Covid low when it traded at 7 P/S. The Covid March low matches the previous low from Q4 2018.

I believe Snap is oversold and we hope to capture this opportunity.

Q2 2022 Earnings

As long as the FED is raising rates, then the primary reason to close a position will be due to a company’s declining cash profile and/or declining margins. Snap provided a shocking report on the bottom line in Q2 and we had no choice but to exit and regroup.

We covered this briefly here when we said: “The other negative to Snap’s report included more losses on the bottom line. Free cash flow is at ($147) million in the most recent quarter. Adjusted EBITDA fell from +$117 million to +$7 million. GAAP net losses went from ($152) million to ($422) million.”

Some of this is driven by the company’s generous stock-based compensation which totaled $1.2 billion over the trailing twelve months, or about $300 million per quarter. That’s 50% of the company’s gross profit.

There was a $500 million stock repurchase announcement in July with 3% of outstanding shares purchased as of August 31. This helps to offset SBC dilution.

However, there is new information regarding Snap’s bottom line as of August 31 and September 6th:

In August, Snap announced a 20% reduction in work force and will reduce operating expenses through restructuring its products to cut back on Other Bets, such as drones and Originals.

This will result in a $500 million operating expense reduction relative to Q2 2022 which includes $50 million from content costs and $450 million from personnel and opex cost reductions. Of the total $110 to $175 million in transition costs, the majority will be reflected in Q3 2022 with $95 million to $135 million incurred as an adjusted operating expense.

Snap stated this will result in “adjusted EBITDA and positive free cash flow at current revenue levels” which will “drive meaningful operating leverage when revenue growth accelerates.”

One week later, there was an additional leaked memo on September 6th where the CEO stated his 2023 goals are for $6 billion in revenue, adjusted EBITDA above $1.5B and free cash flow above $1 billion. This would represent 20% growth on the top line. The memo also pointed toward 30% growth in DAU to 450M, up from the 352M the company reported last quarter.

My interpretation is that DAU will outpace revenue growth because DAU growth will come from Rest of World where users are monetized at a lower rate than North America and Europe. This has been the trend over the past year in Snap’s key metrics.

Of the $6 billion in estimated revenue for 2023, Snapchat+ will contribute $350 million in revenue next year. The premium subscription currently has 1 million subscribers and is expected to reach 4 million by the end of 2022.

Following the announcement, analyst Mark Mahaney stated he is modeling an EBITDA margin of 17% for FY2023 up from 9% in FY2022.

“Evercore ISI analyst Mark Mahaney raised the firm's price target on Snap to $17 from $14 and keeps an In Line rating on the shares as he is "modestly increasing" his FY22-FY23 revenue estimates and also raising his EBITDA estimates following the company's intra-quarter update on August 31. He is now modeling a meaningful EBITDA margin expansion to 17% next year from his estimate of 9% margin in FY22, driven by cost reduction initiatives and scaling of the business, Mahaney noted.”

Morgan Stanley is in line with Mark Mahaney with a 9% margin this year to $670 million and $919 million for FY2023.

“Morgan Stanley analyst Brian Nowak raised the firm's price target on Snap to $10 from $8 following Snap's recent better than expected August ad update and announcement of a $500M cost reduction plan. Nowak has raised his FY22 and FY23 revenue estimates by 9% and EBITDA forecasts to $670M and $919M, respectively, but keeps an Underweight rating citing low near-term visibility and still-high execution risk.”

That would put Snap back on track for a H2 profile similar to 2021 for adjusted EBITDA of about $118 million in Q3 and $229 million in Q4. I’m basing this off 2021 when Q4 was roughly 2X the profitability of Q3.

Perhaps most importantly, if Snap does achieve the $6 billion, then Mark Mahaney is modeling $1 billion in adjusted EBITDA. In 2021, Snap had adjusted EBITDA of $617 million. If we go with $1 billion conservatively and $1.5 billion for a high estimate per the leaked memo, then this will be 1.5X-2X adjusted EBITDA in 2023 compared to 2021.

Overall, there has been a rapid turnaround in 30-day analyst EPS revisions that show Snap as the leading stock in the tech universe for 72K% change on the bottom line for FY2022.

