Micron reported Q2 results that beat estimates and guided for Q3 sales and earnings growth above expectations. However, Micron’s share are off 9% post-earnings, which may be due to commentary around soft demand in China, slowing PC sales and concerns that Micron may be nearing the top of the cycle. We believe that these concerns are temporary, and that Micron is structurally becoming a less cyclical company, which deserves a premium multiple. I discuss the company’s latest results and why we believe the recent sell-off is overdone in more detail below.

Micron’s Q2 FY2022 Beat Expectations and Guidance Was Above Consensus

Micron reported Q2 FY2022 results on March 30th, and sales increased 1% QoQ to $7.8 billion driven by a 4% sequential rise in NAND sales, which accounted for ~25% of total revenues. NAND sales also increased 19% YoY and management expects NAND sales to increase by ~30% YoY for the year. Demand for NAND is being driven by Micron’s new 176-layer NAND technology, which represented the majority of Micron’s NAND shipments. We explained the importance of 176-layer NAND here, stating that Micron has significantly increased memory capacity and is a leader in this technology, allowing the company to capture more market share.

Importantly, the strength in NAND should also be a tailwind for Lam Research, which sells the etching equipment necessary to build the layers for 176-layer NAND. In our latest update on Lam Research, we explained that “the key reason we think Lam could fare better than its peers is because as 3D layers increase, capital intensity also increases. The process does not scale linearly, instead it’s non-linear because it takes longer than 2X to etch a stack that is 2X high and requires more complex etch and deposition equipment”. With Micron guiding for $12 billion in Capex this year and plans for $150 billion in capacity expansions over time, we should expect Lam Research to see strong demand for etching equipment going forward.

Micron’s NAND prices also benefitted from the contamination of ~8% of the global supply of NAND. In February, memory peer Western Digital disclosed that there was a contamination event at two of its Japanese JV facilities, which resulted in 6.5 exabytes of NAND memory being contaminated. Likely benefitting from this event, Micron’s Q2 NAND prices rose ~4% QoQ, driving much of the topline growth as volumes were flat. As shown below, Micron has outperformed relative to Western Digital YTD, however, both companies have underperformed the broader market in 2022. I outline a few reasons for this in more detail below, which we believe are only temporary.

Similar to NAND, DRAM sales increased 2% QoQ and were up 29% YoY to $6 billion, or 73% of total sales. DRAM volumes increased but were offset with a decline in ASPs. Strong demand in datacenter drove the increase in DRAM sales. For example, Micron’s largest segment, Compute and Networking, grew sales 31% YoY to $4 billion, driven by a 60% YoY rise in data center sales which were “supported by robust demand across our DRAM and SSD portfolio” (Q2 call, 03/30/22). DRAM sales benefitted from Micron’s leading 1-alpha technology which is increasingly being adopted in the memory-intensive cloud environment. During the Q2 call, CEO Sanjay Mehrotra stated that DRAM sales will continue to ramp into 2023 when he said that “We have broadened the qualifications for our 1-alpha DRAM products and are well positioned to support the data center DDR5 transition driven by new CPU platforms, which are targeted to begin ramping later this calendar year and gain momentum in 2023”.

Following the strength in cloud sales, Storage sales increased 38% YoY to $1 billion as SSDs continue to replace HDDs, while Embedded sales increased 37% YoY driven by strength in automotive. A blemish was weakness in Mobile sales, which increased just 4% YoY to $1.9 billion. While the rollout of 5G phones will lead to a ramp in memory content per phone, there may be demand headwinds on the horizon. For instance, Apple cut its forecast of 5G iPhone shipments by ~20%. I discuss this in more detail below.

Continuing down the income statement, gross margin increased by 2,100 bps YoY and 100 bps QoQ to 47%, benefitting from higher NAND margins and the ramp in 1-alpha DRAM and 176-layer NAND technologies, which reduces costs as it scales. Management noted on the Q2 call that most of the efficiency benefits have been realized, and that margin expansion from the ramp is largely behind the firm. Furthermore, YoY gross margin comps were impacted by a one-time $300 million charge taken last year when Micron switched to FIFO accounting.

The strength in gross margin flowed down to operating profit, which increased 118% YoY to $2.7 billion. The dramatic rise in profitability was driven by higher selling prices and cost reductions from the ramp in new technologies outlined above. However, Micron has historically been a cyclical industry, and there may be concerns that Micron is nearing the top of the cycle. This may explain the recent sell-off in Micron’s sales, yet we believe that Micron is becoming structurally less cyclical and that its multiple will rebound once this is clearly evident in future results (discussed in more detail below).

Finally, GAAP earnings per share were $2.00 while non-GAAP EPS was $2.14, which beat estimates by $0.16. Non-GAAP EPS increased 118% YoY and the strength in EPS growth should continue going forward. For instance, Micron will benefit from a lower tax as Idaho’s governor signed a new tax law on March 16th, 2022 that will reduce Micron’s taxable income (Micron is HQ in Idaho). The CHIPS act may also be a tailwind to earnings as the US government looks to incentivize reshoring of manufacturing capacity.

As of the end of the quarter, Micron had $12 billion in cash and equivalents and free cash flow was over $1 billion during the quarter. Management stated that they expect free cash flow generation will be “substantially higher” over the next two quarters relative to H1 2022. Micron intends to use ~50% of its free cash flow to buy back its stock and pay dividends to shareholders. Since 2019, Micron has reduced its share count by an aggregate 113 million, or by 9%. With Micron guiding for record sales and profits in FY2022, cashflow generation should be significant, which will support more buybacks in the future.

Looking forward, management expects Q3 sales to grow 18% YoY to $8.7 billion, which beat initial topline estimates by 6%. Management stated that they are “tracking ahead” of their initial guide set in Q1 for FY2022 and that demand remains strong, but noted during the Q2 call that “there are some pockets where semiconductor shortages have not improved as fast as we had expected, and these shortages are likely to continue into calendar year 2023”. Nonetheless, Q3 adjusted EPS is expected to grow 14% QoQ to $2.46, which beat initial estimates by 9%.

Potential Risks are only temporary

As discussed above, Micron reported strong top and bottom-line results, guided above consensus and expects to be report record sales and earnings in FY2022. However, despite this, Micron has underperformed in 2022 and is off ~9% since announcing FQ2 results. This may be due to a couple developments: 1) softness in mobile and PC sales and in China, 2) and concerns that Micron may be nearing the top of the cycle.

In regards to the first point, during the Q2 call management stated that “We see some weakness in the China market as the local economy slows, smartphone market share shifts and some customers take a more prudent approach to inventory management.” CEO Mehrotra added that he expects PC unit growth will be “flattish”. These comments may have contributed to a post-ER sell-off, and it is notable that AMD is also off following the Micron Q2 print, likely due to its exposure to PC sales. However, management added further color that enterprise PC sales are expected to be strong in the near term, which are more content rich in terms of DRAM and NAND content, which should offset this pressure.

Moreover, 5G phone sales are just now starting to ramp, but the timing of this ramp remains unknown. As mentioned above, Apple has reportedly cut its production forecasts for its first 5G phone by ~20%. While this may be a near-term headwind, it is inconsequential in the long term. This is because 5G phones will inevitably take share from 4G going forward, and 5G phone DRAM content is 50% higher than 4G, while NAND content is >100%.We expect mobile will be a tailwind going forward, despite the near term uncertainty in the pace of the ramp.

Finally, a trend that is typical with highly cyclical companies is that investors tend to reduce exposure when earnings are high due to concerns that the company may be nearing the top of the cycle. Historically, Micron has been a highly cyclical company with periods of oversupply and rapidly declining prices. However, with more demand drivers coming from data centers/cloud and automotive, memory demand is no longer dependent on the short-cycle PC market.

During the Q2 call, CEO Mehrotra explained that over 75% of its quarterly volume are under long-term agreements (LTA) that go out beyond four quarters or more, up from less than 25% in prior years. CEO Mehrotra added that all of the company’s large customers are now under LTAs, which helps improve demand visibility and reduces uncertainty. An increase in LTAs significantly reduces the cyclicality of Micron’s business.

Moreover, new trends on the horizon further smooth demand for memory, reducing Micron’s dependence on the short-cycle PC market. For example, CEO Mehrotra stated that “new EVs are becoming like data center on wheels, and we expect over 100 new EV models to launch worldwide in this calendar year alone”. The memory content in higher end EVs is 15x higher than the average car, which further reduces the cyclical nature of Micron’s business.

