This article was originally published on Forbes on Jan 27, 2023,12:17am ESTForbes on Jan 27, 2023,12:17am EST

Ad-tech stocks across the board had a tough year last year. Investors are hoping that 2023 will be a better year, yet according to the projected ad spend for 2023, this may not be the case.

It’s clear that lower ad budgets in 2022 affected nearly every ad-tech stock, including companies that own large audiences, such as Alphabet and Meta. It did not matter if an advertising company has audiences as large as 2 billion or more, runs large R&D departments that can leverage AI, or is centered in the leading media growth trend of connected TV (CTV) ads. Broadly speaking, because ad spend budgets were slashed on a year-over-year basis, this one, single headwind caused 50% to 80% selloffs across the advertising industry. Therefore, it’s prudent to look at whether ad-tech budgets will increase this year or if 2023 will look more like 2022 in terms of top line growth.

Here’s What Happened to Advertising Stocks in 2022

The stock market of 2022 was hectic, and the blowoff top in 2021 is primarily blamed for this. However, irrespective of the stock market’s performance in 2021, the global economy and the United States economy is in a slowing growth environment.

Here is a quote from Insider Intelligence published in November:

“Total digital ad spending worldwide will not grow as robustly over the next two years as we expected in our Q1 forecast. We now project 2022 digital ad spending worldwide to reach $567.49 billion, up 8.6% over 2021. In our previous forecast, we expected 15.6% growth to $602.25 billion. Our Q1 forecast predicted digital ad spending worldwide would reach $756.47 billion by 2024, but we now expect it to reach only $695.96 billion.

The key words here are “will not grow as robustly as we expected.” Stock investors get trapped when growth slows and forecasts come down mid-year. This is because not only must stock valuations contend with a growth rate cut in half (8.6% versus 15.6%) — but analysts must also try and figure out when a bottom will form on the slowing growth. Most will lean conservative, which pushes valuations down even further.

GroupM also lowered their forecast for 2022, from 8.4% to 6.5% (excluding US political advertising), and pure play digital advertising was cut from 11.5% to 9.3%.

Sign up for I/O Fund's free newsletter with gains of up to 221% – Click hereClick hereClick here

What to Expect for Ad Spend in 2023

According to the sources noted above, 2023 will not be the year of recovery for ad budgets. As of now, growth is expected to be lower than 2022.

Magna predicts that global advertising revenue will grow to $833 billion in 2023, or about 5% year over year, compared to 7% in 2022. GroupM is projecting 5.9% growth, or $856 billion in 2023 (excluding US political advertising), compared to 6.5% in 2022 (excluding US political advertising). Both of these 2023 estimates reflect downward revisions of 1.5% and 0.5%, respectively. Including US political advertising GroupM is projecting 7.8% for 2022 and 4.6% in 2023.

Source: Company Websites

According to Insider Intelligence, China will weigh heavily on 2023 numbers as the second-biggest digital ad market is expected to “post its lowest digital ad growth on record” due to “tougher regulations and economic headwinds.”

According to IAB, the U.S. advertisement market is expected to grow by 5.9% in 2023, which is lower than the 9% growth seen in 2022. The slowdown in growth is the direct result of the challenging macro environment.

On a brighter note, the CTV market is expected to grow 14.4% in 2023 and will grow faster than the overall advertisement market. They forecast Linear TV spending to see a drop of (6.3%). Across the advertising channels, digital video, including CTV, is expected to have the highest share of 22.4%, up from 19.3% in 2022.

There are also positive comments from other ad-tech companies on CTV. Hunain Khan, Director, Programmatic CTV supply at Xandr said, “2023 marks a new age of CTV, due to the increased amount of available premium inventory through AVOD platforms.”

Similarly, Hitesh Bhat, Director, CTV/OTT, EMEA at PubMatic said, “2023 will be an interesting year for CTV in Europe, but I’m avoiding “the year of CTV’ hyperbole. The ad-funded opportunity will grow significantly with the entrance of huge players such as Netflix, Disney+, Paramount+ and the combined HBO/Discovery+ offering. I think Netflix and Disney will be careful in terms of ad loads, so as not to annoy viewers who are still also subscribers.