What this means is that instead of Snap reporting ($0.09) EPS, the company is now expected to report $0.05 EPS.

The estimates for FY2023 are at $0.33 EPS, up from $0.16 EPS for FY2023 consensus before the announcement.

Regarding free cash flow, to put this in perspective, the company had negative FCF of negative ($147) million last quarter. The company will now be positive $1 billion in FCF for FY2023 compared to FCF of $126 million in FY2021. That’s a 8X improvement in two years. Assuming this happens, Snap is guiding for a remarkable turnaround in the cash profile of the company — which is the reason we are attracted to the stock once again.

Notably, it was not only Netflix’s entry into CTV ads that made the stock attractive in July/August, but the improving free cash flow guide from 2022 to 2023.

When the headcount reduction was announced, the CEO also disclosed that Snap was losing two of its top ad executives to Netflix. This is seen as a negative yet we are also keen on the Netflix opportunity and imagine the executives see what we see, which is global streaming juggernaut + CTV ads = (likely) a new trajectory.

The CTV ad opportunity is our top trend in media but we also like Snap at this valuation (both things are true). Snap’s audience is especially interesting for advertisers, but ultimately, product takes a back seat when there is a hawkish Fed. As we are seeing with MongoDB, the cash margin is too critical right now to move from a positive FCF to a negative FCF.

Revenue Growth and DAUs:

In a rising rate environment where cash is rerated with each Fed announcement, the bottom line is arguably more important than the top line (within reason). If Snap had not provided a significant improvement to the bottom line, then we would not be re-evaluating the stock.

Regarding the top line, Snap stated in the Investor Update on August 31st that “quarter to date” they are tracking 8% revenue growth for Q3.

What the CEO said in the September 6th memo regarding inflation and how he looks at revenue growth is important so I’ve pasted it verbatim here:

“In this inflationary environment, we need to adjust the way that we think about our revenue growth. With the U.S. Consumer Price Index at 8.5% growth year-over-year in July, and our Q3 QTD nominal revenue growth rate disclosed on August 31st at 8%, our revenue is growing -0.5% in real terms.

In short, if we are growing revenue below the rate of inflation, our business is actually shrinking. Meta’s revenue, in real terms, shrunk by nearly 10% in Q2, while our Q2 revenue grew approximately 4% in real terms. As we think about our revenue goals for next year, we need to consider the rate of inflation and factor it into our ambitions.

Our goal for 2023 is $6 billion in revenue, of which we will generate $5.65 billion of advertising revenue, and $350 million of revenue from Snapchat+.

Assuming that $5.65 billion of advertising revenue represents approximately 20% growth year-over-year, and assuming an 8% inflation rate, we would be generating approximately 12% year-over-year inflation-adjusted advertising revenue growth.

That’s a far cry from the 50%+ year-over-year average annual revenue growth we’ve generated over the past five years, but we believe it’s an appropriate goal in this environment. If we can generate $6 billion in revenue in 2023, we should be able to generate at least $1.5 billion in Adj. EBITDA and $1 billion of free cash flow.”

I believe the market has not moved much on this news because it requires a Q3 report and a Q4 guide to show if there’s any near-term acceleration from the paltry 8% growth. Essentially, the market will be looking for a sign that September was stronger than August. There is risk it September won’t be stronger than August and/or Q4 won’t be stronger than Q3, yet I/O Fund is subjectively comfortable with the risk as I believe the 4 P/S valuation is pricing in the worst case scenario.

We need DAU to remain strong, but judging by the CEO’s comments, that shouldn’t be a problem as the company provided the forecast of 35% growth over the next 18 months when the CEO said in the memo the goal was to: “Increase Daily Active Users to 450 million in Q4 ’23.” This is up from 352 million DAU in Q2.

Risks:

Snap’s management has struggled to provide accurate guidance in H2 2021 and H1 2022. This twelve-month period has seen (40%) drops in price and +58% gains in price in one day.