As shown below, Micron trades at a 9x PE multiple, which is below where it was trading in 2017 and well below its multiple in 2020 and 2021. We believe that the market remains in a “wait and see” mode until Micron can prove that it is less cyclical. If Micron can prove that it is less cyclical going forward, we should expect a re-rating of its multiple going forward. A trend that supports this is the reduction in finished goods, which declined QoQ despite the softness in China, PC and mobile. A build in finished goods inventory would signal that demand may be weakening, a trend we have yet to observe in the memory market.

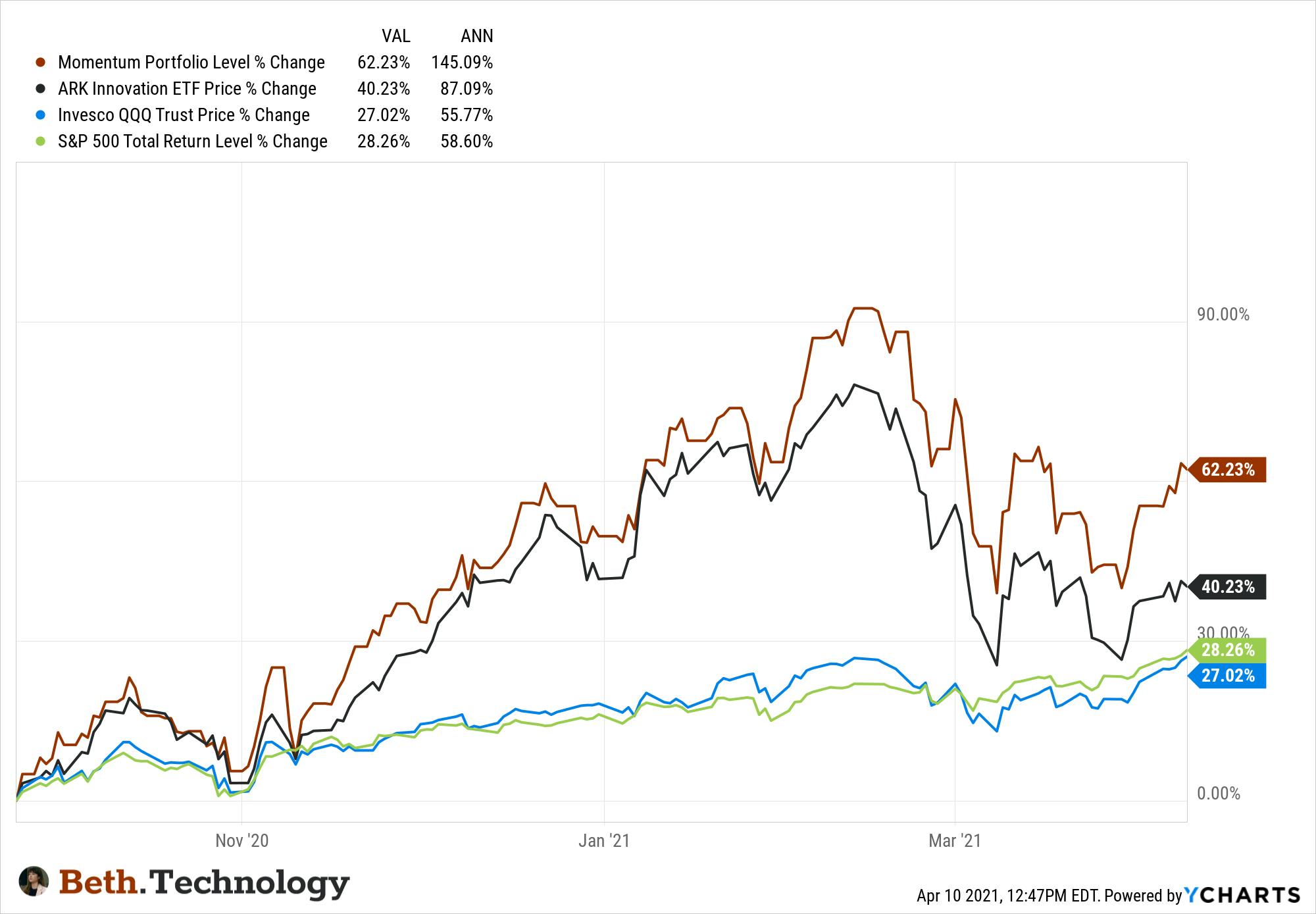

Going into February of 2021, we warned of a selloff based on weakening momentum trending into an important broad market time factor. We used this opportunity to raise some cash and even had a proactive hedge on QQQ at the time. This shift helped us remain competitive with the pros in the growth markets, as did our proactive move out of crypto (and back in again). Even when the growth selloff intensified into late Q1, many were calling for the end of the bull market, as we used that opportunity to add to some quality companies that were getting beaten up. Like many, we underestimated the difficulty in the high beta market, showing mixed results in our additions to high conviction/long-term plays, but we continued to hold the broader thesis that the bull market is not over, as we do today. I do believe we will see a return to 2020-style growth investing before this great bull market is over, but I also believe that we will get a chance to grab shares of targeted companies at lower prices first.

That being said, what I do want to point out is the difference between February 2021 and today. The economic environment tends to lend itself towards high beta being in favor or out of favor. Coming out of the 2020 bear market, we saw a large acceleration of economic growth with low inflation – ie, the perfect environment for our world. As inflation picked up in mid Q1 of 2021, growth investing became more difficult. We still saw numerous winners in this field coming out of the February/March selloff, so a more discerning filter really paid off. The reason for this is that we saw inflation and growth accelerating up at the same time. However, today's dip in growth assets and rotation into more deflation protection assets is signaling something different, in my opinion. I believe looking at the growth trends in the macro-environment will help clarify what that is…

First up, we'll look at our economic heat map.

Note the difference between February of 2021 and today. In February, inflation was starting to pick up but wasn't a major concern (according to the bond market). Also, note how we were in the early stages of accelerated growth in the US economy. Now, compare that to today – growth is starting to slow as our models expect the rate of change in this deceleration to start turning soft red in mid-late Q1. With inflation in the red as well, we also are expecting this slowdown to lead to inflation slowing down as well. We are seeing signs of this slowdown globally with China leading the way. Much like we saw a global growth push in 2017, the macro environment is suggesting a global growth slowdown into 2022.

Our quadrant analysis, which measures the Rate of Change of both growth and inflation in the US, is supporting this thesis.

The October data is being uploaded soon, but it will have the Oct. numbers closer to the bottom right quadrant – inflation/stagflation. This is a risk-off macro environment where high beta struggles, and we see a flight to real estate, utilities, staples, long-duration bonds, and very liquid mega-cap growth companies (exactly what has been working over the last month). We do believe this quadrant will take us into the lower left quadrant (deflation) in 2022.

With this in mind, think of the FED's position. They waited too long to raise rates so are under the gun to rush this process in order to have ammo to fight the next deep correction. So, with growth slowing, inflation peaking, and the FED in a rush to tighten conditions for the next reflation attempt, probabilities suggest that risk assets will continue to struggle until a floor is found in the economic slow-down.

But, don't take our word for it, just look what the bond market is saying.

Remember, long-duration yields are controlled by market expectations of growth and inflation (not the FED). As long-duration yields go down, it's signaling the same slow down our models are showing. The spread between the 10-year yield (not affected by FED policy) and 2-year yield (highly affected by Fed policy) has seen the sharpest flattening since 1994.

Interestingly, this also lines up with our Elliott Wave analysis. I have always been amazed at how using Fibonacci/golden ratio analysis on charts tends to predict future outcomes. Anyone that has been with us for a while knows that we've been talking about 2022 being a tough year based on this analysis alone. We now have a combined macro analysis, coupled with inflation and FED policy catching up to what Elliott Wave was predicting over a year ago.

Trends move in 5 waves in the direction of the predominant trend. this is true in all markets and on all time frames. Since March of 2020, the predominant trend is up. We have a clean 1st and 2nd wave in place (in red). In order to complete the minimum targets for the 3rd wave, we need the current trend to move us into the SPX 4900-5200 region. This will lead to the larger 4th wave, which we expect to be between a 10%-15% drawdown in early/mid-2022. We also have two important broad market time factors coming up – Dec 27-Jan 3 and one in late January (I'll narrow down the focus as we approach this). Almost every chart I map is showing the same inflection points.