The Dentsu ad spending report forecasts that global advertising spending in 2023 to increase by 3.8% YoY to $740.9 billion. It is lower than the 8% expected growth for 2022 and the 19.6% growth reported in 2021. The forecasts have been slashed from the July report, which projected a growth of 5.4% for 2023. Some of the reasons mentioned in the report for the slowdown include rising inflation, interest rates, recessions, and political uncertainty. The report suggests that if we exclude the media price inflation, ad spending is forecasted to drop (0.6%) in 2023.

The Americas region is expected to grow 3.7% YoY to $339.1 billion, the EMEA region to grow 3.8% YoY to $156.7 billion, and Asia Pacific is forecasted to grow 4% to $245.1 billion.

Digital ad spending is expected to grow 7.2% YoY to $422.8 billion. It is down from 13.7% expected growth in 2022. Digital ad spending accounted for 57.1% of all advertising spending in 2023. The share is expected to increase to 59.5% in 2025.

According to Insider Intelligence, digital ad spending is expected to grow 10.5% in 2023 from the expected 8.6% in 2022, both of these estimates reflect downward revisions of 2.6% and 7%, respectively.

The CMO survey done in September 2022 showed that the marketing spending increased by 10.4% in the previous one year for marketers. However, they predict that the growth will slow down in the next one year to 8.8% and will start trending toward the pre-Covid level of 5.8%.

A majority of the companies say that the inflationary pressures are decreasing marketing spending levels. Marketing leaders in large companies report marketing spending reduction due to inflation and on the other hand, marketers in the smallest companies report an increase in marketing spending. The survey also suggests that the marketing expenses as a percentage of total revenue have reverted to the pre-Covid levels, as seen in the below chart. It reached a high of 13.2% in February 2021 to 8.7% as per the September 2022 survey.

Source: CMO SEPTEMBER 2022 SURVEY

The I/O Fund has launched a new $99/year Premium Newsletter called "Essentials" — this newsletter delivers premium samples for our readers who want more actionable analysis for their tech portfolios. This month, we released a stock pick that we believe will be a leader in 2023 plus a video with the buy plan.$99/year Premium Newsletter called "Essentials" — this newsletter delivers premium samples for our readers who want more actionable analysis for their tech portfolios. This month, we released a stock pick that we believe will be a leader in 2023 plus a video with the buy plan.

Google May Be the Stronger Ad-Tech Company in 2023

According to analyst consensus, Google is expected to generate $168.44 billion in net digital ad revenues worldwide this year, down from Q1 expectation of $174.81 billion. By 2024, Google’s ad business will reach $201.05 billion—or 2.8% below the Q1 expectation.

“Google has an edge over its other ad-reliant competitors in an economic downturn, as advertisers facing budget cuts typically prioritize lower-funnel channels with higher ROI like search,” said Evelyn Mitchell, analyst at Insider Intelligence. “Search has also retained full functionality in the wake of Apple’s privacy changes. Search ads are served in response to a user query and don’t usually leverage data about that user, so they’re less affected when iOS users opt out of being tracked. Meanwhile, social media advertising relies more heavily on consumer data.”