This is a volatile stock particularly because management’s guidance has been wrong. We have to take that into consideration when relying on management’s guidance for H2 2022 and FY2023. Morgan Stanley called it “execution risk” when referring to CEO Spiegel’s inability to guide correctly and navigate the many headwinds his company faces.

However, institutional analysts agree with the bottom line and the improvements that $500 million reduction in opex will lead to, including those that are underweight, so that’s helpful. The 8% revenue growth seems reasonable and not an over-promise compared to the 50% revenue growth that had been provided in 2021.

There is a risk that DAU misses as the 35% growth over 18 months is a strong guide.

The stock based compensation is high and viewed as a negative in this macro environment. This weighs on GAAP operating margin.

Conclusion:

Our decision to look for an entry is based on the stronger bottom line, the anticipated full 8X growth in FCF over two years coupled with a rock bottom valuation.

This article was originally published on Forbes on Sep 16, 2022,03:24pm EDTForbes on Sep 16, 2022,03:24pm EDT

Last June, we discussed key reasons that cybersecurity stocks would hold up particularly well compared to other cloud verticals. The analysis pointed to enterprise spending expected to increase in 2022 from the previous year, according to Chief Information Security Officer (CISO) surveys.

Considering the level of cloud spending in both 2020 and 2021, an increase on already high budgets is impressive. The CISO surveys state that 44% will increase budgets in 2022 compared to 41% in 2021 and only 2% are expect to decrease compared to 6% the previous year.

In a similar study from PricewatershouseCooper, 69% predict a rise in cyber spending for 2022 and 26% expect a surge of 10% or higher spending year-over-year. This survey was done across a broader C-suite and executive sampling.

Our analysis in June also pointed out that according to a Gartner survey, 88% of the Board of Directors viewed cybersecurity as a business risk. According to Paul Proctor, VP at Gartner, “The influx of ransomware and supply chain attacks seen throughout 2021, many of which targeted operation- and mission-critical environments, should be a wake-up call that security is a business issue, and not just another problem for IT to solve.”

We had also stated on Fox Business News that a small cohort of companies emerged this past quarter to increase the top line while also reporting narrowing losses on the bottom line. We feel not losing site of opportunities during selloffs is how generational wealth is built.

Sign up for I/O Fund's free newsletter with gains of up to 403% – Click hereSign up for I/O Fund's free newsletter with gains of up to 403% – Click hereClick here

Cybersecurity Stocks Report Another Strong Quarter in 2022

In Q2, cybersecurity stocks did not disappoint with revenue beats across the board. Although SentinelOne had the largest revenue beat, Crowdstrike had the largest beat from a higher revenue base.

Source: YCHARTS

We pointed out on Twitter that one reason for the strong beats is that cybersecurity is not subject to discretionary spending.

Source: Beth Kindig

Sign up for I/O Fund's free newsletter with gains of up to 403% – Click hereSign up for I/O Fund's free newsletter with gains of up to 403% – Click hereClick here

Palo Alto Networks and Crowdstrike have strong bottom lines and this is one reason both stocks have outperformed the Nasdaq this year. With that said, high growth is starting to gain traction again as SentinelOne and Zscaler have the stronger price action in the last 30 days.

Source: YCHART

In the chart below, we see a handful of cybersecurity stocks have been able to grow free cash flow, such as Crowdstrike, Zscaler and Palo Alto Networks. The strong free cash flow is occurring in addition to growing the top line, which indicates cybersecurity is not a “growth at all costs” industry.

Source: CHARTS AND INVESTOR RELATIONS

Conclusion:

Cybersecurity continues to be a top priority in budgets and the results are showing up again in Q2. We found a strong pattern with cybersecurity stocks sustaining growth rates and strong bottom lines in Q1 and also in Q2. The cybersecurity sector overwhelmingly beat estimates compared to other sectors within tech and investors should take notice of this strength.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

We’d like to discuss a few stocks that are showing strong price action in the solar industry. Perhaps the most obvious front runner in clean energy right now is Enphase. The most recent quarter was exceptional as the company reported improving top line growth and an improving bottom line. The company also provided a strong guide for accelerating revenue (again).

Please reference our free analysis on The Inflation Reduction Act of 2022 and Europe's Energy Crisis here.