These time factors are marking inflection points and how the market trends into them will be crucial. Interestingly, they are also lining up with what our models are suggesting – an acceleration of the global economic slowdown in late Q1 (remember, markets are looking into the future, so expect a top prior to the data coming out). Furthermore, if we look at inter-market signals, a similar warning is still present.

Our risk-on and economically sensitive sectors are diverging from the broad market. When we see this pattern, only one of 2 things will happen: (1) either the broad market is leading the risk-on sectors; (2) the risk-on sectors are leading the broad markets. With the preponderance of evidence discussed, we believe 2 is more likely as we push into early 2022.

Why This is Not the End of the Great Bull Market

In one word – liquidity. I've talked about this for several weeks, in various ways. Last week we showed the strange phenomenon that money market funds and the S&P 500 are both close to ATHs, which is one of many examples of the excess liquidity in the markets. This week, we will focus on how the flood of liquidity in the economy is affecting the banking system.

I, for one, do believe the central banking system will go down in history as a monumental failure. However, you have to play the market you are dealt – not the one that you want or think makes more sense. Many pundits have stubbornly ignored this reality, and as a result, missed out on one of the greatest bull markets in US history. That being said, this is a FED-driven, liquidity-fueled bull market, and the drastic actions taken by the FED (and global central banks) during the COVID crash last year is why we are continuing to push higher today.

In 2008, we saw a gradual tightening that ultimately put in motion the GFC. During this time we saw the first run on banks (and money markets) since the turn of the century. The fear was sudden and caused banks to shut the borrowing window for even qualified companies to refinance their debts. As a result, defaults intensified, and only exacerbated the problem. This liquidity/credit crunch was the primary driver behind the pain experienced in the GFC.

Compared to 2007/2008, last year the FED flooded the economy with excess liquidity that was needed by struggling companies to stay afloat. In other words, they guaranteed that a credit crunch would not happen. this lead to the bizarro world of monthly economic data that literally went off the charts in a negative way, while the stock market kept powering higher. As a result, it's hard to look at the current landscape and see any hint of a liquidity crunch. In fact, the opposite seems to be true.

Liquidity in Banks

We tend to see the beginning stages of a liquidity crunch in overnight markets. In other words, if a bank needs additional liquidity to meet their normal business demands, they will borrow this cash from other banks in the overnight markets. If these private banks see trouble on the horizon they tend to not want to participate in overnight loans, pushing the overnight borrowing rate up, and thus making liquidity even harder to come by. This lack of overnight liquidity begins to filter into the banking system and ultimately down into the economy. To combat this free-market phenomenon, the FED created the repurchase agreement program (Repos) to be the lender of last result. In other words, when no private bank wants to take on the counter-party risk of another bank needing cash to operate, the FED steps in.

Prior to the economic slowdowns, we tend to see the FED's repo program tick up, signaling that private banks are not willing to loan into the overnight markets.

Note how these repo agreements preceded major market events. It's a signal that liquidity is drying up, and this removal of liquidity from the market by the banking system is what ultimately crashes the markets.

Now, let's overlay this metric with inflation expectations (10 yr. breakeven rate) as well as economic growth (PMI – manufacturing).

Note how inflation peaked as did economic growth going into these liquidity crunches. What preceded was sharp bear markets in both instances. Now, note the 2011 and 2015 deep correction periods. We had a deceleration in both economic growth and inflation (much like we're projecting going into 2022), but there was no liquidity crunch. The result was either a sharp and quick selloff (2011), or a correction that was more in time than price (2015) before the bull market resumed. It's important to see that we are not in a similar liquidity crunch today. In fact, the opposite seems to be happening.

The FED also has a program designed to address this opposite problem banks can face, and it's called reverse-repo agreements (Reverse-Repos). Banks operate under strict regulations, one of which addresses the maximum amount of cash/credit they are allowed to hold relative to assets. If a bank is close to that limit, it will lend this excess liquidity to other banks for a small overnight rate. However, what happens when most banks are flushed with cash and cannot accept anymore? The FED steps in to be the buyer of last result, exchanging cash for bonds at a minuscule rate.

Today, the reverse repo operation is at record highs.

In other words, the FED is "borrowing" excess cash from banks on a nightly basis. This is what too much liquidity in the banking system looks like. Now, factor in that the FED is STILL adding ~$60 Billion of QE per month on top of the chart above!

So, like 2019 and 2008, the economy is starting to slow as inflation is likely about to peak. However, unlike 2008 and 2019 there is tons of liquidity in the system that has to go somewhere, and with the CPI running at 6.8% and likely to move into the 7% region, money markets and bonds are not very attractive. For this single, yet crucial reason, I see 2022's volatility to be more like 2011/2015 – an extended road bump in a much larger bull market, which we want to prepare our readers for.

Remember, the FED and global governments need inflation. It is literally the only way out of the massive debt obligations taken on by governments, aside from a default. the same problem was seen in the post-war 1940's – large increase in money supply as inflation ran hot for over a decade. This allowed the US government to get out from under their war debts, while the stock market went on a multi-decade bull market. This, I believe, is what the FED is trying to do today – get everyone used to higher inflation, so that the US has a shot of unwinding its debt. So, creating a market crash would not be conducive to this end.

Our Game Plan for 2022 and Beyond

Going back to our Elliott Wave analysis, if we are completing the 4th wave of the larger 3rd wave, that means that we have the final 5th wave to go. If everything moves as planned, which is always a BIG if, we will bottom into late December, and rally hard into the late January time factor, which is targeting the 4900 regions, at a minimum. We also know that we are in a stagflation/inflation style macro environment, which tends to favor mega-cap growth names. The type of mega-cap growth that is working right now is FAANG and semis. Since our recent entries in NVDA and AMD, we are sitting on 60% gains in just under 2 months, as LRCX and MRVL were almost at ATHs while the rest of tech sold off hard. You are seeing where the money is flowing in real-time. We plan to continue to ride this momentum as the SPX makes its minor 5th wave push, focusing on a potential MSFT play and continued adds to our semis.

Regarding high beta, we are trending down into the first-time factor, which, as previously stated, I'm expecting to be a low. This should kick off the final minor 5th wave push. Also, even though we are focusing on mega-caps and semis, I do not think risk assets are being completely left for dead on this push, as of now.

The options market is not as bearish on risk assets now as the popular narrative/Twitter suggests. Note how ARKK is showing negative implied volatility on a 30-day basis based on their recent realized volatility. When this pattern is present at market/asset highs, it's a big warning. However, when we see this closer to market/asset lows, it's a signal that the options market believes the volatility in this asset is likely to reverse.

So, over the short term, our plan is to continue to rotate into lower beta positions, ride any momentum of our higher beta plays (CFLT, VYGVF, ASAN, AFRM, etc), and then build cash along the way.

Over the longer-term time frame, we plan to have a reasonable cash position to accumulate shares of great companies for when the economic environment clears up and the bull market resumes. Our targeted themes will continue to be semis, as Beth's long-term thesis is starting to really pick up, as well as Cloud. As growth slows and rates move higher, borrowing costs will be affected as will revenue streams. In a slow-growth environment, we tend to see companies address margins in a much more aggressive fashion. We saw this in 2020 regarding cloud. The cloud migration intensified because companies saw that cutting costly IT infrastructure budgets and moving to cloud systems both reduced overhead and made their business more efficient. We believe the same will happen in the current environment.

Arguably, the most cost-effective microtrend is the work-from-home trend. This allows companies to reduce COL allowances as well as expensive real estate. This trend is here to stay, and we are only in the early stages. For this reason, we like plays like ASAN, ZM, MNDY, etc. Regarding Zoom, it showed a 94% enterprise growth on top of triple-digit comps. Yet, the market continuously beats it down as a consumer play that peaked during COVID. This is a mistake and allows for a great chance to buy a quality company at low relative valuations. Though we did not expect the market to beat it down this much, we do believe a relative floor is under Zoom based on its current price to forward growth projections.

Look for ideas like this as we move into 2022. If/when we start approaching any bottom from the coming correction we will shift our focus to more high beat/speculative plays. But, for now, defense is warranted for anyone looking to not be shocked by 2022. As always, we developed a thesis based on incoming data. If that data changes, so will our thesis and pivot. We are not looking to be right, only make money. Markets are fluid, and thus require the need for pivots If anything changes, you will be the first to know.