Source: EMARKETER/INSIDER INTELLIGENCE, NOVEMBER 2021

Source: EMARKETER/INSIDER INTELLIGENCE, APRIL 2022

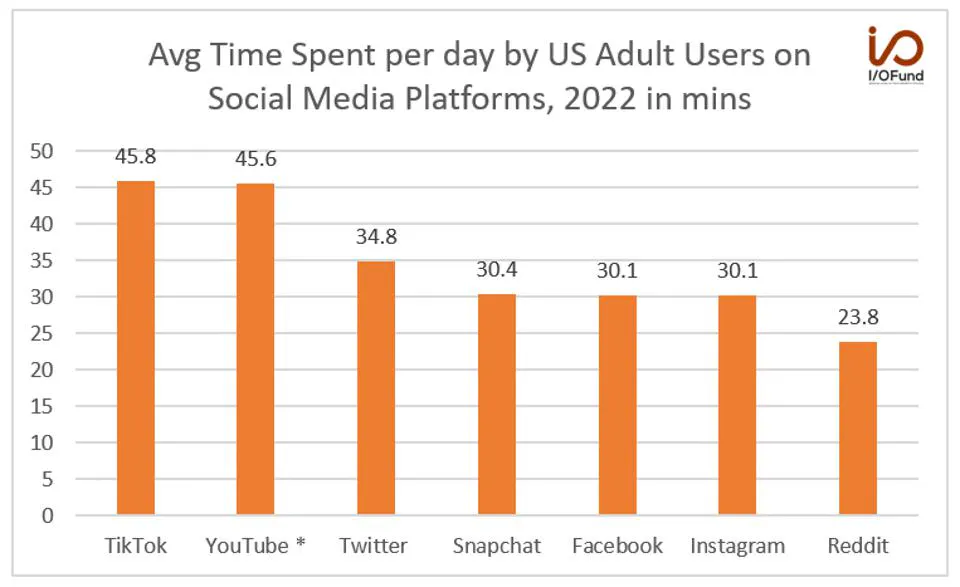

The above two studies from Insider Intelligence show that Facebook and Instagram have the highest number of social media network users in the US. However, these platforms have lost the top spots in terms of engagement as TikTok and YouTube has the highest daily time spent by the users. Due to higher engagement, these platforms are likely to do better for social media advertising makes more sense.

On that note, Insider Intelligence expects Meta to generate $112.68 billion in digital ad revenue for the year 2022, representing a YoY drop of 2%, which is down significantly from the Q1 forecast of $129.16 billion. The firm has lowered the forecast for Meta through 2024 by nearly 20% citing Instagram’s ad revenue to grow by 2.6% YoY to $43.28 billion compared to a 50.2% growth in 2021. The estimate is significantly lower than the Q1 forecast of $54.16 billion. They expect Instagram revenue to reach $59.61 billion by 2024, which is more than 27% lower than the Q1 projection.

Below, Lead Tech Analyst Beth Kindig covers why Meta’s lack of access to third-party data spells trouble for its future growth. This webinar was recorded in April of 2022 yet is still relevant today.

Snapchat ad revenues are also negatively impacted by the economic slowdown. Insider Intelligence has slashed the 2022 ad revenue estimates by 18.3% from their Q1 forecast. They have also reduced the 2024 ad revenue by 33.6% from their Q1 estimates.

The TikTok Threat is Real

Insider Intelligence expects TikTok’s global ad revenue in 2022 to grow 155% YoY to $9.89 billion, below its Q1 estimates of $11.64 billion. They expect TikTok ad revenue to grow 36.7% in the next two years to reach $18.49 billion. However, the 2024 forecast has been by lowered by 21.6% from their Q1 estimates. Jasmine Enberg, the principal analyst at Insider Intelligence, said, “TikTok has transformed from an experimental play to a must-buy for many advertisers,” She further said, “But TikTok isn’t immune to the macroeconomic challenges causing advertisers to trim their overall digital ad budgets. Meanwhile, growing anti-TikTok sentiment among media executives and renewed calls by government officials to ban the platform are causing some advertisers to be more cautious about their spending there.”

According to the Sensor Tower report, social channels accounted for 61% of US digital ad spending in Q3 2022. The US digital ad spending is strong as it grew 5% quarter-over-quarter to $23 billion. Facebook leads the top advertisers in the United States. However, TikTok had the highest growth as it grew 29% QoQ and is a threat to other social media channels.

Disney+ increased its advertising spend in TikTok from $3 million in Q1 2022 to $17.9 million in Q3 2022. TikTok has been successful in being popular among the younger generation audience which has attracted marketers to its platform. As per Omdia research TikTok’s ad revenue is expected to exceed Meta and YouTube’s total video ad revenues by 2027.

Other ad-tech trends to watch for 2023

First-party data ownership is gaining popularity. The data is more reliable even though it might be smaller than the third-party data. The quality of the first-party data is superior and helps better understand the customer’s needs. Contextual targeting is another trend to watch. Contextual targeting means that users will see ads relevant to the topic you are watching or reading. Previously, you used to get ads based on browsing history. Contextual targeting might increase the chances of increasing the return on investment as the ads are relevant to the content. There could also be increased use of AI/ML tools in contextual targeting.

Conclusion

The overall advertising market is expected to slow down in 2023. Some of the crucial reasons are rising interest rates, inflation, and slowing global growth. Even though the estimates have been reduced, the digital ad market is expected to fare better than the broader advertising market.

We believe there will be a handful of winners despite more headwinds in 2023 and we cover these winners for our premium research site. However, until ad budgets resume growth, the industry at large is likely to be volatile in stock price.

Royston Roche, Equity Analyst at the I/O Fund, contributed to this article.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.