An important standout accomplishment from Enphase has been management’s ability to reliably meet its revenue guidance for fifteen quarters since its last miss in September of 2018.

The same is true on the bottom line with fourteen consecutive beats since Dec of 2018.

To have met guidance for 4 years is no small feat considering we’ve been through a pandemic and had ongoing supply disruptions that has directly impacted the solar industry. Given the many variables we’ve seen in the last four years, this is the only company that I recollect accomplishing this. Certainly, it instills confidence that management will meet/beat moving forward compared to its lumpy solar industry peers.

Enphase reported Q2 growth of 68% for revenue of $530 million. This is up from revenue growth of 46% last quarter. Guidance is for revenue growth of 75% for Q3 to $613 million and analysts are expecting 60% growth in Q4 to $664 million.

The company also provided the following on the call: “We shipped approximately 1,213 megawatt DC of microinverters and 132.4 million megawatt hours of IQ Batteries in a quarter” with the company guiding for 130 to 145 megawatt of IQ batteries in Q3. This is up from 120 megawatt hours in Q1.

Microinverters shipped were up 39.7% which marks an acceleration from the 15.7% year-over-year change in Q1. This is down from the peak of 117.2% in Q2 2021 but it’s also a boon that Enphase delivered this growth on top of the hard comp.

In the United States, the revenue increased 15% sequentially and 66% year-over-year. Europe revenue grew 89% year-over-year and 69% sequentially.

Right now, fiscal year revenue is slightly decelerating from 78% growth in FY2021 to 63% expected growth for FY2022.

Management stated they’ve grown IQ battery shipments by 28% per quarter over the last two years in North America and are now introducing these batteries into Europe.

Gross margin is a tick higher than it’s been in the most recent quarters at 41% compared to 40% in FY2021. Gross margin guide was for a range between 38% to 41%. The gross margin is expected to improve when IQ8 reaches scale.

Operating margin expanded to 17% in Q2, up from 14% in the previous quarter and up from 15% in FY2021. Net margin is improving, as well, at 14.5% up from 12% last quarter and 10.5% in FY2021.

Enphase saw a sizable increase in operating cash flow to $201 million, up from $102 million in the previous quarter.

The margin of 38% is nearly double what it’s been in previous quarters. Free cash flow also doubled to $192 million, up from $90 million in Q1. This is 2/3 of the cash flow from all of FY2021, which was at $300 million for the year. This increase was due to higher revenue and an improved cash conversion cycle in Q2.

GAAP EPS is at $0.54 compared to $0.28 in the year ago quarter. Adjusted EPS is at $1.07 compared to $0.53 adjusted EPS in the year ago quarter.

With that said, Enphase has a debt to cash ratio of 1:1. This reflects cash and marketable securities of $1.25 billion and debt of $1.29 billion. Given the current cash profile of the company, this should improve but does need to be monitored.

Note on Valuation

Enphase is not the easiest entry when it comes to valuation. The stock had a blowoff top moment in November of 2021. This aside, the stock is not reliable where it’s currently trading with little success of trading above this top line valuation. In a perfect world, we would find an entry around 10-12 forward P/S or 15 current P/S. That may seem like wishful thinking yet we want to be prudent as solar can be volatile.

Given the strength of the earnings report, we are trading at the stock’s highest valuation on a forward PE ratio in 2022 of 70. Previously, a forward P/E of 50-55 was the top for this stock in 2022. In other words, we will need another blowoff November top to see gains from here, if history is any indication. OR, Enphase will need to start a new valuation trajectory which is risky to predict without more data to support this conclusion.

Product Overview: IQ8 Inverters

Enphase has six models of microinverters in the IQ8 line, which are popular for their performance during a grid outage. Due to IQ System Controllers and IQ Load controllers, the system can sustain off grid. What is unique about the IQ8 is that the system will continue to perform off-grid even without a battery although the battery option is also popular.

The IQ8 Microinverter offers a microgrid with split-phase power conversion that converts DC power to AC power. Because solar panels only produce DC power, inverters are necessary to convert this to alternating current (AC), which is the current that houses use for energy needs. The DC to AC conversion and solar output is performed through the IQ8 and is done off-grid.