Also, it's important to not overreact and sell everything or buy everything in an emotional rush. Instead, we prefer to tilt our portfolio into a defensive/offensive posture. We will target 10-15% cash if our plan for a bounce manifests.

Hybrid and work from home environments are a fundamental tailwind for cloud-based tools that help facilitate this key micro trend. Due to the inherent benefits of hybrid/remote environments, such as decreased fixed expenses (rent) and increased access to global talent, along with the necessary infrastructure in place from the rise of cloud computing, this trend will gain momentum going forward.

Asana is one of the key cloud-based tools that facilitates efficient hybrid work environments and stands to benefit from the structural shift underway that is transforming how people work. Asana is a work management platform that helps teams orchestrate work across an entire enterprise, connecting teams around the globe in an easy-to-use platform. The thesis is fairly easy: do you think workers will go back to being in-office full-time? If not, then more cloud-based tools will be required to perform work efficiently. Notably, these tools were already rising in popularity prior to Covid based on the efficiency factor alone.

Customers use Asana to improve team collaboration and workflow management, helping teams track their progress on projects, assign tasks and responsibilities to employees, set deadlines and keep a record of data related to their work. The company was founded in 2008 by Facebook executives Dustin Moskovitz (co-founder of Facebook) and Justin Rosenstein in 2008.

The two had worked together at Facebook and experienced firsthand the coordination challenges the company faced as it rapidly scaled its business. The two realized that they were spending a significant amount of time trying to figure out who was responsible for what, essentially creating ‘work about work’. This unproductive bottleneck inspired them to create a product that would help organizations coordinate their work.

One of the company’s main focuses has been to increase employee productivity by helping them focus on priority tasks and avoid distractions. Asana has been used by a wide range of companies for multiple uses, such as product launches and marketing campaigns. It helps its users know in real-time what each member of the team is working on and allows managers to easily check project progress to ensure that tasks are completed successfully and on time.

With the rise of remote work environments, Asana’s solutions have experienced rapid growth and demand for its solutions has been especially strong with enterprise customers. Asana went public via a direct listing in September 2020 and the company’s stock is up about 135% since its listing and had gains of about 390% during its peak a month back. Despite the recent pullback in Asana’s stock price, the company remains well positioned to continue to gain share in the rapidly growing work management market (i.e., same story a month ago at a discounted price).

Hybrid-work-from-home will be the future working environment for many organizations, with 73% of employees wanting a flexible remote work option. I am bullish on this micro trend and believe that companies in this space will continue to grow going forward. Asana is a beneficiary of hybrid work environments, evident in its exceptional strong revenue growth, which recently accelerated to 70% in the most recent quarter. The I/O Fund noticed Asana’s rapid growth earlier this year and took a position, realizing an 85% gain in under a month.

Asana, at the time, was quite undervalued based on their expected growth, so we initiated our 1st buy in February at $40. We decided to ride the volatility in Asana in March, and instead looked for breakout, which manifested in May when we added again at $33.25. We became fully allocated in Asana on May 20th, and set our targets above. We trimmed this position 3 times, locking in gains between 65%, 115%, and 224%. We closed the position on November 8th for a 285% gain. Recently, we started accumulating again in the $70s and again in the $60s.

We still like Asana at the I/O Fund, however it’s a position we decided to actively manage rather than buy-and-hold. It could turn into a buy-and-hold but for now requires a more active stance. In the article that follows, I discuss Asana’s market opportunity, product roadmap, financial performance, competitive landscape, and key risks that investors should be aware of.

Market opportunity

The company operates in a large market that is rapidly expanding. According to Allied Market Research, the team collaboration market size is expected to grow at a compounded annual growth rate of 13% for the next decade and reach a total addressable market of $27 billion by 2027. Furthermore, Grand View Research estimated that the global productivity management software market was $43 billion in 2020 and is expected to grow at a CAGR of 14% from 2021 to 2028. In Asana’s recent presentation, they estimate that their total addressable market for workplace solutions will be nearly $51 billion by 2025.

To give a sense of the large market opportunity in front of the company, a recent Forrester Research report estimates that there are about 1.25 billion information workers that would benefit from using Asana’s solutions. The company believes that it is still in the early innings of its the market opportunity and estimates that its market penetration is less than 3% of its addressable population of information workers. Looking forward, there is ample room for Asana’s topline to continue to expand as more information workers take advantage of work management solutions.

Product Roadmap

The company’s platform is built on its proprietary, multi-dimensional data model that it calls the Asana Work Graph. It has features like boards that allow users to easily create tasks for the team, view what other team members are working on, and create different views like calendar list views. Furthermore, the timeline feature allows decision makers to quickly learn the status of a task, who is responsible for executing the work, and helps reduce redundancies.

There are also reporting tools that provide key information about work, such as files, comments and metadata. The result is that Asana helps teams collaborate across an entire organization and ensures that projects are completed on time and efficiently. Asana’s benefits compound in large, complex hybrid work environments such as large enterprises, which I touch on in more detail below.

Another key advantage of the Asana platform is that it has integration capabilities with major apps, such as Microsoft Teams, Okta and Dropbox. These integrations and partnerships with other cloud-based tools help further facilitate the transition to hybrid work environments and improve efficiencies.

With the rising number of information workers who are increasingly working remotely, Asana’s products help employees coordinate core projects, improve productivity across the enterprise and remove information silos that have historically separated teams across an enterprise. Asana’s solutions also yield a solid return on investment for its customers. According to a study conducted by the IDC, respondents reported that Asana has increased organizational efficiencies by reducing time spent on emails by 33%, improved process execution by 42%, and has yielded a 224% 1-year return on investments for its customers.

Asana has also partnered with numerous technology firms to add more features and functionality to its platform. A standout that management highlighted during the Q2 earnings call was Zoom’s integration within Asana. This unique feature allows Asana customers to create a Zoom meeting while they are performing a task directly inside the Asana platform. Once the Zoom meeting is over, the Zoom recording and the transcript can be added to Asana and tasks discussed during the meeting can be assigned to owners. This functionality improves the efficiencies of meetings and helps reduce the amount of time spent “working on work”.

As mentioned above, work complexity compounds as organizations increase in size and become more dispersed with hybrid work environments. Asana’s Work Graph helps reduce the growing complexity for enterprises and replaces micro-management with macro-management, “by aligning [leaders] around key objectives and the work needed to achieve them no matter where they are in the world” (Q3 Earnings Call). We can see the success that Asana has had reducing hybrid complexities by observing growth trends with large enterprise customers, which have accelerated recently. I discuss this trend and Asana’s financials in more detail next.

Financials

Asana released its Q3 FY2022 results on December 02, 2021, which beat both on the top and bottom-line. Revenue growth accelerated to 70% YoY and quarterly sales were $100 million, which beat analysts’ estimates by $6 million. Revenue has increased sequentially for at least 11 consecutive quarters and Asana now has an annualized topline run rate of over $400 million. The growth was led by strong customer metrics as total paid seats surpassed 2 million and total paying customer increased 28% YoY to 114,000.

However, the real story is Asana’s success with enterprise customers, which generally pay more and sign longer-term contracts. Because of this, enterprise customers are generally the most valuable type of customers for a software provider. Asana’s success with this cohort speaks to the overall value that its workplace solutions provide.

For example, while total paying customers increased 28% YoY to 114,000, customers spending $50,000 or more per year (enterprise customers) grew by 132% YoY to 739. This represented an acceleration from the 111% and 92% YoY growth rate in enterprise customer count in Q2 and Q1 FY2022, respectively. The accelerating growth in enterprise customer count highlights the benefits that Asana provides to large, complex hybrid environments. Further highlighting this strength, Asana’s dollar-based net retention ratio for enterprise customers was 145%, up from 140% in the prior Q3 period and exemplifying that enterprise customers are expanding their usage of Asana overtime, a sign of strength.

Some of the large key customer wins in the quarter included Warner Music Group, which chose the company’s enterprise solutions “to organize, manage and track the end-to-end process of how they identify, evaluate and bring new artists into its various labels faster and more effectively”. Asana also expanded its deal with a Japanese customer, which is one of the largest automotive manufacturing companies in the world. Management explained that the Japanese auto customer’s expanded agreement was to help manage their software and product developments (Q3 2021 Conference Call). These customer wins highlight that Asana is useful across multiple industries and different geographies.

It is noteworthy that while Asana is growing its enterprise customer base, it is doing so on a global scale. This provides support that Asana is still early in its topline run rate and has amble room to expand both domestically and globally. Furthermore, Asana is preparing for global growth as it recently expanded its support to 13 different languages, which will help the company capture customers is numerous markets around the world.

Looking forward, Asana expects Q4 revenue to be in the range of $105 million to $106 million, representing a 53% to 54% YoY growth rate. While this represents a deceleration from recent growth rates, the company is likely being conservative with their topline guide. For instance, management guided Q3 sales to grow 59% YoY (at the mid-point) and actual Q3 sales growth came in at 70% YoY.

Management also expects Q4 adjusted operating loss of $53 million to $51 million and adjusted net loss per share of ($0.28) to ($0.27). This represents a larger loss than the Q3 adjusted operating loss of $41 million and adjusted loss per share of ($0.23). While the guide for larger losses is somewhat concerning, the company is investing to grow rapidly to capture market share in the large, untapped work productivity market. As a result, Asana is front-loading investments today that will pay dividends in the future.

We can see the front-loading of expenses by observing trends in sales and marketing (S&M) expense. As shown below, the company’s S&M expense increased as a percentage of total revenues to 73%, which was up 200 bps QoQ but down 900 bps YoY. Asana’s COO Anne Raimondi explained on the Q2 call that the company has been ramping hiring to support international expansion. Specifically, she stated that the company has been “increasing sales and marketing capacity across all of these new offices and regions. So, lots of hiring to support our customers”. Ultimately, I am not concerned with the rise of S&M expense margin since the company is investing in its future growth, which will help the company quickly scale its operations, improving both earnings and cashflows in the long run.

Moving to cashflows, quarterly free cash flow was -$30 million as of Q3 FY2022, down YoY from -$20 million for the same period last year. However, YTD free cash flow -$46 million, an improvement from the prior year metric of -$58 million. Cashflows can be lumpy, but as enterprise customers continue to increase as a percentage of total sales, their recurring upfront cash payments will lead to improving cashflows overtime.

Stock-based compensation and insider purchases

It is also noteworthy that Asana pays some of its salaries with stock-based compensation (SBC), which cosmetically improves the presentation of cashflows. For instance, in the latest quarter, Asana issued $26 million in SBC, up from $9 million in the prior year quarter. However, quarterly free cashflow improved $18 million YoY, or $1 million absent the benefit from increased stock-based compensation. The increase in free cashflow after adjusting for the rise in SBC highlights that Asana has been able to leverage its scale to a degree. Nonetheless, cashflows will remain lumpy going forward and SBC growth may outpace free cashflow generation in the near term.

A benefit of rising SBC is that it makes employees owners in the business, giving them a vested interest in the company’s success. This in turn should improve employee retention and lower turnover, which will help Asana better scale its operations as seasoned employees are generally more efficient than new hires.

Management has also been purchasing shares, which can be a sign that management believes that the company is undervalued. For instance, board member Lorrie Norrington recently purchased 3,733 shares on December 6th for a total purchase value of $248,000 (~$66.51/share). This was the second time she had purchased shares this year after spending $199,000 for 6,200 shares in March 2021(~$32.12/share). Ms. Norrington’s purchases follow a drop in Asana’s price following the general tech sell off that occurred in the back half of 2021. Given the company’s continued strength with enterprise customers discussed above, Asana may be at a decent risk/reward right now.

Another insider that has been purchasing shares is CEO-founder Dustin Moskovitz. CEO Moskovitz has purchased over 6 million shares year to date, which is generally a very bullish signal. However, the purchases likely relate to the redemption of a convertible bond that CEO Moskovitz holds in a trust. As disclosed in Asana’s 10Q, the company elected to convert a convertible note that was “held by a trust affiliated with Mr. Moskovitz and the shares were accordingly issued to the trust. The conversion of the Convertible Notes therefore increased Mr. Moskovitz’s voting power”. Nonetheless, the increase in CEO Moskovitz ownership further aligns his incentives with shareholders, which is generally a positive development.

Competition and why Asana is winning

The work management platform space is very competitive and there are numerous public and private companies competing with Asana. Asana’s main publicly traded competitors are Atlassian (Jira) and Monday.com, but they also compete with Smartsheet and other private companies such as Airtable. For the sake of brevity, I will only be discussing Monday.com and Atlassian’s Jira offering and what sets Asana apart from these competitors.

One of the key pillars separating Asana from Jira is that Asana is built for all teams within an enterprise, while Jira was specifically designed for software developers. Asana claims that Jira is not flexible enough to be applied to teams across an entire enterprise, while Asana was built to be applicable to all employees within an organization. However, the two are not mutually exclusive and users are able to integrate the Jira cloud within the Asana platform, brining Jira’s software development focus into Asana’s easy to use workflow platform. This integration allows all employees to remain in sync and helps various teams, such as business and software development, collaborate across the organization. To remain competitive, Atlassian bought Trello in 2017.

Possibly Asana’s most direct competitor is Monday.com, which went public in June 2021. The two are the leading providers of workflow solutions and both are growing strongly. Asana differentiates itself by being easy to use, transparent and user friendly, making it accessible to all users in an organization, even the non-technical ones. On the other hand, Monday.com claims that it is a Work Operating System, that is more advanced and customizable.

Without getting into the differences in the platform offerings, the key differentiator between the two is likely price. Given that enterprise customers are important to both of these companies’ success, and that neither company directly discloses enterprise pricing, I relied on enterprise customer metrics to get a sense of which platform is favored by large organizations.

As mentioned above, Asana’s enterprise customers growth recently accelerated from 111% to 132% YoY growth, the fastest pace of YoY growth in FY2022. Similarly, Monday.com also reported an acceleration in enterprise customer growth, as customers with annualized recurring revenue >$50,000 grew 231% YoY, up from the Q2 growth rate of 226% YoY.

While Monday.com is growing enterprise customer’s faster than Asana, Asana’s enterprise growth is accelerating more rapidly. For instance, Asana’s enterprise customer growth accelerated 2,100 bps in the most recent quarter, versus to 500 bps acceleration for Monday.com.

Moreover, Asana had 739 enterprise customers in the latest period, which was 20% higher than Monday’s 613 enterprise customers. However, Monday.com was founded in 2012 while Asana was founded in 2008, so Asana’s head start may be the reason why Asana currently has more enterprise customers.

Unfortunately, neither company directly discloses enterprise pricing, but Asana did announce that they have some seven and eight figure deals, highlighting how not all enterprise contracts are not the same. It is noteworthy that both companies report high gross margins, with Asana reporting a GAAP gross margin of 91%, which is about 300 bps higher than Monday.com’s GAAP gross margin of 88%. Asana’s higher gross margin suggests that it is not sacrificing price to drive sales growth, which can be a sign of competitive strength, especially given its recent acceleration in enterprise growth. However, both companies have very similar metrics and are valued about the same (Asana’s market cap is $13 billion while Monday.com market is $12 billion as of publication).

The market likely needs more time and information to fully understand who the winner will be in the work management platform space. However, recent trends suggest that Asana may be pulling ahead given its rapid acceleration with enterprise customers and higher gross margins. We are still early in Asana’s growth story, and there are plenty of risks ahead of the firm, which I discuss in more detail next.

Risks:

Asana faces significant competition in the fast-growing work management space and it is not yet clear who the winner will be. Furthermore, larger companies could very well enter the space and compete with Asana’s solutions, possibly turning customers into competitors.

Asana has also experienced rising losses as it scales its business. The company’s operating expenses are expected to be high as it invests in human capital and office space to expand its operations globally. There is also no clarity as to when the company will be profitable, and shareholders may be diluted if cashflows do not improve going forward. Furthermore, the company recently reported a deceleration in bookings growth, which may forewarn a broader slowdown in sales in the near term. CFO Tim Wan addressed this concern during the Q3 call and explained that bookings are not a great barometer for growth, due to the large amount of customers still on monthly billing plans. Since monthly customer do not impact deferred revenue, they skew the calculation of bookings. Nevertheless, bookings growth will need to be monitored going forward since it is an important metric for Software-as-a-Service companies.