The System Controller or “smart switch” connects the home to the grid power, batteries and the solar photovoltaics, and transitions the system from grid power to backup power. The Load Controller sheds non-essential loads to offer longer off-grid power. The IQ battery offers up to 10kWh of energy capacity, so rather than feeding power back to the grid, the system stores the back-up power for future use.

Notably, the system is modular so a home owner can start small and build a bigger system over time. The system also does not require a battery for off-grid power, and thus, the IQ8 can be more cost effective for entry-level systems. The IQ8 is not compatible to existing systems, however, so it’s only available for new installs.

The secret sauce for the IQ8 Inverters is a customized, proprietary ASIC chip that can quickly change loads and grid events, which ultimately reduces the required battery sizing and battery power. The system adjusts according to the amount of electricity it has access to and this brain or intelligence is helpful when a system is off grid either temporarily or permanently. It also helps to store more energy by knowing when a house has excess power.

Another key feature is the microinverters come with a 25-year warranty and the battery has a 10-year warranty. My understanding is this is an industry-leading warranty, which is key for this level of home or commercial investment.

The IQ8 was first tested in Australia in 2017 due to “anti-islanding” which refers to grid-connected inverters that must shut down when there is a loss of electricity supply from the grid. The reason for shutting down the inverters is to protect the power line workers who are restoring the system. The solution that Enphase designed were the IQ8 models which are “always on” by combining the inverters, batteries, system controllers and load controllers listed above for a mini grid that can produce power from the sun and efficiently store this power at night.

Although California comes to mind for a region that shuts down its grid frequently due to wind storms to prevent fires, or perhaps Texas during the ice storm, this is also in demand globally where there are weak grids (Latin America) or no grid (Africa and parts of India). The company has cited in the past that there are 1.2 billion people who can benefit from the IQ8 due to persistent and permanent grid issues. The company’s current revenue mix is 80% United States and 20% international.

To understand how impactful the IQ8 has been for Enphase, consider that right now it comprises 37% of the company’s shipments and Enphase management expects this to reach 90% by Q2 2023. That is a lot of growth for one product in four quarters’ time.

IQ8 Inverter and IQ8 Batteries Discussions on the Earnings Calls

When asked on the call why the IQ8 system is performing well compared to competitors, the CEO responded:

“Yes, I mean we IQ8 provides a lot of value. Three things is sunlight, backup. Basically, when the grid is out, IQ8 continues to work and provides power, one; number two, it removes any limit on solar to storage ratio, which is the limit of today. In other words, you can have a lot of solar with very tiny storage, and the extreme end being zero storage, that's number two.

Number three is sunlight jumpstart, which means that in other batteries when you completely drain the battery, because you use it overnight, and you accidentally drained it, you accidentally drained it in the morning, IQ8 can come and independently jumpstart the batteries. Because it can provide — it can generate its own microgrid and kickstart the battery.”

Here was another lucid moment on the call when management described why they’re pulling ahead:

“We are trying — we have with the home energy management solution that we have, we are providing a very comprehensive solution. This is not just about the solar part, not just about the battery part or just about the EV part or managing the heat pump, etcetera. Our goal is to provide a one stop shop, a completely comprehensive solution. And everything is managed from software with a home energy management system. This is true in Europe. And actually, it's true here as well.

So for us, our value-add when we think about relative to competition is not look at any one single piece. Although we have to be better than them in every individual component that we are building. But it is about looking at the overall solution. So the homeowner has a great experience where they have one app, and they see they get unprecedented visibility into the performance of their entire system.”

IQ8 battery shipments grew 28% per quarter over the past two years. The company is releasing a third generation in early 2023. According to the earnings call, this battery will “deliver double the power enabling homeowners to start heavy loads.” The release is slightly delayed due to increasing the AC Power of the microinverter following feedback.

The company stated they currently have manufacturing capabilities of 5 million microinverters and will soon have a 6 million capacity after expanding manufacturing to Romania. Enphase is expanding rapidly into Europe including the IQ batteries after launching the IQ batteries two years ago in North America.