Conclusion

Looking forward, Asana appears well positioned to continue to capture share in the work management space. Hybrid and remote work environments are a structural tailwind that will drive demand for work management solutions. Furthermore, these tailwinds will likely gain momentum due to the inherent benefits they provide to both employees and employers. Asana recently reported an acceleration in topline growth, and enterprise customer metrics accelerated even faster. While it is not yet clear who the winner will be in the work management space, Asana appears well positioned given its high gross margins and strong customer metrics. Asana has a large addressable market in front of it and its penetration is very low, suggesting that we are still very early in the company’s growth story.

Royston Roche contributed to this article.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis. The I/O Fund has owned Asana stock in the past and currently owns Asana stock at time of writing. There are no plans to change the position in the next 72 hours.

Follow me on Twitter. Check out my website or some of my other work here. Twitter. Check out my website or some of my other work here.

Below, the team looks at Micron – a semiconductor company the I/O Fund has owned in the past. Micron is in third place behind Samsung and SK Hynix. We analyze both product and financials to determine if Micron has what it takes to capture more market share across data centers, automotive/industrial, and 5G smartphones and edge devices. Earnings are on December 20th.December 20th.

Micron is one that we are watching closely but do not own at time of writing. Please reference Trade Notifications archived on the dashboard and the forum for updates. on the dashboard and the forum for updates.

Overview of Micron’s Products:

By Beth Kindig

When we first covered Micron, the company’s revenue was two-thirds DRAM and one-third NAND. The company’s most recent earnings report shows a heavier weight on DRAM at three-quarters revenue compared to one-quarter revenue from NAND.

NAND memory saves data even when the power is removed, such as when a cell phone is turned off. Beyond mobile devices, NAND is found in traffic lights, digital advertising panels/displays, and anything with artificial intelligence that needs to store data.

Dynamic RAM, or DRAM, stores memory when a device is on, such as PC processors and graphics cards. DRAM is also used in gaming devices and video game consoles. DRAM is 100X faster than NAND, lasts longer, and is smaller in size. However, DRAM is known as volatile memory which means when power is turned off, it does not store data. The benefit of loading the data into the RAM is that reading the data is much faster than reading it from the hard drive.

According to the CEO of Micron, AI servers will require six times more DRAM and twice the SSDs compared with standard servers. In the most recent earnings report, it was also pointed out that “DRAM and NAND stem share of the semiconductor industry has steadily grown over the last two decades, from around 10% to approximately 30% today.” Today, data centers are the largest market for memory and storage due to the growth driven by cloud.

Hyperscale data centers are growing faster than DRAM supply can keep up with. Due to higher capacities and low latencies, DRAM is being used across health care, the military, automotive, networking systems, and data centers. DRAM is being used in the Internet of Things (IoT) due to low latency with automotive using up to 80GB compared to 5.5GB in PCs and 2.5GB in handsets.

NAND is used to store pictures or music on a mobile device and is also particularly well suited for edge devices because it’s ideal for high data storage density. Although DRAM drives the majority of Micron’s revenue right now, NAND is the growth segment to watch as AI workloads move to the edge and will require NAND for the increased energy requirements, portability, and ability to store massive amounts of data.

According to FiorMarkets, Global 3D NAND Flash is expected to grow at a 32.3% CAGR from 2019 to 2025. 360 Research Reports put the CAGR at 20.6% between 2021-2026. Overall, NAND is expected to grow at 11.05% between 2021-2026. DRAM has a CAGR of 7% between 2020 and 2026.

Micron’s revenue segments

By business unit, Micron saw the most revenue growth from Embedded (EBU) at 108% year-over-year and 23% QoQ growth. This was also the largest growth in the prior year. EBU refers to memory and storage products used in automotive, consumer markets, and industrial applications. In 2019, Micron had expanded its wafer fab facility in Virginia with a $3 billion investment to manufacture 20nm/1xnm DRAM and 3D NAND for automotive infotainment, advanced driver-assistance systems (ADAS), and also industrial automation and surveillance applications. Two years later, the investment and engineering expansion appears to be paying off.

This is a key segment to watch as industry CAGR for automotive processors is expected to be 65% through 2023, according to IDC. This is driven by automation and the memory content per car will increase up to 16GB of DRAM and 1TB of NAND to run AI, supercomputer, and high-def mapping. Micron holds 48% of automotive memory market share and is the primary supplier to Nvidia and Intel.

Compute and Networking (CNBU) grew at 26% growth year-over-year and 15% quarter-over-quarter. This is the segment that serves cloud servers and PCs, plus graphics and networking markets, and this segment is the largest source of revenue and operating income for Micron. Bradley expands more on this in his write-up below.

Mobile Business Unit (MBU) focuses on mobile and smartphones and mobile saw its highest-ever mobile revenue in fiscal year 2021. This is partly driven by the uMCP5 multichip package which allows smartphones to handle data-intensive 5G workloads. Micron has also released low-power DRAM for edge devices in a promotion with MediaTek. Micron offers a combined chip for both NAND flash storage and DRAM for 5G smartphones to extend battery life and increase performance without taking up circuit board space. This segment is also one to watch as the memory in smartphones will increase exponentially with 5G due to large data volumes.

Micron has exposure to PCs. This has been a boon during the past few years yet could also weigh on Micron if consumer spending slows.

3D NAND product update

Last year, Micron released a 176-layer 3D NAND product that has a layer count 40% higher than the nearest competitor, which is Samsung. The new NAND device is 10 times denser than previous 3D NAND devices which allows smartphones and edge devices with capacity limitations removed and increased power efficiency. Cloud storage also benefits due to being data intensive.

According to Micron, this device has the “industry’s highest data transfer rate” of 1,600 megatransfers per second (MT/s). The device is the same height as the 64-layer design with a fabrication technique that removes stack height limitations to provide higher storage capacities. The company uses CMOS-under-array (CuA) to build a multi-layered cell stack for more memory to be leveraged in a smaller space while also decreasing die size.

The replacement-gate (RG) flash technology replaces the traditional floating-gate design, and according to Micron’s whitepaper, helps the device remain competitive in terms of time it takes to program and/or to limit the reduction in performance. Micron points out in the paper that extending the number of tiered stacks creates cell-to-cell capacitive coupling, which leads to lower program times. Therefore, the more tiers or layers that competitors release will not necessarily result in better performance due to design limitations. This performance becomes critical as program algorithms can add to time delays when writing the data.

In this iteration, Micron changed the design to mitigate issues of the “cell-to-cell capacitance structure,” or a reduction of electric field duration and increase in voltage threshold (VT), which results in higher endurance life span, increased power efficiency, increased storage capacity, and doubled speed of write performance. The company also changed the material from polysilicon to metal. These two improvements result in Micron’s RG 3D NAND to perform up to 2X faster than other current 3D NAND devices.

Memory and storage can be very competitive in terms of price, so we want to track incremental product improvements. According to Micron, “current 3D NAND design has begun to reach the limits of its monolithic die-level maximum capacity. It will continue to fall short of the immense system-level storage capacities demanded by future data-driven applications. Cell-to-cell capacitive coupling complications and smaller etch requirements account for many of these limitations.” If Micron is correct, then this could be an opportunity for the company to see more market share on 3D NAND.

NAND is expected to see a 30.8% increase in total bit demand and an oversupply in the second half of next year. Competition is expected to drive a decrease in average sales price (ASP). In the earnings presentation, Micron forecast calendar year 2022 growth of 30% in NAND.

DRAM product update

Moore’s Law states that the number of transistors or processing power on an integrated circuit doubles every two years while the cost is halved. This has led to shrinking the circuits to fit more transistors or memory cells in the limited space. At one point, you could see a transistor and now they are measured in nanometers, which is not visible by the human eye. This helps chips switch faster and use less energy and are cheaper to make, as well. As size decreased, memory chips moved to the Roman and Greek alphabet to name nodes which is why Micron calls their DRAM “1-alpha.’ This provides a 40% improvement over bit density compared to the 1z node and power consumption has improved by up to “20 percent.”

These chips are manufactured without EUV, or Extreme Ultraviolet Lithography. This manufacturing method uses smaller 13.5nm wavelengths of ultraviolet light to etch wafers as opposed to lasers from Deep Ultraviolet Lithography (DUV). You could argue that EUV is a point of weakness for Micron as Samsung is using this manufacturing method while Micron is delayed until 2024.

DDR5 is the company’s increased bandwidth product that will increase core count resulting in up to 85% increase in bandwidth. The double date rate (DDR) product has been primarily focused on more bandwidth while previous generations focused on reducing power consumption to serve the needs of mobile applications and data centers. The performance increase is between 1.36X and 1.87X. This has not been released yet but is expected to be released soon.

DRAM is expected to see a decrease in average sales price (ASP) next year while DRAM bit demand will increase by 17%. This will lead to an oversupply in the second half of the year. Micron is forecasting DRAM revenue to be in the mid-to-high teens.

Being U.S. based, plus MU, lowered exposure to China

It’s very helpful that Micron is the only U.S. based manufacturer of memory during a time when suppliers are relocating to the United States. Micron announced that it intends to invest $150 billion globally over the next decade in “leading-edge memory manufacturing and research and development (R&D) including potential U.S. fab expansion.” The U.S. Senate passed the U.S. Innovation and Competition Act (USICA) which includes $52 billion in federal investments for the domestic semiconductor research, design and manufacturing provisions in the CHIPS Act. Congress is also considering legislation called the FABS Act that would establish a semiconductor investment tax credit. Policy could strategically help Micron compete with Samsung.

The next hurdle for semis long-term is relying on China sales. Micron changed how they report geographic information from ship-to location to customers headquarters. Micron also lost Huawei revenue during the same time period which Keybanc estimates was 7-9% of Micron’s revenue.

Here's a snapshot from fiscal Q4 2018 where “ship-to location” was heavily weighted to China.

If we go on customer headquarters then we see that Micron has about 18% exposure in FY2021 if we include China and Hong Kong.

Competitors

Micron was the first to build and ship a 176-layer NAND last year and SK Hynix was close behind. In early 2020, Kioxia and Western Digital released a 112-layer device and are expected to move to 160-layer soon based on split-gate architecture by stacking two 80-layer structures. By splitting the gates, the cell size is reduced in half and this increase the capacity. YMTC was a new competitor from China that released a 128-layer very quickly by skipping the 96-layer generation. The company uses an expensive copper hybrid bonding technique that enables higher bit density. YMTC is likely to take market share in China across all memory and storage competitors.

According to TrendForce, SK Hynix saw the largest increase QoQ on NAND flash sales with a 25% QoQ increase and Kioxia reported 3D NAND sales of 20.8% QoQ compared to Micron’s 8% increase QoQ. In terms of DRAM, TrendForce reported that Samsung grew it’s lead with 11% growth QoQ while Micron also grew it’s lead with 12% growth QoQ compared to SK Hynix at 8% QoQ.

Micron is Becoming Less Cyclical

By Bradley Cipriano

Micron has reported strong results over the last few years and this continued into 2021. Micron is a key player in the memory market, which is going through a structural change. Demand is no longer dependent on PCs, rather memory demand is now being driven by much stronger tailwinds such as datacenter server growth and the rollout of 5G. This structural change is making Micron less cyclical.

Looking forward, Micron expects these structural tailwinds to continue to drive growth at the company. CEO Sanjay Mehrotra explained it well during the Q4 FY2021 Conference Call when he said that “Industry trends like the broad integration of artificial intelligence into all computing, proliferation of the intelligent edge, continued data center growth, and deployments of 5G networks create new and expanding opportunities for Micron.”

The rise of cloud data centers has led to a structural increase in demand for semiconductor components such as DRAM and NAND memory, which helps smooth out the boom and busts cycles that Micron was historically exposed to. Micron explained the new market dynamic in its 10K when it stated that “data is today’s new business currency, and memory and storage are a critical foundation for the data economy”.

The IDC estimates data creation will explode going forward (pictured below), driven by the rise of cloud computing. Furthermore, the IDC estimates that less than 2% of data is saved today, and that data creation is far outpacing data storage capacities.

Furthermore, the ramp of the metaverse also requires massive scaling. During Marvel’s (MRVL) Q3 Conference Call, the company stated that the metaverse “will significantly accelerate a number of key trends, which are already occurring in the cloud today, including the need to store huge amounts of data”. With Meta (aka Facebook) guiding for $34 billion in capex in 2022 to develop the metaverse, the demand for data storage will likely be strong for the foreseeable future.

We can see the structural change underway by looking at results over the last four years. For instance, aggregate gross margin over the last four years was 44%, well above historical (cyclical) periods, and aggregate operating cashflow margin was ~50% over the same time period. In response to the structural change underway in the memory market, management recently initiated a quarterly dividend ($0.10 per share), which highlights management’s contention that the memory market is becoming less cyclical. I discuss Micron’s recent financial results in more detail below.

New memory technologies keep pace with cloud innovation

To address the issue of exploding data creation, Micron has innovated on some key new technologies that will enable datacenters to capture and retain much more data. Two of these key new technologies are 176-layer NAND and 1-alpha DRAM, which Micron began shipping in volume this year.

Micron stated that the introduction of “176-layer NAND and 1α (1-alpha) DRAM represent major technology breakthroughs for our company and the first time in our history that we have achieved industry leadership across these two flagship technologies”. 176-layer NAND is an extension of 3D NAND, and as the name implies, has 176 layers of cells that dramatically increase memory capacity. Previously, NAND was on a 2D plane with just one layer, and Micron has significantly increased capacity by expanding beyond a single layer of memory. Furthermore, the 1α DRAM memory node was introduced in 2021 and materially improves the performance of DRAM memory (20% to 30% higher yields), which is critical for cloud servers that rely on low latency and high performance.

With the continued development of AI, cloud servers require significantly higher quantities of DRAM, as the number and capabilities of these intelligent edge devices increases, more data is stored, processed and accessed in the cloud. The demand for storage in the cloud environment is growing exponentially and Micron’s industry leading 1α DRAM nodes should be able to capture market share in this fast growing segment in FY2022. We can see the strength in cloud computing by looking at Micron’s Compute and Networking segment (CNBU) sales, which increased 34% YoY to $12.3 billion during FY2021 and rebounded from an 8% YoY decline in the prior year.

CNBU is Micron’s largest segment (44% of sales) and continued strength here will be rewarded by the market. With that said, there was a deceleration in this segment between fiscal Q3 and fiscal Q4 both YoY and QoQ from 49% down to 26% YoY growth and down from 25% to 15% on QoQ growth.

In Q2 FY2021, Micron also began shipping 1α DRAM nodes for mobile, which improved power efficiency in mobile phones, and allows for memory intense use cases like smart photography. Management explained on the Q4 call that 5G phones have 50% more DRAM than 4G phones, meaning that the continued adoption of 5G phones should be a significant tailwind for Micron going forward.

Micron also began volume shipments of 176-layer NAND for mobile in 2021. On the Q4 call, CEO Mehrotra explained that “176-layer NAND-based mobile product went from just introduction to 1-million-unit shipments in a record time. Fastest RAM in the history of the Company”. The ramp in 176-layer NAND helps put into perspective how much demand there is for Micron’s new technologies. Following this strong demand, Mobile (MBU) segment sales increased 26% YoY to $7.2 billion in FY2021, a record high. The continued roll-out of 5G phones will likely be a tailwind for Micron going forward.

The roll out of these new technologies is just now beginning to ramp. To accelerate the roll out of these new technologies, Micron expects to increase its annual capex by 20% YoY to $12 billion, which follows a 22% YoY rise in capex in FY2021. Micron explained that capex will be driven by its continued transition to 176-NAND, as well as infrastructure support for the introduction of new technologies such as EUV lithography. While increased capex spend does not guarantee increased sales, there are also signs in Micron’s balance sheet that point to heightened demand in the near term, which I discuss in more detail next.

Micron’s financials

Following the roll out of new technologies during the year, Micron reported strong results to end its fiscal year. Specifically, Micron’s Q4 FY2021 sales increased 37% YoY to $8 billion, an acceleration from the 36%, 30%, and 12% YoY increase in Q3, Q2, Q1 respectively. Gross margin increased 1,300 bps YoY to 47%, the highest level since Q3 FY2019. On a rolling four-year basis, gross margin was 44%, highlighting the strong success Micron has experienced in recent years. As shown below, the sustained improvement in four-year rolling gross margin suggests that Micron’s business is becoming less cyclical.

The strong gross margin flowed down into operating margin, which increased 1,600 bps YoY to 36%. On an annual basis, operating margin improved from 14% in FY2020 to 23% in FY2021, while non-GAAP operating margin was 28%, up 1,200 bps YoY. The strong margin performance was driven by pricing increases across DRAM and NAND products and ongoing product transformation. Looking forward, management guided that gross margin would remain strong at 47% +/- 100 bps in Q1 FY2022, as the company continues to benefit from the new product releases (discussed in more detail above).

Continuing down the income statement, GAAP EPS increased 175% YoY to $2.39 and on an annual basis GAAP EPS increased 117% YoY to $5.14. In the last five years, Micron has reported an aggregate $28.94 in GAAP EPS, or nearly five times as much as it had earned in aggregate earnings over the prior 33 years (dating back to 1984). As discussed above, Micron had historically been a cyclical company dependent on PC demand for memory, but tailwinds from datacenter and mobile have structurally changed the demand environment for memory and have made Micron’s business less cyclical and more profitable. Below, we look at the 4-year rolling gross margin to discuss the continued strength in the company.

We can also see this outperformance in cashflows. Micron’s annual cashflow margin was robust at 45%, and FCF margin was also strong at 9%. Annual FCF margin has been positive in all but one year since 2012 and has been positive for five consecutive years. As a result of the strong cashflow performance over the last few years, management initiated a quarterly $0.10 dividend.

CFO Dave Zinsner stated on the Q4 call that “the initiation of a dividend is an important milestone that reflects the structural transformation Micron has undergone over the last several years, and it shows our confidence in the sustainability of our cash flow generation”. He added that Micron expects to return more than 50% of FCF to shareholders through dividends and buybacks going forward. If the memory business is becoming less cyclical, then shareholder returns could be substantial going forward given Micron’s robust profitability and cashflow generation.

Finally, inventory trends also highlight the strong demand for Micron’s products. Inventory declined 17% YoY despite the 37% YoY growth in sales, as Micron has struggled to replenish lean inventory levels in response to strong customer demand. Typically, in cyclical industries, elevated inventory levels can be a sign of concern, so the drawdown in inventory highlights the strong demand for memory in the current environment.

Inventory composition is also bullish, as raw material inventory increased to 11% of total inventory, a three-year seasonal high, while finished goods inventory declined from 19% of inventory to 11% in Q4, a five-year low. The drawdown in finished goods highlights that Micron is shipping its product faster than it can be replaced, highlighting the strong demand it is experiencing. A rise in raw materials and decline in finished goods means that management is quickly selling its product and anticipates that this demand will continue.

Outlook and valuation

However, a risk with the low inventory levels is that Micron will not be able to fulfill the strong demand in the near term. There are also supply chain issues outside of Micron’s control that may impact demand in the near term. CEO Mehrotra explained on the Q4 call that some PC customers are adjusting memory purchases in the near term due to non-memory component shortages. He added that supply chain constraints for IC components will limit some large shipments in the near term.

This commentary helps explain Micron’s Q1 FY2022 forward guide miss. Micron guided Q1 sales to be $7.65 billion at the mid-point, 10% below the Street’s initial estimate at $8.5 billion. Micron also guided Q1 EPS to be $2.10 at the midpoint, or 15% below initial expectations of $2.48. CEO Mehrotra explained that while there are near term supply chain issues, “shipping growth will resume in the second half of the fiscal year, and we're planning to deliver record revenue with solid profitability in fiscal 2022”. While Micron only quantified its Q1 guide, CEO Mehrotra’s statements suggest that growth will rebound in the second half of the year as supply chain issues and low inventory levels normalize.

Looking forward, Micron is expected to report Q1 earnings on December 20th. Q1 sales are expected to increase 33% YoY to $7.65 billion and non-GAAP EPS is expected to rise 169% YoY to $2.10. For the year, Micron is expected to grow sales 16% YoY to $2 billion and to report $9.01 in non-GAAP EPS, which gives it a 9.2x fwd EPS multiple. This is slightly below Intel’s fwd P/E multiple of 9.7 but above Western Digital’s fwd P/E of 6.7x. Furthermore, Micron’s fwd P/E of 9.2x is below the 15.8x level it reached earlier in the year, which highlights that there is room for multiple expansion going forward.

Micron also trades at a slight premium based on trailing earnings. Its TTM P/E multiple of 16x is 45% higher than the peer median of 11x (peers include Samsung, SK Hynix, Intel, and Western Digital). Micron is likely being awarded a premium over its peers due to its current technological lead in key technologies discussed above.

Conclusion

Micron’s sales grew 29% YoY in FY2021 and management expects this growth to continue into FY2022 as demand for memory remains robust. The memory market is becoming less cyclical due to numerous tailwinds that have expanded demand for memory beyond PCs and into more memory intensive markets such as data centers and mobile. Micron is ramping capex to keep pace with outsized demand and has innovated new technologies to keep pace with the cloud environment.

Management also issued a quarterly $0.10 dividend, which further highlights management’s contention that its market is becoming less cyclical. Micron currently trades at 9x fwd P/E, which is near Intel’s and above Western Digital’s multiple. If the company can prove to the market that its business is less cyclical and that its 40% gross margin and 50% cashflow margins are sustainable, then its multiple will likely expand going forward.

Below, we review Twilio, Snap and Shopify. This quarter, Snap separated itself from other ad-tech companies in the ad rebound cycle. On the surface, this was accomplished through user growth and strong guidance. From a product perspective, our readers knew going into this quarter (and last quarter) that augmented reality has quietly begun its trajectory.

Twilio is a company that recently acquired Segment. This is not your typical acquisition, rather it is a hard pivot into first party data. Twilio’s future very much depends on management nailing this transition. We had presented this in granular detail in our Twilio LTBH (long-term buy and hold) webinar. We see no issues with Twilio’s report, in fact, with Segment Journeys Twilio is ahead of schedule on cross-selling, which began July 1st.

Shopify is a steady winner that we had stated in a Motley Fool podcast was a favorite pick of ours going into 2021 and during our two LTBH Top 10 portfolio review found here and our 2021 portfolio review here. Some of these LTBH positions are like hitting singles and doubles while others we swing for the fences. Shopify has the most potential to become a FAANG stock as the company has solidified its place at the e-commerce infrastructure layer. We discuss why Shopify shows evidence of taking market share from Amazon, and one area in particular where Shopify is stronger. Rarely, do we see such a strong product open the flood gates for distribution at this stage in its maturity; the flood gates for distribution are social media.

Summary:

In May, we disclosed that we were looking to increase our Snap position (and Shopify) and we closed our Pinterest position after reviewing our LTBH portfolio. We could not have been clearer in terms of our conviction on this augmented reality (AR) stock. We also broke down the company in great detail in June, which is worth a refresh if you’d like more product analysis and backstory on the company’s AR strategy and how it relates to Apple’s iOS updates.

There are a few key takeaways from Snap’s earnings. The first is that the product is going through rapid iteration to be a first mover in augmented reality. At the consumer level, you could say Snap is an only mover as there isn’t another company reaching early adopters with this much consistency. The second takeaway is that we’ve seen an ad rebound in many earnings results this quarter yet Snap stands out for its user growth in the face of tougher comps – both this quarter and next quarter’s guidance.

Here is a laundry list of AR product features that Snap discussed in the earnings call:

Cartoon 3D Lenses turn people into 3D-animated cartoons. The Cartoon 3D Style Lens shows the potential for AR features to go “viral” with 2.8 billion impressions in the first week.

Connected Lenses which enables real-time shared experiences, like building LEGO models together

Scan which allows users to scan outfits and find recommendations or the right size/look

A Unity plugin for personalized Bitmojis to be used in games

Lens creators can use Lens Studio 4.0 for features like virtual classification, multi-person 3D body mesh and cloth simulation

Spectacles with 3D reality display

Content products like Snap Original Shows including 177 international channels

Spotlight, where Snaps are showcased, grew a whopping 49% quarter-over-quarter

The keywords from this earnings report are “inside and outside of Snapchat.” Many of the AR features above will reach non-Snapchat audiences. Disney is using the Camera Kit at their theme parks. Bumble is using Lenses to create backgrounds and effects. Viber is a calling and messaging app that uses Snap’s lenses. Restaurant recommendations can be overlaid onto Maps and Poshmark is using Snap’s minis platform for daily shopping events. Although “minis” are technically on the Snapchat platform, they’re coming from developers outside the platform, such as Ticketmaster which uses minis to discover shows and buy tickets.